This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

The quieter tone of last week rolled over into primary once again. June 2021 numbers went stale for 144a issuers last Friday, and we tracked just two RegS-only deals on Monday, followed by Pinewood on Wednesday. Zooming out, European countries have begun to increase restrictions on fears of a resurgent wave, focusing on unvaccinated populations. Also, after the hairy 6.2% US CPI inflation print, there was another beat as the UK announced CPI inflation of 4.2% YoY, more than double the BoE target, and a near ten-year high.

Discounters dividend

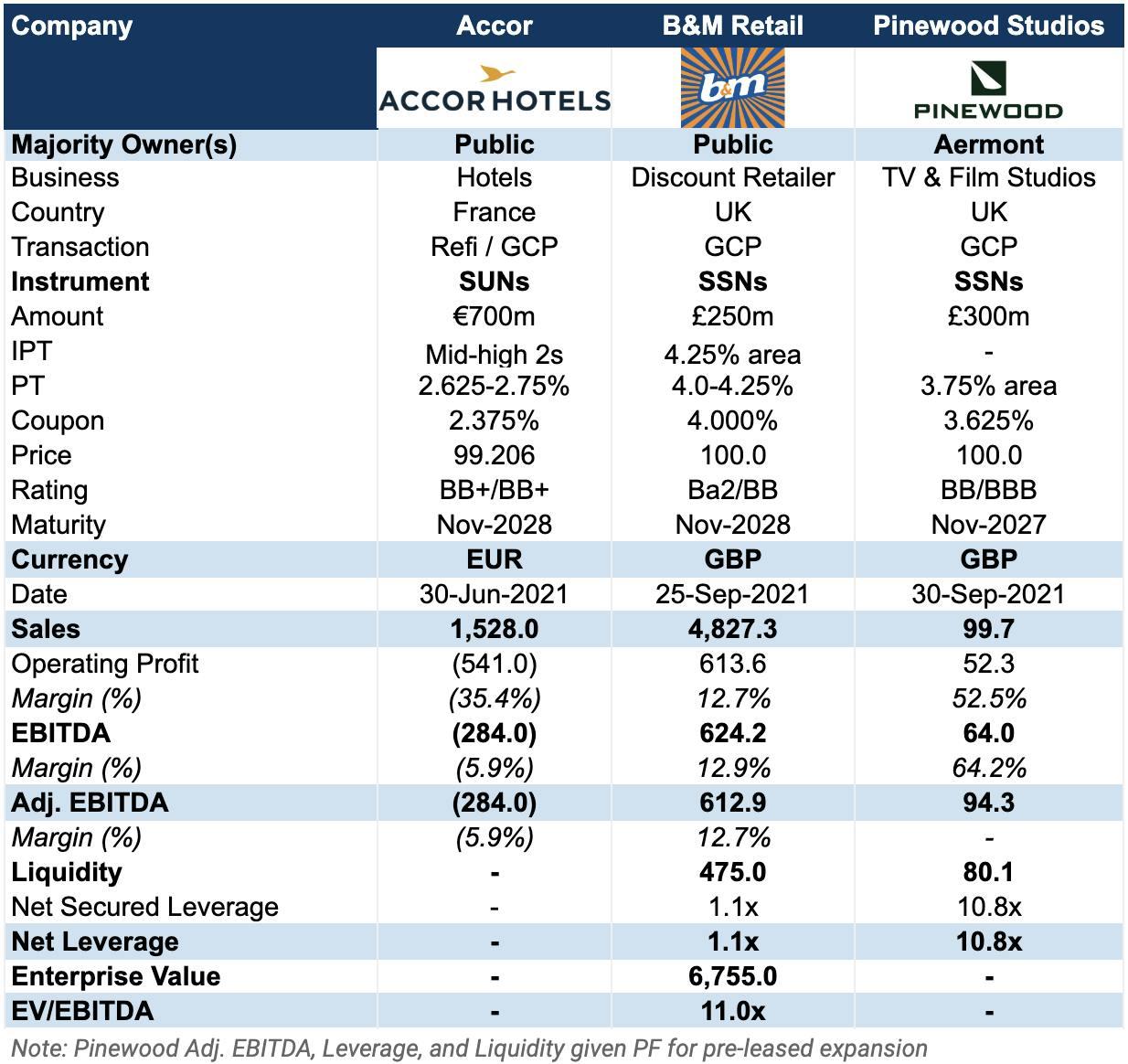

In spite of the relatively dry week for High Yield, Sterling supply was topped up by a new offering from UK-based discount retailer B&M. Marketing £250m in Senior Secured Notes due 2028 (Ba2/BB), proceeds will be used for general corporate purposes, or a special dividend up to the principal amount. If the entirety of the offering was paid out this would increase leverage by 0.4x – although this unlikely a concern – it would still leave £90m of cash on the balance sheet, and an enormous equity cushion of more than 90%.

