This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

LevFin Wrap — Awaiting the reopening; Secondary starts strong

David Orbay-Graves

+Michal Skypala

+ 1 more

•6 min read

New Year’s hangovers may have been shaken off, but reopening trades in the European high-yield credit market are yet to emerge — likely holding fire due to the short working week and some European countries still being on holiday (Greek, Syrian and Orthodox Christians have Christmas on 6 or 7 January — Merry Christmas to any readers celebrating today!).

In terms of what’s in the pipeline, we’ve already got an indication that unrated airline Air France-KLM could be the first to issue a bond, with the airline expected to price a €300m sustainability-linked bond in the near future. Proceeds are earmarked to repay state loans granted during the pandemic.

“We don’t see much [imminent issuance] on the bond side,” said one levfin banker. “It will more come from loans […] not much though. Next week will not see a huge number, even fellow banks are not into immediate offload [mode].”

As previously reported, the number of M&A-related LBO financings in the pipeline has dwindled, leaving most activity in the refinancing space (alongside increased volumes of amend-and-extend and exchange transactions).

“There are not very many M&A processes happening at the moment — we are open for business in underwriting, but we’re going ahead slowly and taking some time. There is a mismatch between what issuers and sponsors might want to do, and what you can do,” the banker continued.

Most of the hung underwritten debt from large LBOs last year has now been offloaded, they added.

One buysider told 9fin that they are mainly being pre-sounded on A&E transactions for loans, with some expected to come next week, potentially in the pharmaceuticals and telecoms sectors. However, the market is not fully back yet, they cautioned, adding that the success (or otherwise) of these A&E transactions will depend on the specifics of the credit.

Meanwhile, new CLO issuance in December means there will be some good demand for loans, said a second buysider, who added that they expect some deals to start filtering through next week. “The market is positive enough to digest them – but I’ve been told that there was potential for decent new issuance in a week or two a lot of times in 2022 and it has not always happened!”

Secondary off to a good start

The first few days of the year proved constructive for European high-yield credit. The iTraxx Crossover index tightened 34 bps to 440 bps in Tuesday and Wednesday trading, before widening slightly to be indicated at 445.5 bps at time of writing. US high-yield credit fared slightly less well, with the CDX HY coming in 15bps to 469.75 bps by Wednesday, and is indicated at 473 bps at time of writing.

European credit may have benefited from some unwinding of pre-Christmas hedges, and lower than anticipated CPI prints from Germany and Spain. Data published on Tuesday showed German consumer prices rose 9.6% YoY in December, compared to analysts’ consensus view of 10.7%. Meanwhile in Spain, consumer prices rose 5.8% YoY in December.

Meanwhile, European wholesale natural gas prices fell to their lowest level since the Russian invasion of Ukraine on Monday as the abnormally mild winter continued. Dutch TTF gas futures, which hit as much as $367/MWh in March, were quoted at $77/MWh on Monday.

The positive noise in Europe can be contrasted with the US, where the fear of recession continues to weigh. Nonetheless, bear in mind that this week’s tightening in the iTraxx Crossover is effectively just returning to its mid-December level (434 bps on 14 December) prior to a late-year widening.

Movers and Shakers

There were no particularly dramatic price moves in the European high-yield space this week. Among the bigger losers were DIC Asset AG’s €150m 3.5% 2023 SUNs, which widened 116bps to a STW of 1.9% and Victoria PLC’s €250m 3.75% 2028 SSNs, which widened 79 bps to a STW of 7.2%. The only credit-specific newsflow on either was DIC Asset’s announcement that it had disposed of its Kaufhof Chemnitz department store, bringing total disposals in 2022 to around €400m.

One of the more eye-catching names tightening this week was UK-based specialty chemicals company Synthomer, which saw its €520m 3.875% 2025 SUNs tightened 86 bps to a STW of 2.9%. As 9fin wrote late last year, while the company’s divestment of its laminates and films unit will reduce Synthomer’s debt load slightly, more meaningful deleveraging remains dependent on its ability to sell other non-core assets at attractive valuations.

