The inflation surprise is once again opening the door to more, aggressive, Fed hiking (187 bps are now priced in for 2022, from 155 bps last Friday). This boosted the greenback and helped drive Sterling to $1.14 — its lowest level since 1985 — on what is fittingly the thirtieth anniversary of Black Wednesday. Weak UK performance data hasn’t helped, after the ONS posted retail sales volumes down -1.6% in August and non-retail stores volumes down -2.6%. And following a one-week delay, the BofE’s Monetary Policy Committee will now meet next Thursday (22nd), just before Friday’s (23rd) mini-budget from Chancellor Kwartneg — where hopefully we’ll see further detail on the mega borrowing requirements for Truss’s energy support package and tax cuts.

You get what you pay for

It was into this softer tone that Apollo launched Lottomatica’s new M&A deal, re-opening European High Yield 61 days after BestSecret offered the last Euro paper. Lottomatica (previously Gamenet) last tapped the market in November 2021, offering PIK Toggle Notes to fund a €375m distribution to shareholders.

This time round, the gaming operator was offering €350m Senior Secured Notes due 2027 (B1/B), adding ~0.8x EBITDA to gross leverage, with proceeds earmarked for pre-funding of future acquisitions. Gradually diversifying, the online segment of the business now generates over a third of group EBITDA, up from around 3% in 2017. And in line with further M&A ambitions Lottomatica is in negotiation with three targets, with an agreed purchase price of ≤7.5x EV/EBITDA on retail components and ≤11.0x EV/EBITDA for online — these projects (A,B,C) each generated €25-35m in the twelve months to June 2022. In addition, there are also €80m planned synergies with IGT’s Italian B2C Assets — acquired last year for €956m — which are expected to fully run through by the end of 2023.

Funded into escrow, bespoke control release conditions require only that (i) “at least 90% of the proceeds” are to be used “in connection with” a strategic investment or acquisition and (ii) pro forma leverage ≤3.25x — or as our legal team describes it, ‘broad drafting’ which offers ‘significant flexibility’ in how it can apply the proceeds. Also, the escrow mechanics allow the issuer to redeem any unreleased portion of the Notes at par, within 12 months from the issue date, with a six-month extension if acquisition documents have been signed within that 12-month period.

The OM does not specify that the target / investment even needs to be held within the Restricted Group, so the funds could arguably be transferred outside the Restricted Group to acquire assets via a parent, JV, Unrestricted Subsidiary or other affiliate. And while the pro forma ratio test helpfully offers some assurance, it’s set more than 0.8x above opening leverage.

Reportedly a ‘best-efforts’ deal, there was presumably no need for an OID, and so a suitably punchy coupon arrived with IPTs on Wednesday in the 10.00% area. This trimmed to 9.75-10.00% on Thursday before final pricing landed at the tight end at par.

The existing SSNs have ~2.75 years left to maturity and offered yields of 7.2-7.4% on Monday (8.0-8.3% as of today), suggesting a healthy premium on the new notes, even accounting for the duration mismatch. Probably in response to this, and the general dearth of new paper available, books were more than 3x oversubscribed. Meanwhile, yields on the 2026 PIK Toggles, offering just 11.7% YtW on Monday — have since widened to ~12.6% today.

Elsewhere, Norwegian debt purchaser and collector B2Holding also returned — offering four-year €150m Senior FRNs (B1/B+) — following a postponed transaction in November last year. Proceeds will pay down existing debt including a portion of the €249m drawn under the DNB / Nordea revolver. Indeed, DNB and Nordea, alongside Pareto Securities, are GloCos on the transaction which priced on Thursday at E+690 for par.

Looking ahead, as the TLB backing Bain Capital’s Inetum buyout progresses (PT, €300-400m, E+500, 90-91) we have the High Yield portion to look forward to early next week, with commits due on the loan next Friday (23rd September).

High Yield Secondary

In line with the broader macro news, Secondary instruments traded down an average of -0.93 pts (16% +0.61 pts | 81% -1.24 pts). As expected, Dollar debt took the largest hit (-1.64 pts), followed by Sterling (-0.91 pts) and then Euro-denominated (-0.62 pts) issuance. Similarly, the iTraxx Crossover widened out to 538 bps on Thursday’s close from 524 bps last Friday, having dipped to 508 bps on Monday.