In the H1 results call (11 November), management were unconcerned about recent price rises, suggesting shrinkflation as a solution “a packet of six socks might become a packet of five socks”, or simply passing the small percentage increases on already low cost goods through to customers. New UK wage increases will present a cost increase, but management were keen to point out that its key customers were those benefiting from higher pay, so some of it will return to the tills: “Without putting it too bluntly, those members of the public are not going to be spending it in Harrods”.

Pricing emerged on Wednesday, and tightened from IPTs in the 4.25% to land at 4.00% – a slight premium over its larger, and shorter tenured £400m 3.625% SSNs due 2025.

Burning cash

There were more Sterling Notes from film and television studio group Pinewood, who will use the £300m 3.625% Senior Secured Notes due 2027 (BB/BBB), and £218m of cash on balance sheet to fund expansion at Shepperton Studios and five new stages at Pinewood West. Including the new expansion at these sites, the adjusted freehold valuation of property would be £2,672m, or a net LTV of 38%. The group has two existing long term leases with Disney and Netflix, both of which make up substantially all of EBITDA. Netflix has also signed a new lease for the majority of Shepperton South’s expansion. The deal wrapped up same-day at the tight end of IPTs – and before news emerged of a fire breaking out at one of their sites in Iver Heath.

Aside from a drafting error in the preliminary OM (which would exclude the existing SSNs from the Secured LTV ratio), there is portability at a net LTV below 50%, and covenants appear to be structured for some sort of exit event – either an IPO or sale.

