This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Welcome to Excess Spread, 9fin’s new newsletter covering happening, trends, deals and more in structured credit and ABS. We’ve got big plans to come — watch this space.

For now though, let’s take a look at markets. Soggier summer spreads haven’t stopped the CLO market going from strength to strength, with more debut managers in the pipeline, and a huge chunk of primary loan supply ready to be swallowed by warehouses and new issues.

A swift and unscientific review suggests most managers with a presence in the market have at least one open warehouse – though it’s no longer an obvious slam dunk trade to refi or reprice older deals, potentially meaning a less frenetic issuance calendar dominated by true new issues and refis from the Covid era.

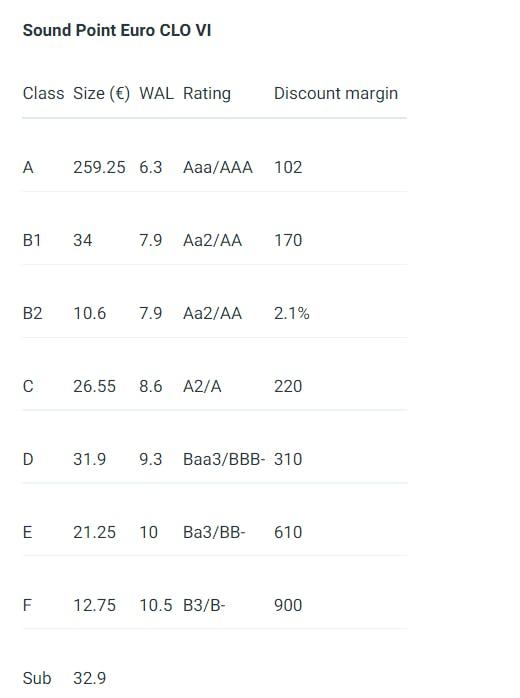

Spreads for AAA-rated bonds are now outside 100bp, having touched tights in the high 70s earlier this year, but the overall cost of capital still points to attractive equity arbitrage, and the “psychologically important” triple digit mark might induce the odd marginal buyer back into the asset class. Sound Point, one of Europe’s top performing managers, landed at 102bp on Friday, while down the stack spreads were roughly in line with other deals priced over the summer, such as Redding Ridge 8 and Voya 6.

Sound Point’s deal has been followed by Cairn Capital with Cairn CLO XIV. Initial guidance levels look to test slightly tighter, with senior notes targeting 100bp-102bp, but triple digits looks to be the norm for now.

New issue loan spreads look like they might be offering a little more juice than earlier in the year, with Roompot, the first sizeable deal of the autumn, marketed on a 450bp margin for a B2/B rated facility. With supply predictions spiralling higher, starting with some concession makes sense – there are no forced buyers any more, and smaller, less liquid deals will need to attract attention.

The CLO market might be increasingly sizeable in its own right, with nearly $200bn outstanding, but it’s still exquisitely sensitive to market technicals, with relatively few players at the crucial top and bottom ends of the capital structure. If one or two of these accounts sit on their hands or hold out for better pricing, it can have a big knock-on impact.

Wrapper’s delight

Coming back to the market following some time off, I was also struck by the reemergence of the monolines in structured credit — Assured Guaranty has wrapped deals for NIBC Bank and Blackstone Credit, cutting the regulatory capital cost of holding CLO debt for banks.

Monolines (specialist bond insurers) were hugely active in guaranteeing subprime tranches and CDOs before 2008, with unfortunate results (most of them blew themselves up), and have been ….rather less active in securitisation since then.

Assured Guaranty doesn’t seem to have shouted about its CLO wrappers from the rooftops though, perhaps because it’s a gift to purveyors of clickbait.

A few publications are still doggedly pursuing the line that CLOs=CDOs of ABS, so throw in a monoline wrap and some regulatory capital benefits, and you’ve got an easy “2007 ALL OVER AGAIN” headline.