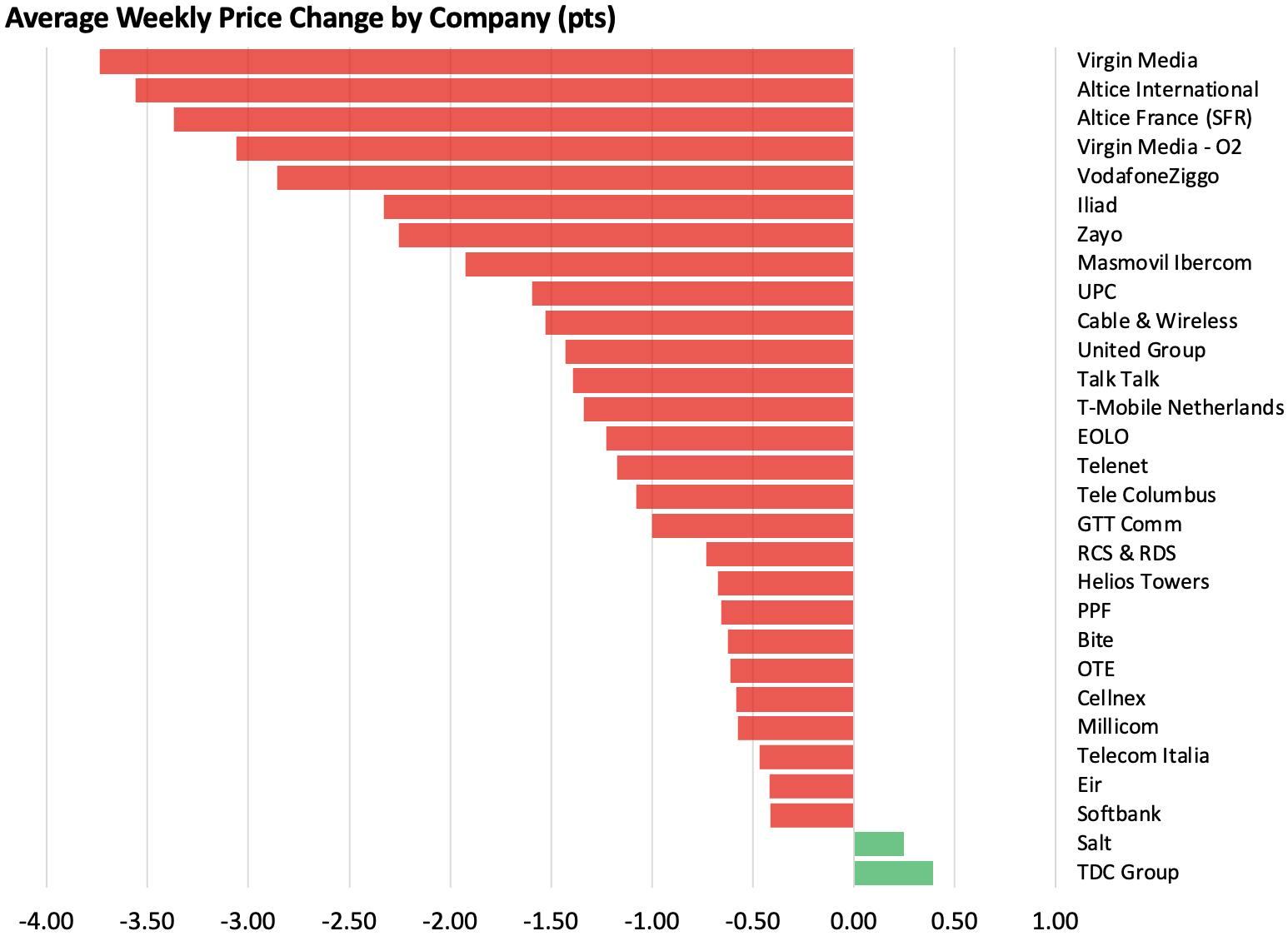

By Industry, Energy traded largely flat (+0.06 pts), with IT (-1.22 pts), Communication Services (-1.56 pts) and Healthcare (-1.58 pts) the largest downward moves.