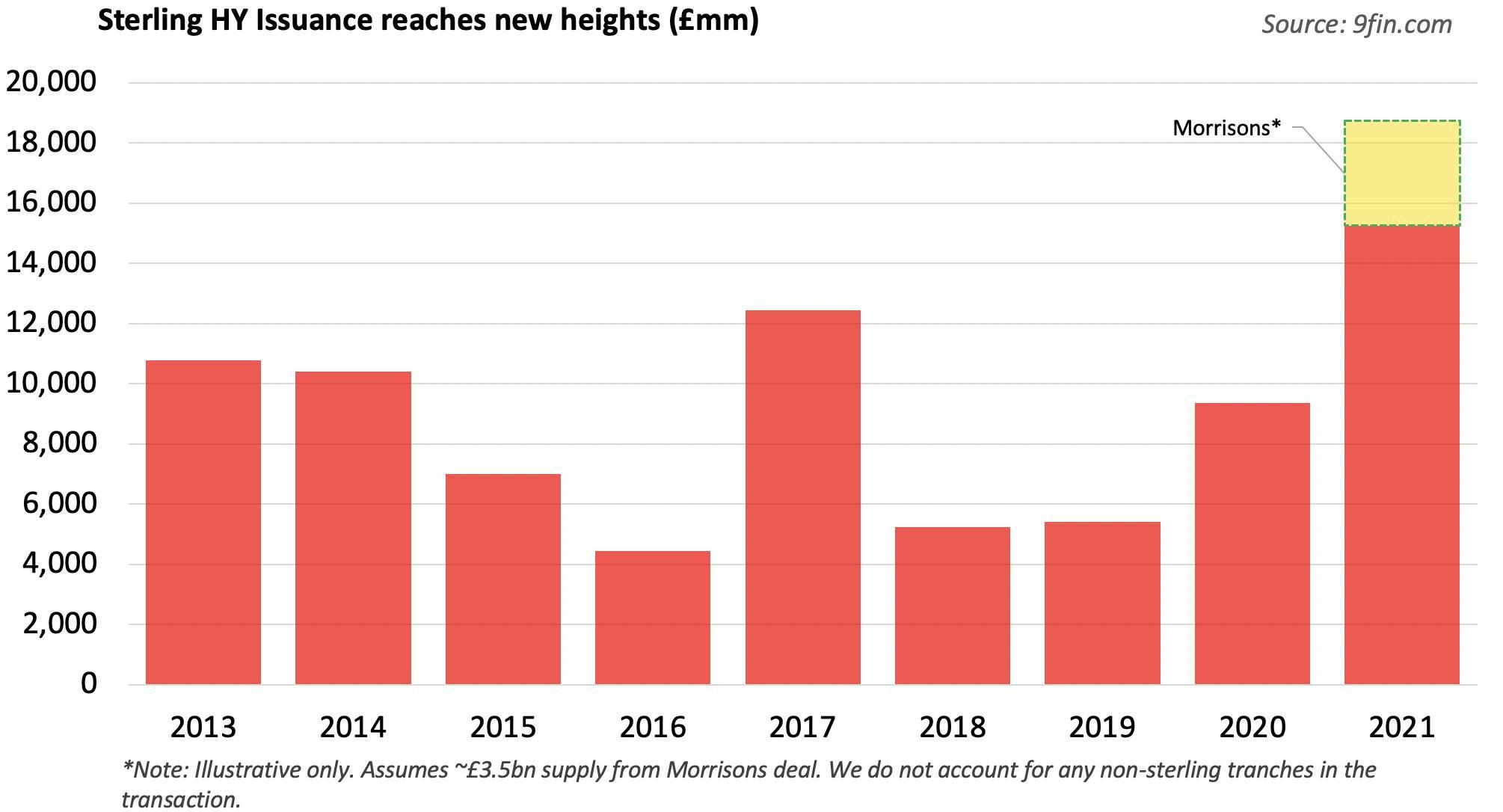

Adding to these issuances, Morrisons is expected to launch it’s £6.6bn LBO by CD&R in the coming weeks. Even without the Morrisons contribution, over £15.2bn has been printed already in high yield, so far exceeding 2017’s £12.4bn.

An industry leader on decarbonisation, the group has strong science based targets in place, aligned to the Paris Agreement – it was even the first major international hotel group to set net-zero SBTi aligned targets. The two KPIs include; a 25.2% cut in Scope 1 & 2 emissions by 2025 (base year 2019), and a 15% reduction in Scope 3 emissions by the same date. A 0.125% margin step-up will apply for each target missed.

Leveraged Loans Primary

Is it beginning to look a lot like Christmas? Certainly in our leveraged loans snow globe, buysiders are hearing jingle bells and the accompanying primary calm. Two buysiders agreed in the last few days the 2021 primary barrage may have finally come to a ceasefire for the year. “We’ve seen opportunistic things still coming to market,” said the first buysider, “but big M&A is a bit quieter and could be done for the year.”

A third buysider also agreed that with such little dealflow coming through this Monday (15 November), we were certainly nearing the end of the year, despite banks maintaining there are a few more deals to come.

Sellside bankers may be referring to the mammoth Morrison’s deal, which was expected to barrel onto the scene towards the end of November. On 12 November, GLAS announced it was the security agent for the expected £6.6bn syndication, which will see CD&R take Britain's fourth largest supermarket private.

