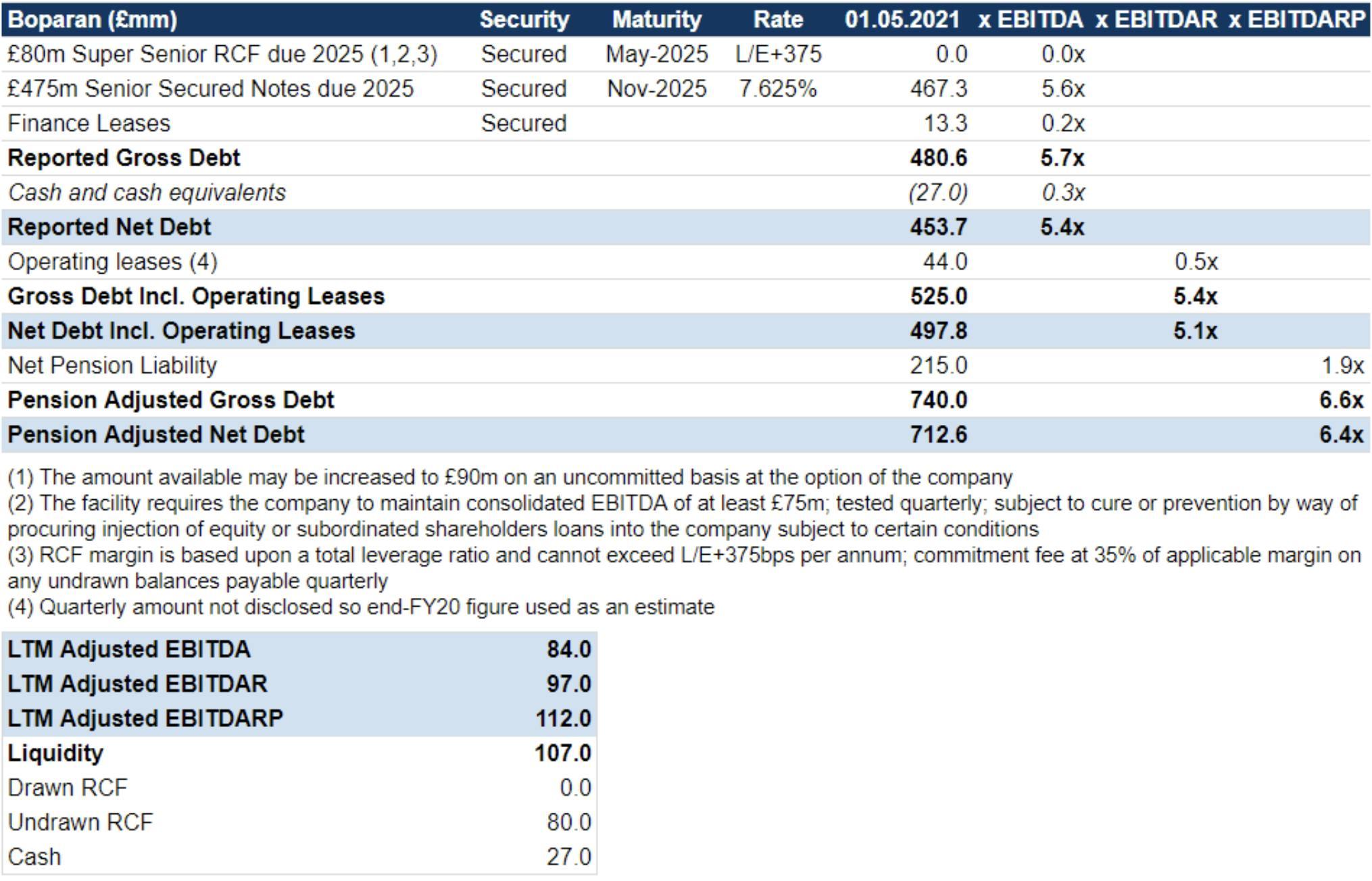

Boparan besieged by Brexit, bottlenecks and bracing headwinds

Boparan is certainly facing its fair share of headwinds, battered on several fronts by external structural and COVID-enduced challenges, and operational issues in its beleaguered Poultry division. The company’s recent bond - issued as part of a stressed refinancing in November 2020 - paying a handsome coupon has suffered the headwinds, slowly limping down from its above-par standing in mid-March to its high-80s position now, yielding an attractive ~11.1% to maturity (not likely to be redeemed at a premium, in our view).

Despite the attractive return potential, the investment thesis is fraught with risk, as the company contends with a growing list of challenges and the balance of potential triggers on the horizon appears more weighted to the downside. There are question marks in our minds as to whether the company can grow into its capital structure, even though the recent refinancing and the use of disposal proceeds reduced the capital stack; following on from the trend in previous years in which disposal proceeds were used to manage the balance sheet.

The growing list of headwinds

Energy costs and the knock-on impact on carbon dioxide (CO2) production: the impact of a dramatic rise in gas prices this year on energy bills has been well documented with UK wholesale natural gas prices up 250% overall since January and a staggering 70% alone since August. This is a headwind in itself for Boparan, as it is for the majority of businesses in the UK and Europe currently, compounding cost inflation pressures on several fronts from rising feed prices to spiking labour and logistics costs.