This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Friday Workout - Delta Force meets irresistible HY; Austrian Residential Evils; Deliverance for Provident

Chris Haffenden

•17 min read

The force the Delta variant is spreading around the world is having little effect on the object of High Yield issuance which is very much in motion. Covid-affected industries such as hospitality and travel remain readily received by investors, marketed on 2019 numbers. After Pizza Express last week, Sani/Ikos - the luxury Greek all-inclusive hotel business was the next one to bask in the limelight.

European reopening in June/July was supposed to save the summer of 2021 for travel operators. But the Delta variant’s exponential rise (42,000 cases in the UK yesterday) has cast doubts on the ability to take summer holidays. Despite the best attempts of Boris Johnson to fully open up as the school holiday’s approach, our European neighbours are more cautious, with France, Netherlands, Greece, and Spain all announcing new restrictions this Monday. So even if we are able to travel from a UK perspective, our neighbours are less accommodating (pun intended) on the other side.

On a related note, grey-haired travellers such as myself may be turned away at the borders, as 5m Britons received the Indian-made version of the AstraZeneca vaccine in March which has not been approved by the European Medicines Agency. Italy’s loss is Scotland’s gain for my household.

HY juices equity returns

Last week, we mentioned a few top of the market indicators. I would add another - bondholders taking equity risk for bond returns while funding future projects, a charge levelled by some investors looking at the Sani/Ikos deal.

A great prior example was Sirius Minerals which sought to find HY buyers in 2019 to fund revolver draws for its polyhalite mine in North Yorkshire. The deal had a 1096-page OM (28 MB), but that wasn’t the only difficulty for investors to digest. Many viewed the potash substitute miner drilling a 30km tunnel under the sea as a more likely candidate for project finance with an accompanying government guarantee. Management had told investors this route would take too long to secure. There was another reason however, the RCF had a security demand feature that required additional HY bonds for each $500m draw that was made.

In the end, even 13-15% yields failed to entice buyers to fund the project which required $3.5bn of total capex and wouldn’t produce any free cash flow until 2024. The company admitted defeat that September and eventually ended up in the arms of Anglo American.