Within Communication Services, Telecom names have been hit hard (-1.70 pts) — likely due to their longer dated structures. On a crude average Virgin Media (-3.7 pts) tops the list, led by a -5.9 pt decline on its SSNs due 2029. The 5.250% notes were last seen around 80, offering a 9.3% yield for the double-BB name.

In other single name moves, French care homes group Orpea’s 2025 and 2028 SUNs dropped -9.7 pts and -5.3 pts respectively. H1 results posted on Monday showed revenues up +10.9%, but an EBITDAR margin down to 18.5%. Operating profits have been hit by decreased Covid-19 support and the loss of non-recurring income specific to 2021, in addition to new cost pressures — energy as a percentage of revenue jumped to 2.9% in the first half, compared to just 1.9% in 2021.

Very few names managed meaningful positive gains on the week (just 2.5% names covered were up more than +1 pt). One of these however, automotive seals supplier Standard Profil, saw its2026 SSNs gain a further +2.6 pts, now +8 pts since Q2 earnings in early September. Raw material cost inflation is mostly passed through, OEM production schedules are robust, and importantly, the car chip shortage is easing.

Leveraged Loans Primary

Primary is back in action, but as one buysider said: “We’ll see how long it lasts for.”

Indeed, it feels like we’re waiting for primary to die again, just as it is sputtering back to life. Buysiders feel the credits coming to market aren’t worthy of their time, or are just small add-ons, and with banks and direct lenders taking chunks of syndications, if not entire deals, it’s difficult to get that excited.

Even Inetum, an IT services firm backed by blue-chip sponsor Bain Capital, will now have a debt financing that includes a TLB, TLA and a senior secured bond — a recut from the original TLB capital structure, as reported.

BNP Paribas and Credit Suisse are guiding a €400m TLB at E+500 bps with a 90-91 OID. The new structure gives 4.4x senior secured leverage, going down to 3.9x if working capital financing is excluded, said two buysiders.

“We passed on Inetum given its low valuation and potential for earnings misses, although the yield may be attractive for some,” said the second buysider.

Deals currently being pre-sounded are struggling to gain good traction. To get done, OIDs still need to be in the low 90s and a 5-handle is a pre-requisite, which makes it tough for sellsiders to get clients to issue. One sellside originator said they felt it was doubtful they would close another deal by the end of the year.

The market’s reopening deal for Accell, a Netherlands-based bicycle manufacturer, has now closed, but its progress does not bode well for the market.

The €700m 2029 TLB priced at E+500 bps and a 94 OID, after guidance of E+500 bps. Bookrunners Deutsche Bank, Shinhan and RBI did not disclose OID guidance, but 9fin revealed it was expected to be offered at between 93 and 94.

The book built well, with almost 50% of the paper taken on by banks early on in the process and as of Wednesday (15 September), leads had around €200m of IOI orders on the remaining portion.

Nevertheless, buysiders speaking to 9fin were overall negative on the credit, with six declining the deal, and a further two undecided 24 hours ahead of commitments on Wednesday.

“This deal is like a textbook case study of what not to do in credit investing,” said a third buysider. “Unfortunately it will be another data point for underwriters to avoid the European loan markets right now. I wish they would bring something better to open markets.“

Docs were also a thorn in buysiders’ side with lenders complaining about a “lenient” J Crew Blocker, among other issues.

The deal was marketed on €157.2m of LTM (June 2022) adjusted EBITDA for 4.6x and 4.4x gross and net leverage respectively. See here for the full loan preview.

Will the other deals in the market fare much better? KronosNet, the new name for the merged entity of Comdata and Konecta, is also in market in the low 90s (talk is 93 area), with E+575 bps price talk on a €450m TLB.

The pair of Southern European call centre businesses have a troubled history. Comdata was in a restructuring process for years, and the combined business has a great deal of exposure to emerging markets, particularly Latin America.

