This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Still drenched from the deluge of EHY bond deals earlier this week, we at 9fin were hit by another storm, as Viceroy’s report on the Adler complex broke on Wednesday morning. Our focus shifted from reviewing yet more aggressive docs – with Modulaire and Arcaplanet notable mentions – to surveying the foundations of the short-sellers’ allegations as Adler and Aggregates bonds suffered severe subsidence, before receiving some underpinning later that day as cash buyers emerged.

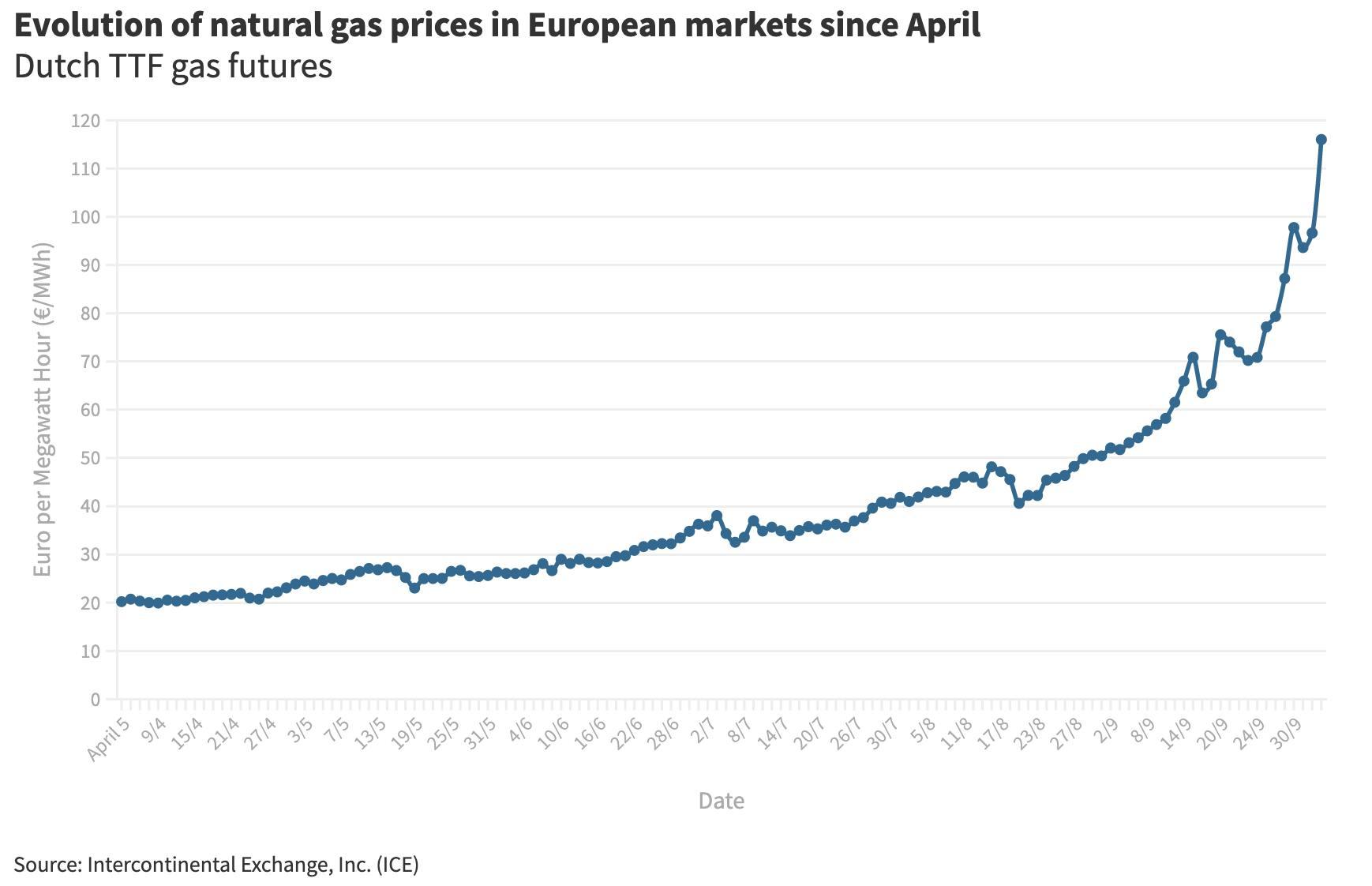

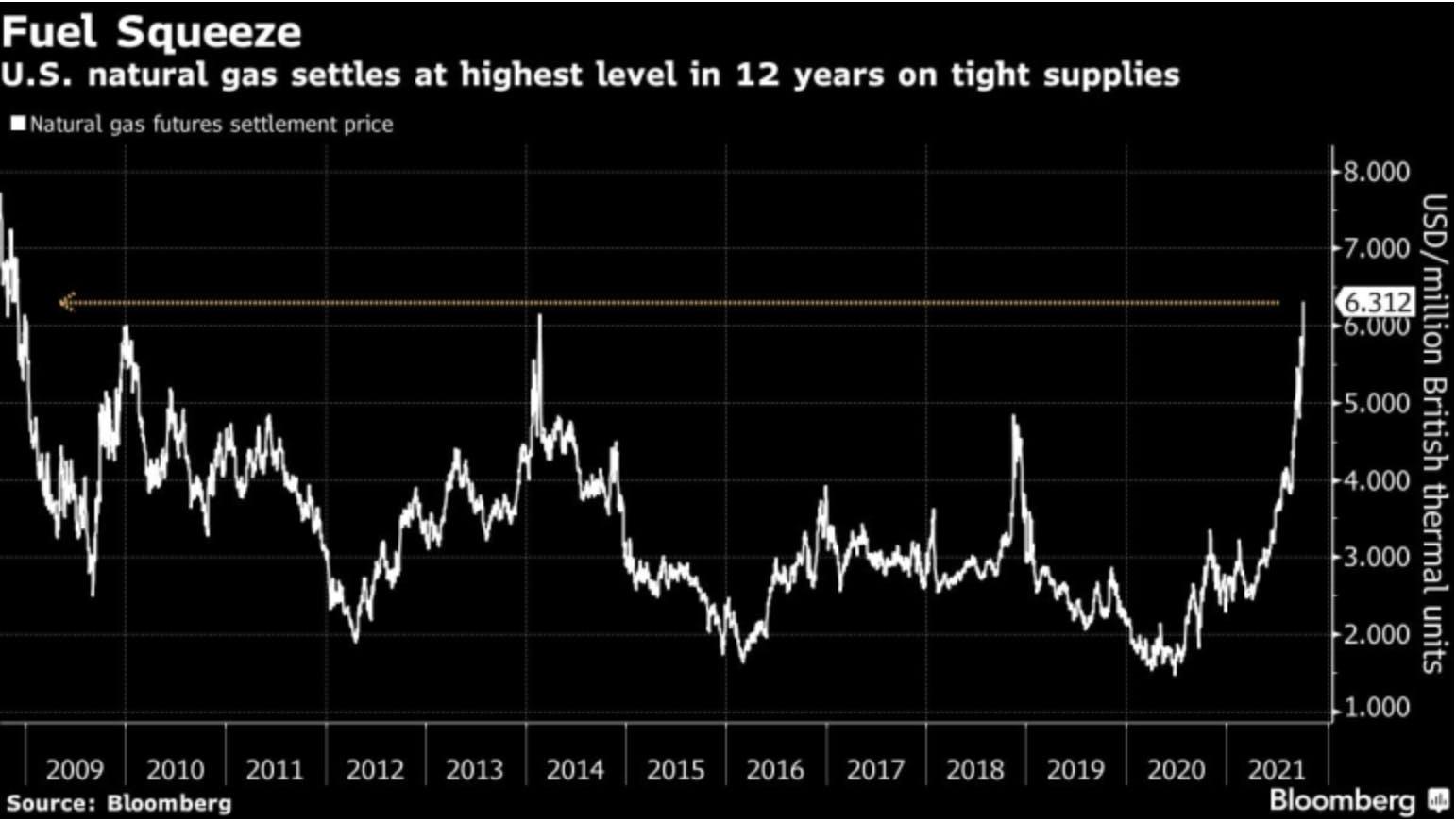

The Adler short seller news diverted attention from Natural Gas prices going parabolic that morning before Putin rode to the rescue and daily price rises quickly reversed. But Natural Gas is still substantially higher than on 21 September when the CO2 crisis hit in the UK. I doubt the US-owned fertilizer plants will stay onstream in the North East when the UK government’s three-week subsidy runs out soon.

A quick skim of our documents database pulls out 120 European HY offering memorandums which mention “Natural Gas” and “Costs.” While we further refine this list, I’m slightly surprised that newbie HY borrower Consolidated Energy with over 60% of its costs coming from Natural Gas has barely moved on the week – more on this name later - but it’s time to return to Adler and renew an old acquaintance who I have never forgot.