It is true that the monoline’s involvement is likely driven by regulatory capital considerations — there would be little point in such a wrapper in a regulation-free universe — but it’s clear enough that Assured Guaranty likes the CLO business. It bought BlueMountain last year, rebranding it “Assured Investment Management”, and providing the BlueMountain team with a captive source of capital to keep their CLO new issues humming along.

More importantly, CLOs decidedly are not a retread of CDOs of ABS, they’re more diversified corporate credit-backed instruments that have been tested brutally in two crises and come out smelling of roses….etc etc, I’m getting tired just typing this.

Everyone who was in the CLO market in 2008 has their own version to explain why their product wasn’t like the bad stuff — and they were basically right.

But there’s still a big regulatory irony to the post-crisis CLO market.

It’s been the big success story of European securitization — the only asset class to have hit higher issuance volumes than pre-2008 — but no thanks to the regulators. European policymakers and regulators have poured their efforts into encouraging banks to fund their consumer lending through securitization, through the “simple, transparent and standardised” framework, but have done nothing for CLOs beyond adding to their admin burden.

There’s been a good deal of high level talk about the need to shift Europe from an “80% bank 20% markets” economy to a structure more like the US, in which it is normal for small and mid-sized companies to access institutional debt markets at a far earlier stage. But when confronted with a market where this is actually happening — the rise and rise of the CLO industry — regulators have tended to get nervous rather than giving their wholehearted endorsement to the shift from bank to institutional funding for Europe’s corporates.

Together gets it

In consumer asset classes, post-summer supply kicked off quickly, with five deals from frequent users of the securitization market — UK RMBS deals from Together Money and Shawbrook/TML, a Dutch RMBS from RNHB, and auto deals from parts of the BNP Paribas and Santander empires.

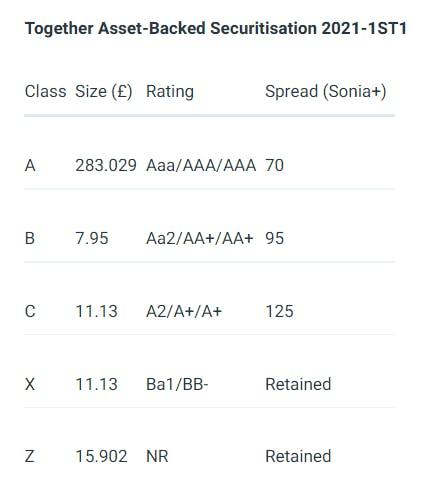

Together, also a high yield bond issuer, took a new approach to the RMBS market, issuing a deal backed only by first charge mortgages, rather than blending first charge with second charge as in its previous issues.

This allowed the company to add five new investors to its RMBS programme, and sharply cut the costs of raising RMBS funding, both through tighter bond spreads and a more efficient capital structure. The new issue was 99bp cheaper than Together’s last Covid-era outing, which blended first and second charge, and 46bp inside the company’s previous best deal. The advance rate improved from the company’s previous record of 81% to 89%, and it was able to issue down to class ‘C’, rather than adding yieldier ‘D’ and ‘E’ tranches as in previous deals.

Together Asset-Backed Securitisation 2021-1ST1

Over the summer, Together also took the unusual step of issuing a £96m non-performing/re-performing privately placed securitisation, backed by loans it was required to repurchase from its warehouse facilities.

As Together’s corporate balance sheet is funded by relatively expensive high yield notes, paying 5.25% and 4.875% respectively, any securitisation funding it can eke out is likely to lower the company’s cost of capital. The deal was placed to a single investor, but serves as a proof-of-concept for future NPL placement, and may serve as an example to other specialist lenders. Together will continue to service the loans backing this deal — often a sticking point for potential NPL/RPL buyers, who usually like to control their own collections directly.

Together, of course, are known for their extensive outreach to the broader securitisation market, putting their hands in their pockets to sponsor the lanyards at Global ABS — a big move for an issuer. Here is your correspondent enjoying his branded lanyard three years back…

Your comments and feedback on Excess Spread would be much appreciated. Get in touch via team@9fin.com or via our chat bubble