This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Dot Plots, HY Pinches Punch, Landlords fail to call time

Chris Haffenden

•12 min read

The LevFin TwitterSphere was sceptical when I suggested that Barclays’ save the date Leisure and Hospitality issuer on Tuesday could be Stonegate. After all, the day before Boris Johnson had confirmed a widely leaked four-week extension of ‘Freedom Day’ when restrictions that dramatically affected the hospitality sector would reach their terminus.

I was close, the deal was for Punch Taverns.

So, yet another legacy PubCo securitisation is being unravelled, to be replaced by High Yield. It is further evidence that investors are not only willing to look at reopening trades, but are proactively seeking them out, hoping for further H2 upside - the demand for NH Hotels providing confirmation of this viewpoint.

Reopening has created inflationary pressures and the global supply chain is severely constrained. Add in difficulties in finding workers, partly due to Brexit, furlough payments, with many displaced in their home countries riding out the pandemic, there are still many challenges facing corporate issuers as activity returns.

For example, news in the FT yesterday that poultry producers are cutting production due to worker shortages saw Boparan bonds drop 1.25-points to 93.0 bid.

But despite the above, new HY deals such as Punch are still being marketed for perfection, with pre-Covid EBITDA and significant add backs for planned cost savings, assuming savings achieved during the pandemic can be retained. But conversely where are the adjustments for anticipated increased costs – from their inability to fully pass on raw materials prices – plus increased shipping and labour costs?