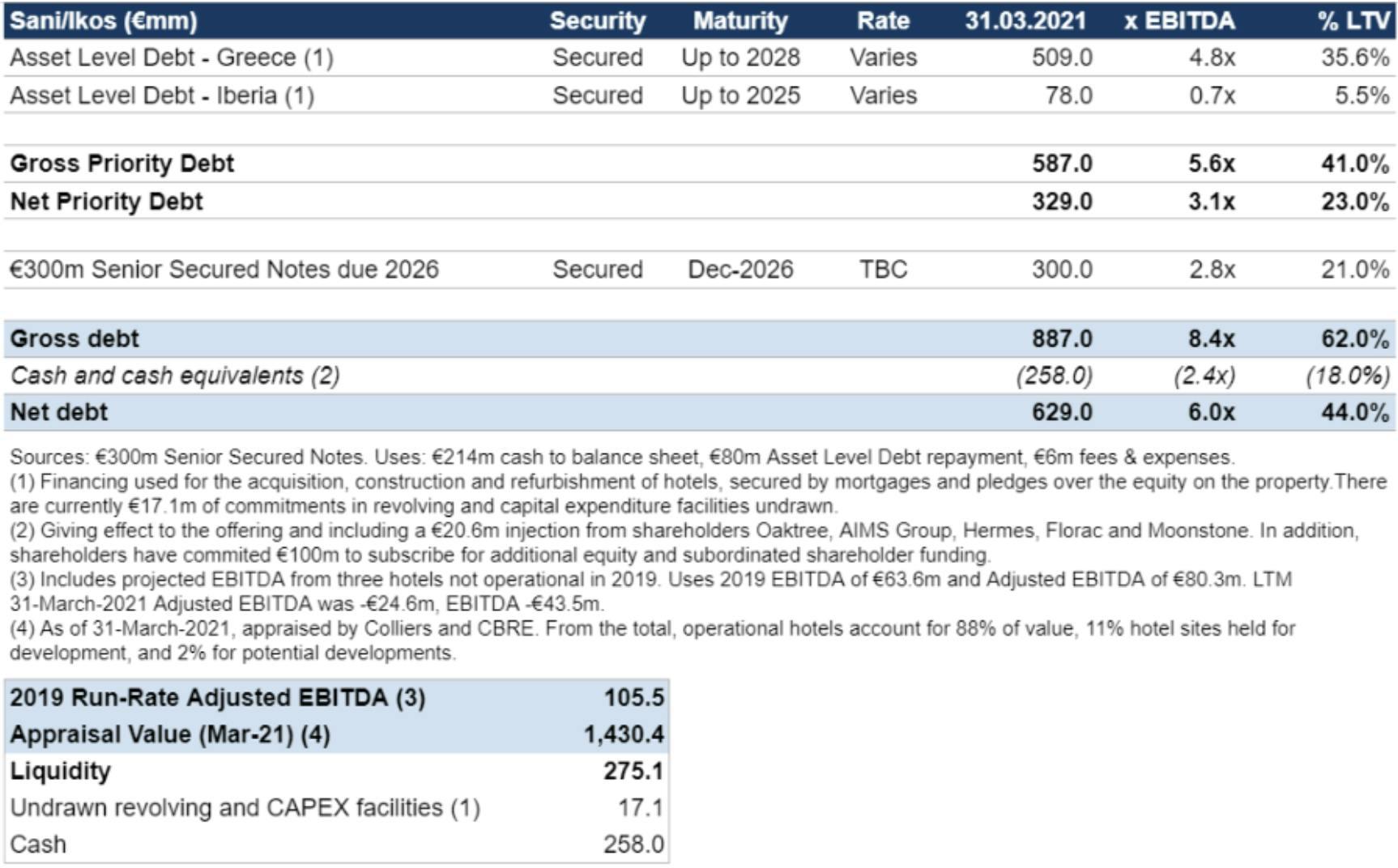

Sani/Ikos operates a portfolio of ten five-star luxury resorts with another two under development, including the Five-Star Sani Resort in Hlakidiki (highly recommended by a 9fin staffer) and Ikos all-inclusive hotels. But it has significant future capex needs, largely funded by debt, as it seeks to increase its rooms by 65% to 4,500 by 2025. Unsurprisingly, it was hit hard by Covid in 2020, with revenues falling by 85%, with adjusted EBITDA turning negative (-€27m). Cash burn was around €4.1m per month. Shareholders who include Oaktree (29%) and GSAM (20%) have committed €100m to future growth and capex.

The split-rated (B-, Caa1) €300m senior secured notes sit behind €587m of priority debt, 5.6 turns of leverage on a gross basis if you are willing to use the run-rated adjusted 2019 EBITDA of €105.5m. Gross total leverage is 8.4x. Cash will be €258m at close, but this is likely to be eaten into in 2021, likely to be tough to get its 40% occupancy break-even rate.

The deal priced this morning at 5.625%, between the CCC-rated TUI Cruises and the recent NH Hotels deals. But this wasn’t enticing for one seasoned HY investor who wrote on twitter:

“Very surprising that people are willing to pay 5.5% for this. Bondholders are just funding the equity upside (through the capex). The company will run out of cash by 2024 so expect more debt. The covenants especially the incurrence isn’t EBITDA based but LTV. Perfect for priming.”

While some might be encouraged by the €1.4bn asset valuation, as our Legal QT outlines, the notes do not benefit from an Opco guarantee and are structurally subordinated to the priority debt which could have room to increase debt significantly. Docs are loose with unrestricted subs explicitly able to transfer value as Permitted Investments to shareholders. Uncapped restricted payments at 46% net LTV – which means that they are available from day one.

I will leave the final word on Ikos to the HY investor who points out that €560m of capex spend from 2016-2020 has only resulted in €100m of additional revenues, equating to a ROI of around 6%. This is in stark contrast to the 20% plus the company projects in the OM.

De Oppresso Liber

News of an Austrian property High Yield issuer this week brought repressed past memories back into my consciousness. Not only is the Austrian jurisdiction difficult from a legal perspective (insolvency regime is a nightmare) but accounting and reporting standards are poor, with several high-profile real estate scandals, which I covered in a past life.