Mad for add-ons

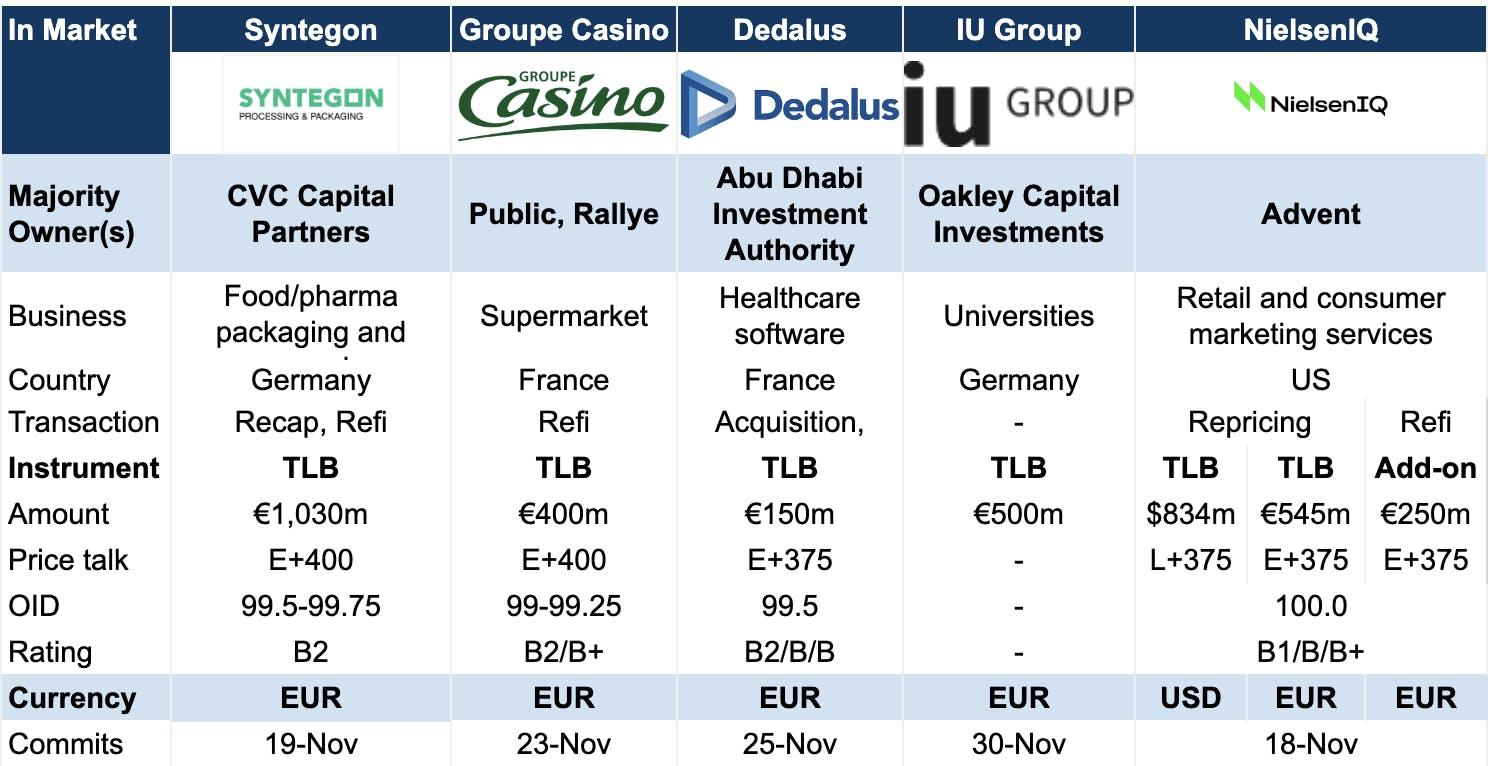

Opportunistic add-ons mentioned by the first buysider came from two well-known levfin operators, NielsenIQ and Dedalus. The former, a carve-out from the customer research behemoth Nielsen, is repricing its loans and adding cash to the balance sheet. Dedalus, touted as a “straight-forward story,” came to market this week with its second add-on of the year. Even despite a data leak earlier in the year, the B2-rated company has guided the add-on at E+375 bps. See our June 2021 preview here.

Groupe Casino is also in the market with an add-on, this time raising an extra €400m off the back of its existing €1bn TLB. The financing will go towards a tender offer for its bonds with maturity dates in 2023 and 2024, according to a report by LPC. See here for details of all of Casino’s instruments.

While all three have yet to allocate, the credits should prove easy fodder for analysts who have already done the research on these well-worn names.

Patterned tights?

Pricing was in flux this week, with the gains made in average pricing in the past month or so being held in some deals. As the first buysider said: “I’d say pricing has plateaued at around E+375-400 bps. If someone was to come to market with E+350 bps, we’d have to think carefully about it.”

However, pricing also snapped back into the tight positions we’ve experienced all year on some deals, encouraging market participants to question the permanence of improved pricing. The second buysider said: “Pricing has got better, but a couple of deals have tightened this week. One I worked on should have come wider.”