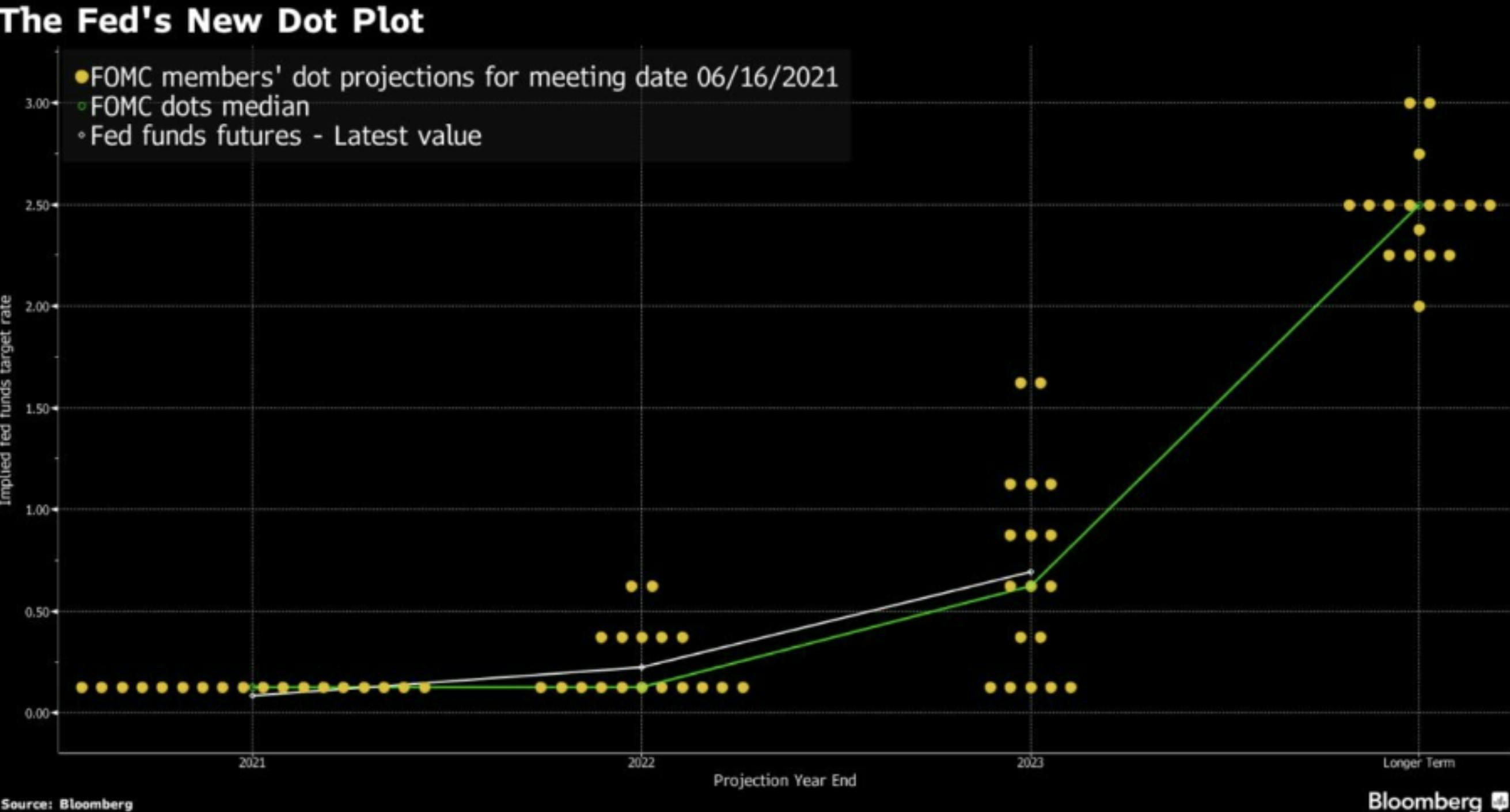

Charting Dot Plots

The Friday Workout previously sounded words of caution whether the narrative supporting risk assets is unravelling in the wake of sharper than expected growth and inflation. Zero hedge puts it well:

“The] Fed is holding rates at zero and buying $120 billion in bonds every month in the face of 17.4% export price inflation, 11.3% import price inflation, 6.6% producer price inflation, 5% consumer price inflation, [with] over 15 million Americans on government dole, over 9 million job openings for Americans, record high stock prices, record low homebuyer sentiment, [while] banks are puking excess cash back to The Fed at record levels.”

Ahead of the FOMC meeting this week, all attention was on the dot plots. These show the anonymous views of regional Fed presidents on GDP, unemployment, inflation, and Fed interest rates. The latter was seen as key, with more members in June expecting two hikes in 2023, with some even going for 2022.