Caner Chameleon

Regular readers will know about my and Mario Oliviero’s strange and fleeting meeting with Cedvet Caner in his luxury Mayfair home over a decade ago. At the time he was struggling to keep hold of his Level One property empire and wanted to convince us by showing us a bunch of docs on his kitchen table that evil hedge funds were trying to steal his East German real estate assets on the cheap.

To briefly recap, despite having no real estate investment track record, he managed to borrow €1.2bn from Credit Suisse (the bulk subsequently securitised) to buy an ageing prefabricated East German property portfolio. Amid allegations of stripping out excess management fees and a number of related party transactions, he ultimately lost the portfolio to creditors, but escaped imprisonment after eventually being acquitted of fraud allegations in September 2020.

They say that a leopard cannot change its spots, but Caner appears to be more like a Chameleon – possessing an ability to adapt quickly to his new surroundings to hide in plain sight.

Adler Group denies that Mr Caner has any control over the German Real Estate group, saying that he is only acting as a consultant. But the Viceroy report says that Caner’s control is an open secret and that his wife, brother-in-law, and other associates from his time at Level One hold senior positions at various related-party entities, which they allege are acting covertly with Adler in stripping value away from bondholders and shareholders via a series of related party transactions.

These transactions allow Adler to sell at inflated prices, boosting profits and residual valuations. But most of the payments were deferred, creating receivables which Adler then uses to reduce LTV calculations and keep in compliance with bond and loan covenants.

One of the most notable property transactions was Gerresheim, a former glassworks, sold by German property giant Patrizia in 2017 for €142m to Brack Capital Properties – an Israel-listed company that subsequently become an Adler subsidiary in April 2018. Almost immediately the Brack directors were replaced by former Level One executives. In March 2020 a 75% stake in the project was sold by Brack to an entity owned by Caner’s brother-in-law at a valuation of €375m, giving a €233m fair value gain to Adler. But only a third of the purchase price (€79m) was paid, with a €75m loan also made by Adler to the SPV holding the asset. The project’s development remains on hold, and in their latest Q2 2021 report Adler said it was reversing the sale due to planning delays and objections from Deutsche Bahn, the railway operator. The asset was returned with a €145m mortgage (up from the original €90m) and the €75m loan remains unpaid.

Some of the receivables due from other transactions are almost four years overdue and are unlikely to ever be paid, suggests Viceroy. Not only is the company allowed under its bond docs to deduct receivables amounts to reduce LTV ratios, it is also able to add investments in associated companies to the other side of the equation to improve the ratios.

Under its bond covenants an LTV of over 60% constitutes an event of default, as does a secured LTV of 45%, and unencumbered assets must be over 125% of unsecured debt.

To properly understand the group, you need to know the back story.

In the past couple of days, I’ve been getting up to speed by talking to funds, advisors and those familiar with the German residential real estate market.