Meinl European Land resulted in brief jail time for esteemed private banker Juilius Meinl in 2009 before he was released on bail for a record €100m bail bond. Unbeknownst to its bondholders the CEE-focused real estate company had spent most of its capital and reserves to do a share buyback to boost its flagging share price. According to a NY Times article the suspected €3bn fraud was expected to ensnare a former Austrian Finance Minister. In 2015, Meinl was eventually charged alongside other board members of his private bank with breach of trust charges over an illicit €212m dividend. MEL investors lost an estimated €5bn.

Immofinanz was another high-profile collapse. Problems at its 51%-owned Immoeast subsidiary (€3.2bn writedown in 2008), eventually brought its collapse. The €500m raised via a bond issue had disappeared between the two companies and Constantia Privatbank – a bank held by Karl Petrikovics, the Immofinanz chief executive. He was finally convicted in 2013 over a series of stock option deals.

But the one that brings back the most memories, is the least well known, but is yet more incredible, the collapse of Level One. I became aware of it in August 2018, when one of my advisory sources complained that it had ruined his summer holiday. He was recalled to London from Spain to head off an insolvency filing after lenders to the c€150m mezzanine debt had covertly petitioned the Jersey HoldCo for administration.

After a failed IPO in 2007, in the spring of 2008 the group turned to a bunch of hedge funds for mezz funding, to keep the plates spinning for a mere 20% PIK margin and a pledge over 50% of Level One shares.

Credit Suisse by this point were very nervous, on the hook for €800m out of the €1.15bn senior debt repackaged into a German residential CMBS securitisation. Rental income was a mere €80m.

A few weeks later, myself and Mario Oliverio (of future Reorg fame) were in the kitchen of Level One CEO Cedvet Caner at his Charles Street Mayfair home admiring the Georg Condo Superman artwork and pouring over a bunch of documents spread across his dining table.

Caner claimed these docs proved that he hadn’t siphoned out excessive management fees, adding that he could find the €60m needed to pay the overdue maintenance bill for 30,000 former East German socialist housing units. He claimed the filing was merely tactical by hedge funds seeking to gain control of the portfolio on the cheap.

An interesting aside, The six-story luxury flat ended up being Britain’s biggest ever house repossession.

After a brief clandestine meeting in a departure lounge of a regional German airport in early August, the mezz lenders lined-up a prominent German insolvency administrator from a top German law firm as CEO for the Jersey HoldCo. Appointed as part of their enforcement plans, the same day he unilaterally appointed himself in charge of the German Operating Companies.

Kroll, the Jersey administrator, removed him from his HoldCo role a day later, but this was not before he had filed documents at the Berlin Court concerned over the solvency of the group. He would later tell me that he had been duped by lenders and that he feared for his professional reputation if he hadn’t deposited the docs with the court ‘as insurance.’

How Cedvet Caner, whose only previous business experience was building up and blowing up a call centre company in his native Linz could borrow €1.3bn against a bunch of prefabricated East German flats with high vacancy rates was probably a sign of the times for the hot commercial real estate market. In 2006, bankers were desperate for product to securitise, and real estate agents willing to push up appraisal values to suit.

Caner claimed he had Monégasque residency for tax status, our reporting due diligence found out this was incorrect. A motor racing fan, two of the loans backing the securitisations were called Lowes and Porters, the toughest corners on the Monaco GP circuit.

There were also wilder accusations of Russian mafia involvement and siphoning off of funds by Caner (who had Kurdish ancestry) to fund the PKK in Northern Iraq. But we couldn’t substantiate. One day I should write the screenplay.

For those who wondered what happened to the insolvent portfolios – Portier and Loews were acquired by Deutsche Wohnen in 2013 from Blackstone (which bought it out of administration) for discounts of 21% and 24% respectively to the whole loan balances.

But I’ve deviated for too long, back to the latest Austrian Property financing:

Part of the Signa Group, owned by Austrian billionaire Rene Benko, Signa Developments is issuing €300m of Senior Unsecured Notes due in 2026. It claims to be one of Europe’s largest residential and commercial property developers (36% offices, 29% residential, 26% retail) focused on Austria and Germany, with significant exposure to recent real estate hotspots Vienna and Berlin.

Their business plan is to finance projects via debt and sell at least 50% forward to property investors prior to their completion which normally takes 3-5 years. It says it has a Gross asset value (GAV) of €3.5bn and gross development value (GDV) of €8.45bn.