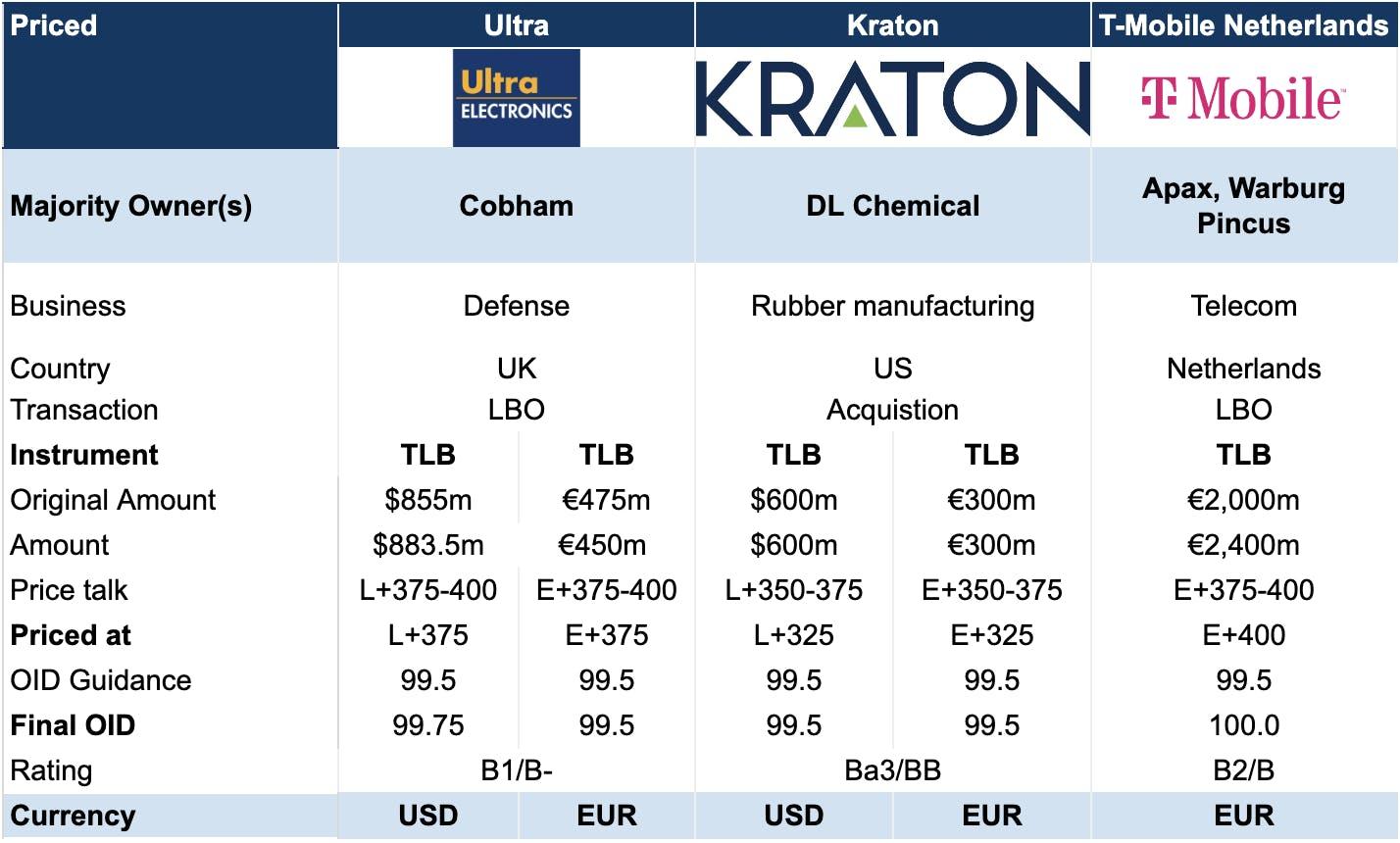

Allocating this week, Kraton’s sponsorless transaction achieved margins tighter than its guidance, though buysiders looking at the deal noted that initial price talk was strong, related to its credit rating. Kraton, which is to be acquired by DL Chemicals, offered the lowest leverage of any deal this week, though this was tempered by weak historic financials and exposure to raw materials volatility. Clients can see our loan preview here or request a copy here.

Also on the tighter side this week, was the market’s largest deal: T-Mobile Netherlands. The telco lacks hard assets and is piling on debt to fund the buyout, but it’s size, stability, and healthy cash flow all led to a smooth syndication, which saw its OID tighten to par. Clients can see our loan preview here. If you are not a client but would like a copy of this report, please sign up here.