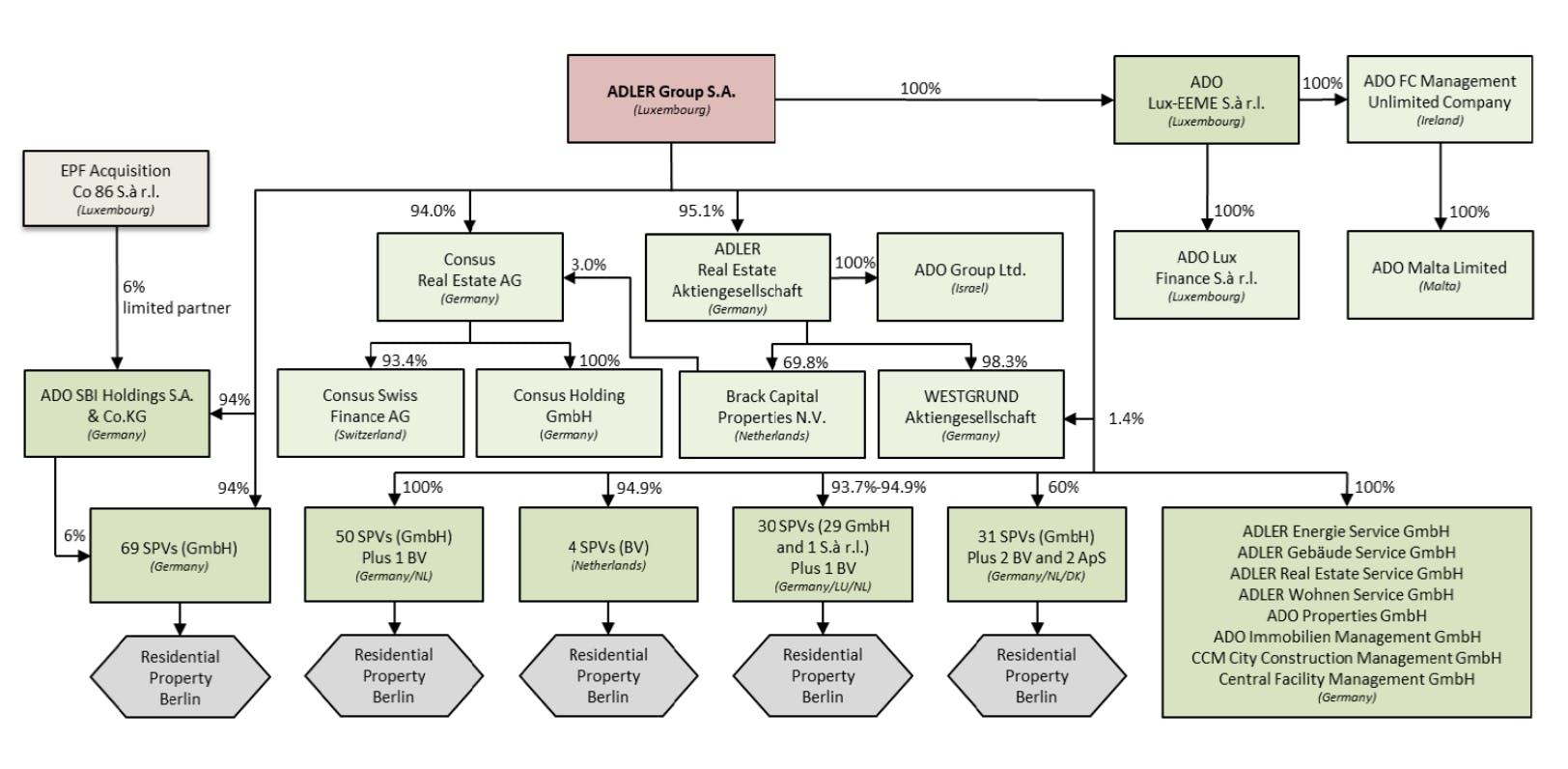

ADO properties were a low-LTV (below 25%) owner of rental properties, more like an annuity play, carrying solid investment grade ratings. But that all changed in September 2019, when Adler Real Estate acquired a 33% stake. It then replaced the board, and then drove ADO to buy Adler RE at a substantial premium to its share price. This allowed them to lower their high LTV via the combination. This prompted outrage amongst ADO bondholders who demanded early repayment and ADO shareholders who tried in vain to get BaFin to intervene. But very recently ADO shareholders were successful in getting a German parliamentary enquiry into the transaction – so watch this space for developments.

The ADO/Adler RE combination was renamed Adler Group, and in early 2020, Adler Group acquired a 20% stake in troubled developer Consus “from certain minority shareholders” with Aggregate Group granted a poison pill at the same time. Aggregate agreed to sell its 51% stake in Consus to Adler in May 2020 at what Viceroy alleges was a substantial premium to fair value. It further contends that Gunther Walther who is the majority owner of Aggregate was a major investor in Level One. Following this series of transactions, Aggregate ended up with a 23.6% stake in Adler, becoming its largest shareholder.

The Consus acquisition dramatically changed the risk profile of the new Adler Group. This was recognised by ratings agencies which downgraded it to Ba2/BB citing the increased uncertainty around development risk, with Moody’s saying at the time “The company will face the challenge of integrating ADO and ADLER while at the same time integrating a build-to-sell developer and turn it into an in-house developer. The transaction expresses a high degree of risk appetite of the company.”

Adler Group has been a prolific borrower in the bond market since the combination.

But a significant amount of Adler Real Estate bonds remains outstanding, in theory they may be better positioned as the company has yet to execute a domination agreement. It is unclear, however, whether this is related to its inability to remove 4.9% of holdouts, but in theory the Adler Real Estate bonds are structurally senior, noted one distressed analyst.

A second analyst noted that LTVs at the two entities are different, meaning that they could be priced differently. Depending on how the situation evolves, there could also be the prospect of orphan CDS which could help provide an improved bid under a refinancing scenario, he suggested.