A fourth buysider said they were unlikely to get involved given the nature of the business alone, while the fifth buysider is a bit more hopeful. They noted the strain of Comdata’s history, worrying that it may repeat itself, but felt the merged business’ recurring revenues, low churn rate and “great” revenue visibility could be enough to lure them in. ICG’s backing is considered positive as well.

Comdata issued a €355m TLB with a E+500 bps margin back in 2019, while Konecta’s €100m and €320m TLBs each have E+500 bps margins and priced at 98 and 99, respectively.

Also in the market is Rovensa, an agricultural biochemicals business, with a €387m add-on due 2027. Price talk on the deal is currently E+525 bps with a 94-95 OID and a 0% floor. The tranche is non-fungible with a €520m TLB that priced at par with an E+375 bps margin.

The company has boosted its €115m RCF up to €165m in this transaction, of which €28m is drawn.

Ratings agencies expect the acquisition of Cosmocel to bring diversification and scale to the business. Rovensa, being a true Iberian company, with dual headquarters in Madrid and Lisbon, will be making the jump into Latin America with this Mexican buy.

Partners Group, alongside minority existing investor Bridgepoint, bought Rovensa in 2020. The business generated adjusted EBITDA of €172m, pro forma for the acquisition, to June 2022.

Finally, TenCate Grass, a sports surfaces manufacturer, is issuing a €274.3m add-on fungible with its €315m TLB, issued in October 2021. The original tranche priced at 98.5 with a E+500, and while the add-on will have the same margin, OID guidance has not yet been disclosed. The add-on is rated B2 and will support the acquisition of US-based Hellas.

But even as primary struggles back to life, direct lenders continue to take market share. LPC reported this week that Ares Management will be providing a €400m unitranche to support BC Partners’ acquisition of Havea, a health products and supplements manufacturer currently owned by 3i.

Leveraged Loans Secondary

The flipside to a primary market with attractive OIDs, even while credit quality may be mixed, is that secondary opportunities become less exciting, said the fourth buysider.

To take Inetum as an example, of the 122 loan tranches in the IT sector, only 12 are currently indicated at below 90-mid. Only eight of the 110 tranches indicated above that level has a 5-handle.