The process kicked off with extremely issuer-friendly documentation, but the sponsor buckled in syndication to add a ticking fee, lower its ESG ratchet and reduce the senior secured net leverage ratios associated with debt incurrence and portability, among other changes. Clients can see our full summary of T-Mobile Netherlands doc changes here.

Agro docs and ESG shocks

Aggressive documentation was a theme of the week, as much as it has been of the year. Syntegon had its docs called out by six buysiders as aggressive. A fourth buysider has told 9fin the issuer will decrease the number of margin ratchets as well as the associated leverage, remove the inside maturity basket and lower the restricted payments basket ratio, though they have not yet included a ticking fee.

The packaging machinery business offered one of the more complex credits in the market this week, with two buysiders reporting late nights spent trying to navigate the business’ equity-stripped capital structure and cost savings programme. But despite this, the process is said to be going well, according to buysiders. The margin and OID will price at the tight end of guidance, according to the latest update seen by 9fin. See our loan preview here.

Buysiders also complained of greenwashing on the Syntegon deal, but the biggest ESG offender of the week was, by far, Ultra Electronics. As a quasi-acquisition for controversial Cobham, buysiders were confused by the rationale of the merger, but involvement in weapons manufacturing was the real obstacle for most here. Despite this, some lenders found solace in Ultra’s limited exposure to offensive weapons and the latterly tightened documentation, and the deal priced at the tight end of initial E+375-400 bps guidance. See our loan preview here.

High Yield Secondary

Softening slightly, instruments traded down again this week, -0.10 pts on average (39% +0.22 pts | 57% -0.33 pts). All Industries were in the red, although Real Estate, Financials and Utilities only just. At the lower end we saw Industrials (-0.16 pts), IT (-0.17 pts) and Energy (-0.25 pts). Elsewhere, the iTraxx European Crossover was steady versus last week, tightening just 1 bps to 246 bps.

The fall in Energy was largely driven by Tullow and Enquest, both of which released trading updates this week.

Enquest admits “group production has been challenging”, mostly from performance at Magnus, a recent unplanned shutdown at Kraken, and a supplier driven delay in the pipeline replacement in Malaysia. Average net production to October 2021 has fallen to 44,306 beopd, with production for the year estimated at around 45,000 – below the previous guidance of 46,000-52,000. The Senior Notes have fallen to ~97.3, from around 99 on Tuesday.

Tullow’s SUNs due 2025 fell around -1.5 pts to 85.7 after the release of its November trading update. On 11 November, Tullow exercised its right of pre-emption related to the sale of Occidental Petroleum’s interests in the Jubilee and TEN fields in Ghana (equity interests expected to increase to 38.9% and 54.8% respectively). Rahul Dhir comments this underscores “our belief in the value and growth potential of our assets in Ghana”. Tullow continues talks to find a partner for its $3.4bn onshore project in Kenya, with a final development plan expected by the end of the year. Full year guidance remains unchanged at 58,000-61,000 boepd.