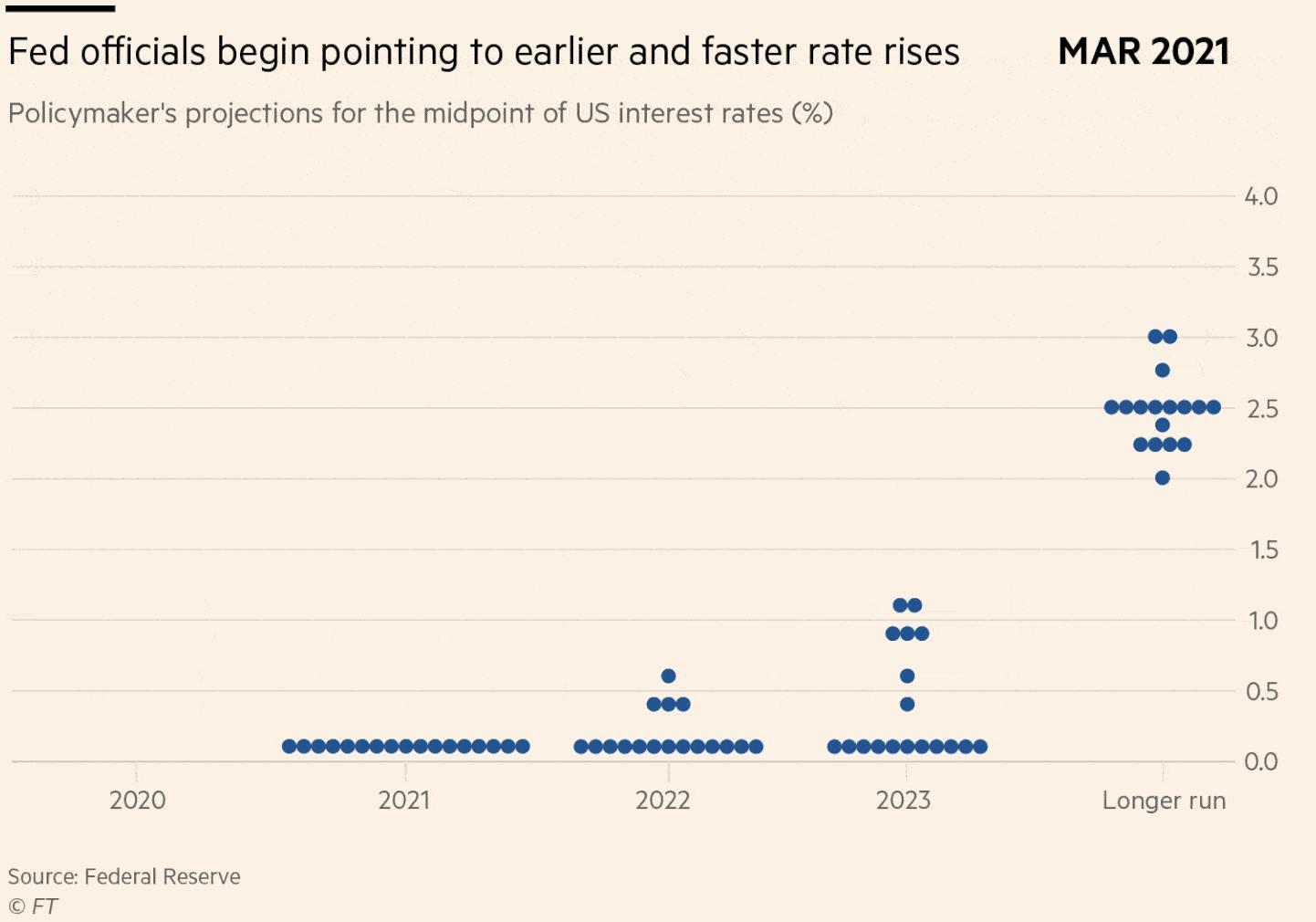

For comparison, below is the one in March. This FT article has a nice moving graphic to show the changes in perception.

There was a slight change in rhetoric, but there was little in J-Pow’s comments to scare HY bulls. Wolf Richter gives a good and easy to read summary of the Feds Monetary policy announcement

Sure, the Fed is considering tapering, but says it will communicate in advance for markets and its QE buying continues for now (but on a net basis if reverse repos continue at elevated levels, effective tapering may have already begun). Treasuries rose by almost 10bps on Wednesday to 1.57% on the comments, but have reversed since to 1.49% at time of writing, the low end of their recent range.

With further fiscal stimulus from Biden’s planned programmes to come and growth surprising to the upside, is it strange that the Fed is starting to alter its stance? Still a long way before we can say they are ahead of the curve (pun intended). The sharp move in five-year yields (now at 0.866% from 0.799% pre-FOMC) and the flattening of the 5/30 year curve suggest this.

However, markets still discount a 72% chance inflation rises will be transitory. The narrative may be changing, but it is happening slowly, and the Fed appears to like it that way.

Pinch Punch

PubCo’s have come a long way from the early 2010’s when they deservedly had bad press. Owners saw them as OpCo/PropCo property plays and seemed uncaring of their tenants forcing them to pay exorbitant prices for mainstream beer whilst limiting their purchase options.

A mutual friend, beer writer and Rye publican Jeffery John Bell explains well from experience how tied pubs such as the excellent Gunmakers Arms, gradually saw a difference in approach from their PubCo landlords.

In a past life, I spent several weeks talking to all the main protagonists for the Punch Taverns restructuring – the complex deal reduced the total debt in two securitisations by £600m took over 3.5-years from start to finish – ending up with a creditor-led solution.

My opus is available on request.

Many advisors on the 2014 deal tried in vain in recent months to approach management believing another restructuring was inevitable. Punch was unlikely to be able to repay £90.2m of Class A3 notes due this September given leverage in the high teens, with the wider securitisation seen as unsustainable.

To avoid tripping covenants, last summer noteholders in the remaining Punch B securitisation agreed to add back Covid-19 effects to EBITDA for covenant purposes. Reorg Research recently suggested that the sponsors were considering injecting equity to address near-term maturities and/or make further pub sales to meet the A3 note repayment.

But Stonegate shows that High Yield investors will look beyond current difficulties and lofty leverage. The UK’s largest PubCo’s 9.5% bonds strongly rallied this year, to yield 6.25% from around 8% in January.