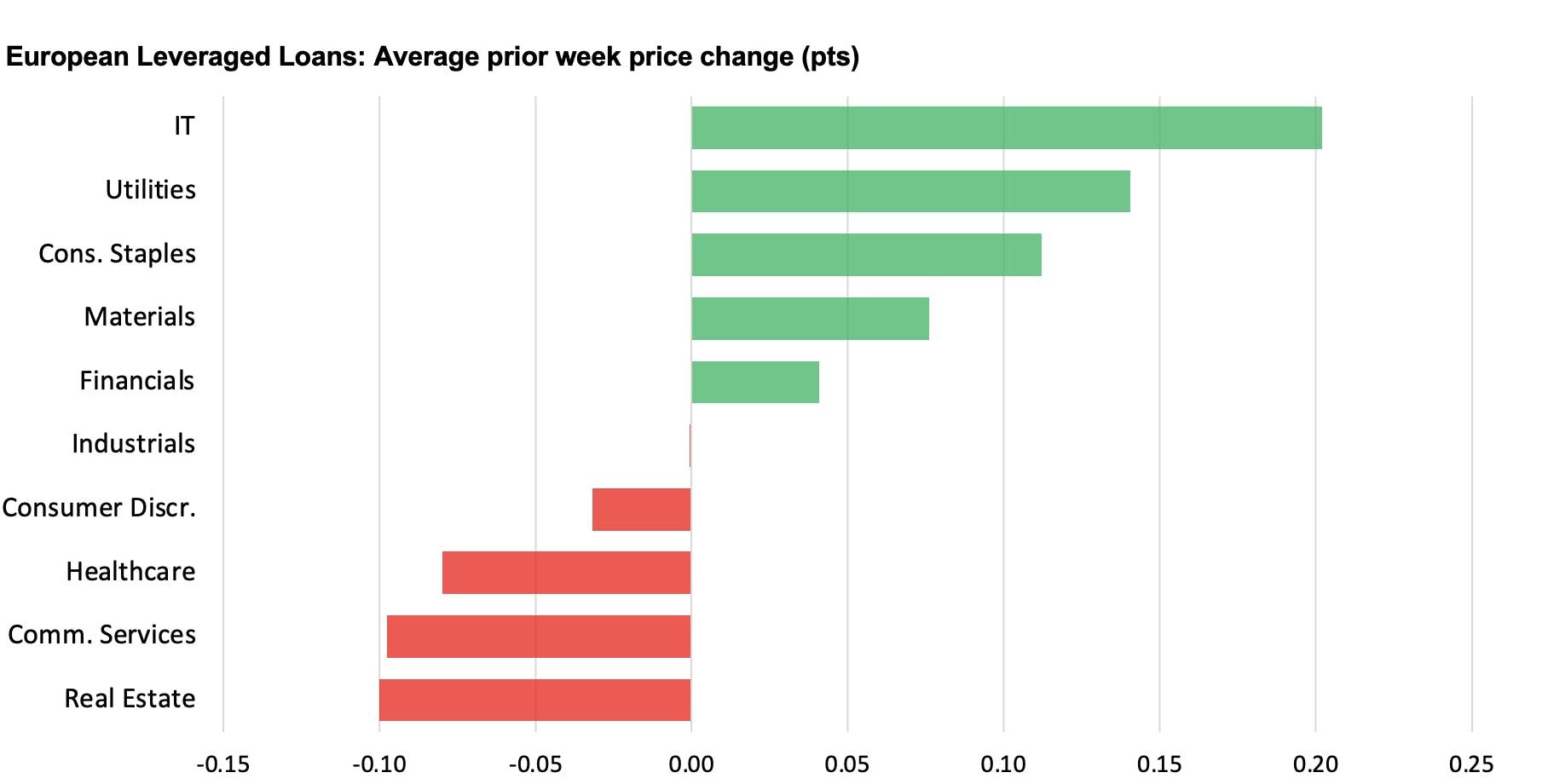

Indeed, the market has seen a fairly positive week, with very marginal improvement in IT, utilities, consumer staples, materials and financials. Even drops in real estate, communication services, healthcare, consumer discretionary and industrials were less than a tenth of a point.

Some individual credits saw much more dramatic downfalls. Cineworld’s €607.7m TLB paying a E+262.5 bps margin dropped a dramatic 9.7 pts this week Its creditors’ lawyers and advisors negotiated a revised agreement in bankruptcy court in order to keep the movie theatre chain operating, after an initial DIP loan proposal was deemed unsatisfactory. Clients can see a full update on the court proceedings here. 9fin has recently published a Restructuring QuickTake on Cineworld which clients can view here. If you are not a client but would like to request a copy, please submit your details here.

The US/UK cinema group filed for Chapter 11 on 7 September 2022 in the Southern District of Texas bankruptcy court.

Constellation has also had something of a car crash this week, after earnings were less than satisfactory. Its 2028 €400m TLB, 2028 £400m TLB and its £325m second lien, each dropped 8.7, 8.5 and 7.3-points, respectively.

The first buysider was bullish on the UK-based car auction business during the summer, feeling more comfortable with the used car market than new production, but still buysiders were taken aback by the company’s earnings this week. Q2 EBITDA dropped to almost a third of what it was in Q2 2021. Nevertheless, the two buysiders feel confident in the owner of webuyanycar.com, expecting Q3 and Q4 to be far superior to Q2.

BWIC activity has also taken an upturn. Bids were due on Tuesday, 13 September on a €64m portfolio of loans, the largest tickets of which were €5m slices of Masmovil and Biogroup while the rest of the BWIC included €3m pieces only.

In total, it included 21 euro-denominated loans, with a mix of more resilient names such as Verisure, Masmovil and Biogroup, but also a number of food / retail credits that have recently experienced cost input pressure like Prosol and Upfield (Flora). Clients can visit here for the full list.

A slightly more varied list of tranches hit the auction block on Thursday, 15 September. The circa €70m-equivalent portfolio of secondary loans and bonds comprised seven bonds and 21 loans, mostly in euros, but with some sterling tickets. The biggest tranche was a €5m second-lien piece of TMF Group. Clients can see here for the full list.