But we are getting ahead of ourselves. What is the real issue here?

Yes, there appears to be evidence of a number of related party transactions with individuals with a chequered history, but should bondholders really be worried, surely, they are still covered?

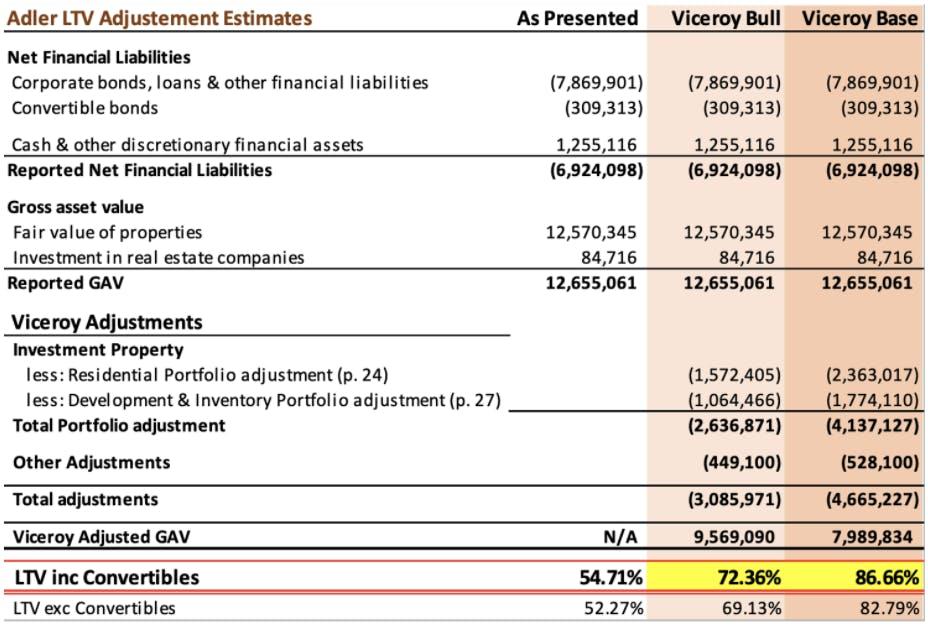

Viceroy is questioning the discounted cash flow valuations it uses to value its property portfolio and the discount rates applied, which it says significantly inflates the valuation of its rental assets. The 2.3% -3.8% cap rates used are substantially different from its peers, such as Grand City Properties -with a 4.1% average cap rate, with Viceroy outlining that Adler’s rates are on average 100bps lower than their market peers. The cap rates are more suited to high-end properties in Berlin, but the quality of the properties are B and C class, and Adler applies this rate across their whole German portfolio. It provides anecdotal evidence on rents per sqm and investment capex to back its arguments.

Compounding the valuation effects, are assumptions for rental growth which are 3-5x higher than its competitors, say Viceroy. Adler is assuming that it can reposition its portfolio to increase rents by at least 20%. But rental growth rates have been on fire, especially in Berlin with attempts to impose a rental freeze overturned in the courts, and a non-binding referendum by its citizens to repossess apartments from real estate companies. Around 50% of Adler’s properties are in the city.

Using residual value for its development pipeline is also problematic, note Viceroy based on “various subjective, sensitive and long-dated estimates” Adler assumes that all the projects can be completed at their estimated cost. Viceroy cites a number of instances where properties were not developed, and development expenses were reversed through the accounts.

Making adjustments for cap rates and changes in the valuation of the development properties, Viceroy calculates a 86.6% LTV in its base case, and 72.36% in its bull case, both significantly above Adler’s LTV triggers:

But as LevFin Twitter was opining on Wednesday night, even at these elevated LTV levels the bonds should be covered. In any event we should know relatively soon, as Adler has said that “it has decided to initiate a review of strategic options for its residential yielding portfolio which could result in a sale of a material part of its yielding assets, following strong inbound demand and recent upward market valuations.” The co-CEOs (yes, there are two - I wonder who has the final say) said they wanted to accelerate deleveraging and return funds to both bondholders and shareholders.

FinTwit (again) claims that on hurried calls with management, they outlined those proceeds would be applied to the bonds. The distressed analyst cited an interview with German trade publication manager magasin, which quoted one of the CEOs as saying that 40k to 60k properties could be sold, a substantial portion of its 69,701 units, of which 19,853 are in Berlin.