Punch has decided to follow it to High Yield, exiting its securitisations, looking to raise £600m of five-year bonds, priced at a similar level to Stonegate. This might be a tad aggressive, given its previous notoriety.

Positives are a good underlying portfolio valuation of £850m giving a 64.5% LTV slightly lower than its PubCo peers. It also has fewer pubs in city and town centre locations (after selling at top dollar to residential developers in recent years), leaving it less exposed to changes in working and social mixing patterns. It wants to grow EBITDA by converting 178 pubs from leased and tenanted to managed, which boosts margins.

Negatives are substantial EBITDA add backs – around 22% (based on pre-Covid figs), and if these are ignored leverage is at least 9.5x, leaving little or no equity cushion. Hefty investments in pub conversions will hinder deleveraging for at least a couple of years. More managed pubs will result in more earnings volatility. Pension deficits could be problematic, depending on how they are dealt with, said one distressed analyst.

For more 9fin analysis, we have taken a more detail views on the figures with our Financial QuickTake. Please email team@9fin.com if you would like a copy.

Our Legal QT (which highlights that the EBITDA add backs are uncapped for 24-months) and Credit QT (which appeared on the morning of launch) are also available upon request.

Hotel Checkout

At the same time, HY investors were looking at another reopening opportunity - NH Hotels. Some continental investors who had to swap Punch into euros costing them 100bps were questioning whether this was a better trade in the low 4’s. Prior to the pandemic, it traded at sub 3% yields.

The Spain-based hotel operator, which has hotels in European city centres such as Barcelona, Amsterdam, and Rome, expects to have 90-95% of its sites open by end-June. Despite only having nine-months of cash buffer (based on Q1 burn rates) investors were reassured by €874m of unencumbered assets in the €2bn portfolio. Just prior to the deal, NH had disclosed a €125m sale/leaseback of a Barcelona hotel, and secured €100m convertible shareholder loan.

Pricing however appears tight at 4%. It’s unclear how strong hotel occupancy will be in the key summer months, reliant on travel corridors, vaccine passports and spread of the Delta variant. Business travel is a key component of revenues, but some investors hope tourist traffic can make up for the shortfall.

Landlords fail to call time

Hospitality businesses have been lobbying the UK government hard in recent weeks. The moratorium on statutory demands and winding-up orders was due to expire at the end of June. With £6bn of arrears, the British Retail Consortium had pitched a proposal to ministers, after a call for evidence in April. Their main points were adopted by the government.

The results will be seen as another blow to commercial landlords.

Many landlords believe that the balance had already shifted against them, after recent court decisions for Virgin Active and New Look. They are expecting several aggressive proposals from tenants in the coming months to reduce rental payments and haircut arrears. NCP’s sanction hearing next week is the latest in a series of battles.

In addition to extending the restrictions on winding up orders from 30 June to 30 September, forfeiture and commercial rent arrears recovery will be extended until March 2022. This date can be brought forward earlier if legislation for new plans for binding arbitration to facilitate compromises between tenants and landlords is enacted earlier.

The full government announcement is available here. A briefer summary from Kirkland & Ellis is here.

The Government says it will publish a formal response to its “call for evidence” on commercial rents and COVID-19 in due course; further information on the call for evidence is here.

McRefi

With restructuring opportunities limited, given the hot financing market, we have been pivoting to looking at stressed refinancing candidates. 9fin’s deal predictions are popular with our subscribers, this week we took the format to McLaren, looking at its potential options.

Faced with a £150m HoldCo loan to repay to the Bahrain Sovereign Wealth fund next month, and £530m of SSNs which go current in August, the UK-based Supercar manufacturer said in its Q1 earnings call that it was looking at equity funding options.

As 9fin’s Ben Hoskin outlines in McLaren lines-up McRefi to deal with £750m of upcoming maturities the existing 5% sterling notes feel priced to perfection at 99.5, reflecting the expectation of a deal getting done. Discussions for a full-stack refinancing - which reportedly will include some equity or holdco debt capital raise - appear to be in advanced stages, with Goldman, HSBC and Global Leisure Partners working on the structure.