Optically pro forma LTV looks low at 50.1%. But the company applies different accounting practices to its peers and recognises annual changes in fair value of its development portfolio in its P&L. Payments on their profit participation notes can be missed, but must be rolled, and if included as debt (as the ratings agencies do) the LTV is a toppy 66%, extremely high for development property.

The focus on gross development value for reporting and covenants is aggressive and as our Legals QuickTake explains there is significant capacity for additional senior project debt (70% LTV) and it can pay annual dividends of 6-7% based on NAV as long as a 55% net LTV is met (allows £104m for FY20).

There are potential conflicts in the retail assets whose tenants are owned by Signa Group, the failed Karstadt department store chain, and Kika Leiner furniture business, formerly part of Steinhoff.

If this wasn’t problematic enough, those with an ESG mandate might decide to look elsewhere. On a macro level, the real estate sector is one of the largest carbon-emitting sectors and has been criticised over its self-regulation, and while Sustainalytics says it is an industry leader there is a lack of meaningful environmental data or targets at Signa, according to our analyst.

But governance is likely to be the major issue for investors.

As our ESG QuickTake outlines Rene Benko was convicted in 2012 of making improper payments to Croatian officials and sentenced to one year in prison. Media reports of alleged corruption, suspect dealings by SIGNA including moving around of assets for tax avoidance, allegations of passing losses to external investors and suspect internal loans, plus potential links to money laundering. Some of these charges were admittedly dropped.

Deliverance for Provident Financial, avoids Amigo’s fate

When the FCA shot down Amigo’s Scheme of Arrangement in June, many observers including us had expected that the Provident Financial’s English Scheme would suffer the same fate. But unlike Amigo, the financial regulator decided not to oppose the Sanction hearing stage.

But in a letter to Provident, it’s clear that the FCA isn’t happy about being backed into a corner by the doorstep lender who decided to stop lending at its PPC subsidiary, meaning that redress claimants could end up with nothing if the Scheme is rejected and it is placed into administration.

While many would say that stopping doorstep lending with APR rates of 1500% is a good thing, it is leaving just £50m to pay claims. A figure which the FCA believes is arbitrary, Provident Financial is able to ring fence its redress obligations, having backed away from a previous commitment to meet PPC liabilities as they became due in January 2022. As the FT says in their summary, Provident’s credit card and car finance divisions are set to deliver an operating profit of £93m this year.

For Amigo Loans there were no smiles from Justice Miles who threw out their English Scheme of arrangement noting the lack of a burning platform, rejecting the binary outcome being posed by the company of an imminent administration. The UK-based guarantor lender had sought to deal with redress claims from legacy lending by placing them in an SPV with just £15m of cash and the rights to 15% of profits from 2022 to 2024. The claims would be compromised by the English Scheme.

The FCA, had challenged the Amigo Scheme, noting around £600m of redress claims would at best see a 10% recovery. A revised Scheme drawing in bondholders and with legal advisors appointed to represent claimants is most likely.

But in the meantime, keen to stop copycat Schemes the FCA has said that it intends to consult later in the year “on guidance regarding the FCA's approach to schemes and other similar restructuring tools, which is expected to include where firms seek to compromise redress through arrangements under company law.” We suspect that Provident and Amigo will be closely watched.

Other 9fin coverage

Despite few active restructurings in the first half of 2021, the evolving legal landscape has more than made up for the lack of deal flow. The effectiveness of new legal processes such as the UK Restructuring Plan are now regularly tested via the courts, with a slew of challenges keeping lawyers busy. Several legal precedents were set, with emergent case law driving how future restructurings are structured.

In our H1 legal review, 9fin spoke to several legal advisors to review activity and identify the key themes in the first half of 2021. We identify and summarise the key takeaways and provide links to more in-depth 9fin articles and lawyer materials for those who wish to dive deeper into the detail.

Topics in the H1 review include the following:

Brexit - lack of recognition of UK processes

New competing processes – Netherlands and Germany to steal from the UK?