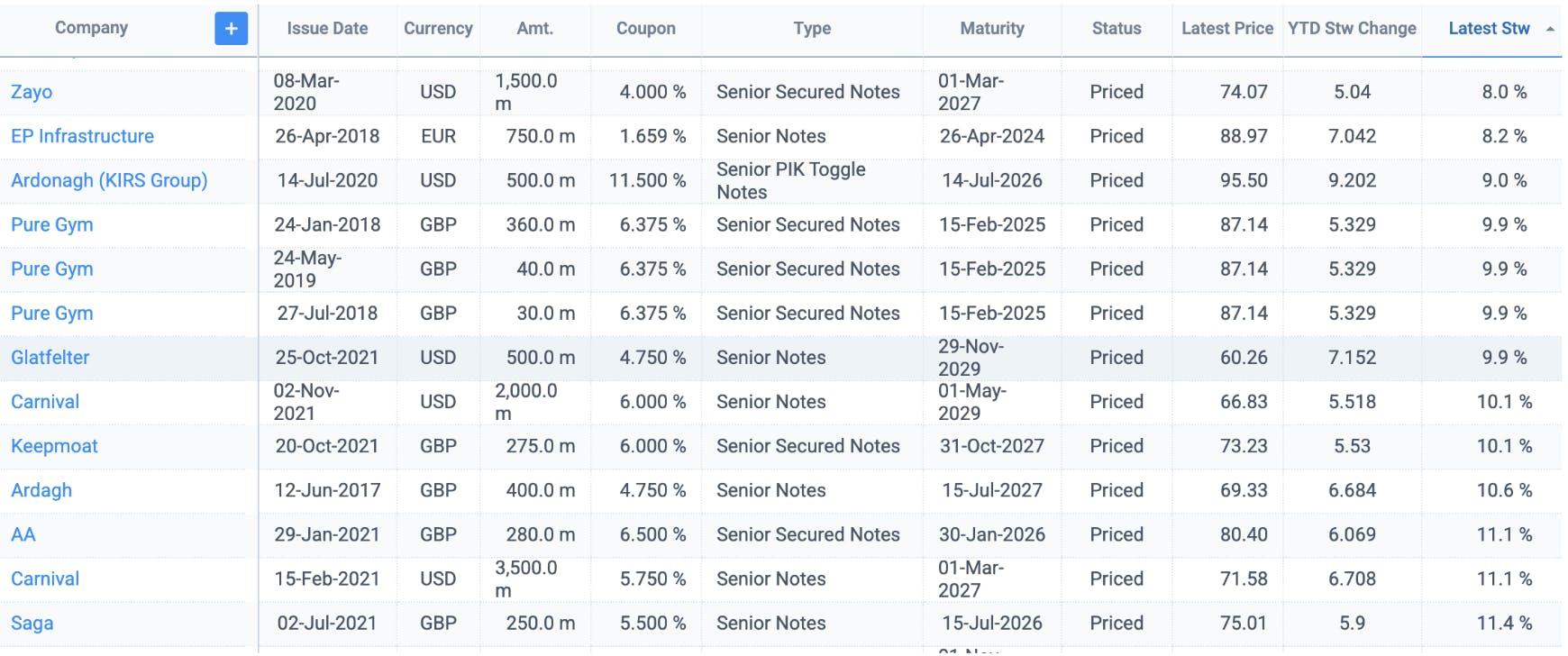

Excluding stressed credit (STW < 10%), the following euro-denominated fixed-rate bonds saw some of the biggest week-on-week moves in spread to worst (STW) terms, according to 9fin’s European price moves screener.

HY spread risers (price declines)

HY spread decliners (price risers)

A year to forget

Last year was one to forget. In term of returns, high-yield credit lost 11% in 2022, making it the asset class’s second-worst year on record behind 2008, according to a BofA Global Research report. Sectors hardest hit were media (-17%), healthcare (-16%) and cable & tech (-15%), said BofA. Relative outperformers were capital goods, metals and energy.

But despite expectations that market volatility will persist into 2023 (potentially posing a threat for those with near-term maturities), corporates are going into the year with remarkably robust fundamentals (something Man GLG’s portfolio manager Michael Scott previously highlighted in this column).

“Debt leverage has never been lower in [high-yield] than it is today – net at 3.6x and gross at 4.0x are record lows. Interest coverage is at all-time highs of 5.8x, although likely to drop,” said the BofA report.

Nonetheless, spreads are generally expected to widen further before coming in again. In a research note published on Friday, analysts at Barclays Bank wrote: “We expect a peak in spreads of 650bp in H1 largely driven by greater dispersion as a result of earnings deterioration, before spreads tighten back to 500bp by the end of 2023.”

“Our meetings with a large number of real money and hedge fund clients in December suggest that investors are somewhat caught between having a pessimistic view on credit near term given the growth outlook and earnings deterioration, especially in the context of where valuations are, but also conscious of what is technically still a strong market and with the expectation that default rates will still remain low in an historical context. Subsequently, the dispersion in views for 2023 is among the largest that we can remember to start a year,” the note added.

Deutsche Bank capital add-on

Slipped out just before New Year was Deutsche Bank’s announcement that the ECB had imposed a 20 bps capital add-on linked to “the ECB’s newly introduced separate assessment of risks stemming from leveraged finance activities”.

Deutsche Bank is way over the ECB’s minimal capital requirements, so it’s not like it has to go raise equity to cover it… but 9fin’s Owen Sanderson worked through some of the maths, and it’s a pretty serious slap on the wrists — potentially more than doubling the capital allocated against the levfin business.

That kind of capital hike could be very damaging to DB’s market position in levfin, if the business has to eat it all themselves, but given Deutsche CEO Christian Sewing’s vocal opposition to the ECB’s approach, it’s likely the leveraged business gets some help from head office.

Besides, Deutsche has also been beating a tactical retreat from parts of the market. Sewing said on the bank’s third quarter earnings call that “on origination and advisory in Leveraged DCM, we gave up market share, but kind of on purpose, because we already slowed down our underwriting at the end of Q1 or in Q2. And therefore you see that in new underwritings that we’ve reduced market share, but that is an on-purpose behaviour. We can also see it now, when I look at the pipeline and the commitments we have out there and the losses we have taken, I think this was the right strategy.”

He continued: “By the way, to be very clear, we will stay in that business. That is a very important business. You will have seen some announcements last week that we will adjust our internal capacity to the volumes we see. But this is a very important business on the financing side. It feeds other businesses like the M&A business.”