We think that Aston Martin is the nearest comp, but McLaren doesn’t have car-fanatic shareholder and has a less transformational business plan. Its aim is to emulate Ferrari, with more exclusivity and sales at higher price points for its ‘specials’ and hypercars. Whereas Aston has a new SUV to drive sales and a technology tie-up with Mercedes, McLaren needs to rely on its own development and a big portion of production costs which it capitalises on its balance sheet as intangibles. Tangibles are just £256m.

Our best guess is that GS will use Douglas as a template to issue a HoldCo PIK to repay the Bahrain loan and take the strain for the new debt structure.

For more information on potential debt splits, debt capacity, relative value and expected pricing, non-subs can request a copy at team@9fin.com

In brief

Two more former distressed candidates took further strides towards safety this week.

Bonds for Germany-based copper alloy producer KME had traded into the 70s in recent weeks. Investors had been concerned about the rolling over of substantial off balance sheet debt (€393m L/Cs and €395m borrowing base facility due 2022) and a €204m pensions deficit.

The sale of its Special’s division dragged on for months, after its announcement last summer. But on Wednesday the bonds surged 15-points to 92-mid when it was revealed Paragon Partners had gone exclusive to buy a 55% stake for €260-280m, implying a 11x EV multiple.

Similarly, Potash producer K+S has the sale of its OU Americas business for €2.6bn to reduce debt from around 9.5x to around 6.2x, according to S&P. Earlier this week, it launched a tender offer for up to €450m in aggregate for its €500m 3% notes due 2022, €625m 2.625% due 2023 €600m 3.25% due 2024 at 103, 102.95 and 104.35 respectively plus accrued interest.

A legal challenge by two Comexposium lenders slipped under our radar late last week.

SVP and Attestor secured an expedited hearing in early July in the English High Court. The application made by SVP and Attestor’s challenges the company’s position that the French insolvency law filing trumps the English Law provision under the SFA docs for disputes.

The funds are seeking information to enable them to respond to the company and ‘fully engage’ in the French proceedings and to protect their interests. But the company has failed to provide any information since last September, they claim. The France-based events business says under French Insolvency law (recognised in England via Recast Insolvency Regulation) the information obligations under the SFA are no longer enforceable. The funds fear a similar fate to Rallye Bondholders, a 10-year term out when the French procedure ends on 29 September.

What we are reading this week

While the UK is trying to buy more time to get second jabs to be more effective against the Delta variant. Unherd asks about the need for third vaccinations and tweaking the vaccine code

Dominic Cummings has provided some evidence of WhatsApp conversations but not direct to the parliamentary oversight committee. This post on his new Substack page is free, I will leave it to you to decide if it is worth paying £10 per month in the future to read.

As Morgan Stanley boss James Gorman says that if NY employees can go into restaurants they can come into the office, the FT has a graphic showing the plans and flexibility of other Investment Banks.

It hasn’t been a good week for new financial vehicles. Lordstown Motors the EV SPAC admitted that its binding orders didn’t exist after a special committee investigation. It then said they did at a Automotive Press Associate bash, but then had to clarify in an SEC filing that in fact it did not have any “binding purchase orders or other firm commitments.”

Billionaire Mark Cuban might have made a Titanic mistake with his investment in TITAN - part of a "multi-chain partial-collateralized algorithmic stablecoin ecosystem" from IRON Finance. Zero Hedge outlines how this might be the first ‘Bank Run’ for DeFi

Could Clover prove unlucky for WallStreetBets looking to squeeze Clover Health to the Moon? Keubiko certainly thinks so, his analysis suggests that $3bn of stock comes out of lock-up on 5 July. One to set your diary for, it could be even more intriguing than GME.

According to the BofA investor survey, investors are still all-in and extremely positive.

But commodities this week (except laggard oil) showed some signs of topping. Copper has led the way seen as the most sensitive to reopening and reflation trades, but in recent days the chart appears to be breaking down. China has announced it will release metal reserves to tackle price and shortage fears which could weigh further on prices.

Meanwhile, the container shipping chaos continues.

And finally, Kudos to Capital Structure’s Victor Jimenez for his suggested headline for Nomad Foods - the owner of Birds Eye