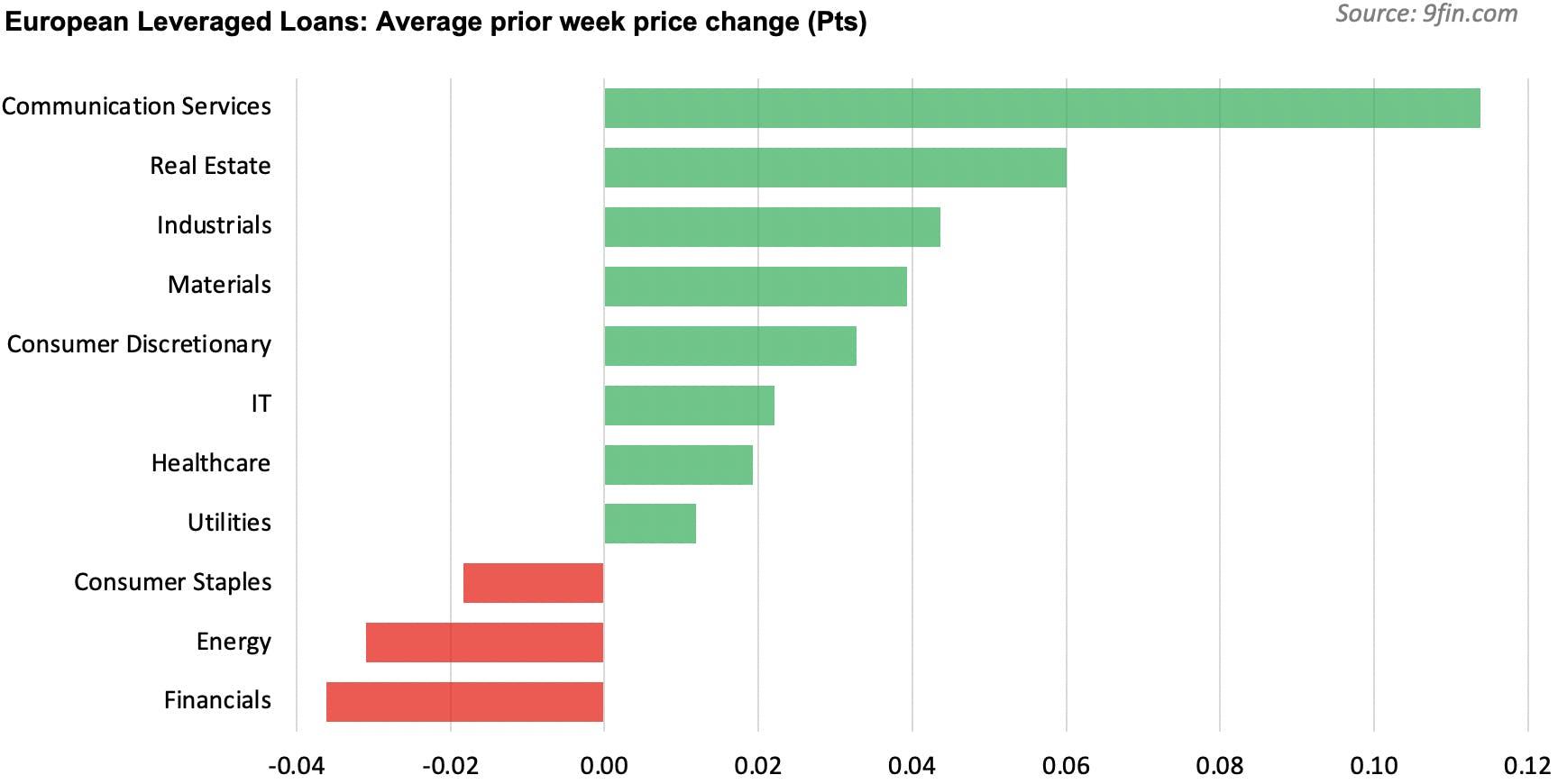

Leveraged Loans Secondary

Once again, secondary took a back seat for many buysiders this week. Said the second buysider: “Between earnings, focusing on primary and doing end of year reviews, there’s not really been any time to look closely at secondary.”

But even for those who have had the time to look, the secondary market doesn’t look particularly lustrous. The first buysider said: “We’ve just been picking through secondary, and we don’t there’s much value in secondary right now. The Covid names, even the theme parks, are back in the high 90s.”

Buysider apathy for secondary names shows in another flat week for the market. All sectors remained essentially stable save consumer staples, energy and financials, which all declined less than 1 pt.

Genesis Care was our biggest faller this week. Its €400m and €500m tranches fell by almost -2 pts and -1.5 pts, respectively on the back of “weak earnings and cash flow and elevated leverage,” according to S&P. The tranches’ indicated price began to fall from around par on 28 October, as the Australian clinics operator geared up to report “materially weaker” earnings, according to S&P, due to weak recovery in its US business and lower patient volumes due to the pandemic. The tranches are now indicated at 94.5 and 98, respectively.

Praesidad was a highest riser this week, closely followed by Cineworld, and these were the only two credits that rose more than a point this week.

Praesidad, a security systems and products manufacturer, has steadily risen out of its previously distressed position in the 50s, back in the early aftermath of the Covid-19 pandemic. The €290m tranche is now indicated at 91 off the back of ratings upgrades and “comprehensive restructuring efforts ... which will support profitability improvement over the next 12 months,” according to Moody’s.

The LevFin Wrap is published weekly for 9fin subscribers and includes our Forward Pipeline. If you would like a copy of our Forward Pipeline, sign up here.