UK Restructuring Plan – DeepOcean first to use cross-class cram down

gategroup – why the UK Restructuring Plan is an insolvency process

Virgin Active – relevant alternative; valuation challenges; restructuring surplus

Landlord challenges – lessons from Virgin Active, New Look, NCP

Importance of Burning Platforms – Hurricane and Amigo

A jurisdiction challenge by the French HoldCo for Comexposium was heard on Tuesday in the English High Court in front of Justice Zacaroli. SVP and Attestor, two Comexposium lenders, are seeking a declaration from the court that the information, access, and meeting provisions under their SFA agreement remain valid and binding. The company counters that the court has no jurisdiction to try the claims because it falls within Article 6(1) of the European Recast Insolvency Regulation, following filing for French Sauvegarde insolvency protection last September. It adds that Sauvegarde has its own rules on provision of information and therefore rights and obligations under the SFA are no longer valid under the French process.

SVP and Attestor are seeking information to enable them to respond to the company and ‘fully engage’ in the French proceedings and to protect their interests. But the company has failed to provide any information. They are concerned that similar to the experience of Groupe Rallye the company will abuse the process to impose a ten-year term out on their debt.

Justice Zacaroli issued an order earlier today, rejecting the company’s jurisdiction challenge.

Lawyers for the lenders said they were looking for a three-day trial (to assess their Part 8 claim) in the week of 16 August. There was a pressing need to gain information as they expected that a restructuring plan could be promulgated by the company ahead of the 22 September anniversary of the Sauvegarde plan.

In brief

Naviera Armas’ restructuring plan is likely to be amended after Grimaldi agreed to acquire its Transmediterranea assets for €375m. It is also likely to affect the application to SEPI – the strategic fund from the Spanish government for a €160m loan, which el Confidential suggests will have to start from scratch.

Very Group’s Shop Direct appears to have been caught up in the Greensill collapse and is seeking to refinance a $200m loan to avoid a technical default. Our initial analysis is that there is unlikely to be a cross default with the RCF and bonds as it sits outside the restricted group and the off-balance sheet financing may not come under definitions of indebtedness but watch this space.

Pure Gym posted an upbeat assessment of its recent reopening, whilst noting that some restrictions remained in place at its gym’s, most notably in Denmark. It said that it is considering capital raising to fund growth opportunities, adding it is in the early stages of considering options for raising equity, including potentially in the public markets.

Swissport restructured last year, wiping out claims from its senior unsecured notes via a Scheme. But earlier this week, it sought to address some of the smaller and older remnants of its capital structure. It is offering to discuss with holders “the possibility of the Stub Notes agreeing to a voluntary impairment of the Stub Notes obligations in exchange for a cash payment that would be shared pro rata with all holders of the Stub Notes. While this cash payment would be small in comparison to the obligations owed under the Stub Notes, it is a cash payment that otherwise would not be available to the holders of the Stub Notes if the Issuer were otherwise required to file for bankruptcy under the laws of Luxembourg.”

Inter Milan is reportedly looking at its options to refinance its €375m December 2022 bond, of which €100m is held by Oaktree. The fund has also advanced €250m of direct lending to a HoldCo. Suning the Chinese owner has been widely reported to be seeking investors to either exit or raise funds to repay the bonds.

What we are reading this week

We try to be apolitical in the Workout but Keir Starmer’s warning in PMQs a couple of weeks ago, is proving prescient. The sharp rise in the Delta variant has meant that over half a million people have been pinged by the NHS Covid app in the past week. This has meant that up to 20% of some company’s staff are missing for 10-days cue United Pingdom headlines from papers this am.

Richard Walker, managing director of Iceland Foods, said in a tweet that coronavirus-related absences were “growing exponentially. Within a week or two they’ll be the highest ever. This will be a sh*t show for business.” We can only guess how bad it's getting over at Boparan.

First revealed by Global Capital in late June, the EU has announced its Fit for 55 package to meet its 2030 goal to reduce emissions by 55% from 1990 levels. Our ESG team will be looking closer at the impacts for HY names and sectors, but the initial view is that it could have significant impacts on a number of sectors.

As we try to understand movements in US Treasuries in the wake of higher-than-expected inflation numbers, the supposed hedges – Bitcoin and Gold also fell – it took one observer this week to nail it on twitter:

“Who knew that the best hedge for inflation would be a 2013 Toyota Corolla.”