Recent transactions suggest that demand for portfolios remains strong. Akelius recently sold its €9.1bn German and Nordic residential portfolio to Heimstaden Bostad for an impressive 2% yield, according to a report from CoStar. The portfolio had 14,050 apartments in Berlin, 3,592 in Hamburg, 1,093 in Copenhagen, 4,107 in Malmo and 5,934 in Stockholm. But rental rates and property prices in the German capital are showing divergence, with a recent JLL report outlining strong rental growth for better quality properties, but that Berliners are net-leaving the city given the unaffordability of rents.

If Adler can realise prices higher than book, it will reassure investors on its LTV levels. But what will they repay? Adler says that all its debt maturities in 2021 are covered, with the next main maturity being €400m of Adler RE bonds due in April 2022, will they take out these or the more expensive longer-dated debt? Will these be true sales to non-related party transactions and be mainly for cash?

Post asset sales, the group will be inherently riskier, and it will still need to find finance to develop its development pipeline, to generate future value, noted the second analyst. The bonds are currently yielding 6-7% [as at Thursday], and while the group says it has around €1bn of capacity to issue on a senior secured basis – they are unlikely to get anywhere near the sub-1% funding levels of their rivals, he added.

In the past couple of days, Adler bonds have rebounded strongly from their lows. On Wednesday around 100m of bonds traded, noted the second analyst. The focus now will be on the company providing a more detailed response to the Viceroy allegations. In the meantime, there could be further noise regarding a BaFin investigation – they have already said they are treating the Viceroy allegations seriously.

Then there is Aggregate Holdings, whose bonds have been hit even harder in recent days, hitting 60 at one point yesterday – they were just below par at the end of August. Given its purported dependence on Adler to service its debt burden, with talk that it has margin loans secured against its Adler stake, causing some to believe it is a leveraged bet on Adler. But this morning, Vonovia announced that it had purchased an 18-month option over a 13.3% stake in Adler Group at a significant premium to the current share price, saying that the shareholders and all other relevant stakeholders in the German resi sector have no interest in an unstable Adler. You wouldn’t bet against them being a buyer of Adler portfolios either.

This has created a sharp short squeeze in Adler bonds this morning, with some bonds on the open being up as much as seven points. Aggregate is up even more, almost 15-points higher, as Vonovia revealed it was “working with the involved banks we have extended a loan to Aggregate Holdings in the lower three-digit-million range at prevailing market conditions.”

I suspect this story will run fast in the coming days, but to avoid the workout becoming a creature of one, not many colours, we will leave Aggregate for another time.

Unnatural Gas (price moves)

I will resist the temptation to get political on the reasons and causes for the shortages and sharp movements in natural gas prices in recent weeks. But the magnitude of the moves has been incredible, as has the intra-day volatility, especially in the past week.

A number of industries and LevFin borrowers are heavily reliant on natural gas. Not just chemicals and refining, but food and paper sectors, alongside cement and other building materials, aluminium iron and steel production and metal packaging, to name a few. Helpfully the current bogeyman Gazprom gives a breakdown of UK energy use and the fuel mixes.

Illustrating the magnitude of the problem, on Wednesday, Saint Gobain, the French building materials company said its energy and raw materials costs inflation would be €1.5bn this year, up from €1.1bn. I suspect several analysts will be hurriedly looking through Q2 reports to look at corporate energy usage and hedges, and their ability to pass on input costs. The third quarter will be testing for many.

A company on a recent bond roadshow said that for the Natural Gas inputs to their Caribbean and US plants “they are hedged out for two-years out for “high levels of coverage.” They revealed that approximately 90% of their gas needs are hedged into 2023. But, surely, given the recent price action, you are entitled to ask more details about the nature and magnitude of the hedges? It really matters when and at what price they were struck. Could they have been put in place only recently at elevated prices approaching 6,000 or struck nearer to 2,000 earlier this year?

This is even more important as for Consolidated Energy - if you haven’t guessed the credit by now –natural gas is 60-75% of their cost of goods sold. The world’s second largest producer of methanol (and producer of urea ammonium nitrate and Melamine) says ‘take or pay’ contracts with gas providers and gas contract caps and collars - surely these are much more expensive than in past years given the price volatility - and “price formula products to end product pricing” for Methanol give it a natural hedge.

But in one-on-ones with investors, some were disappointed by the Consolidated Energy management’s reluctance to provide any further details of the hedges and their structures, citing commercial sensitivities and confidentiality, said one potential investor who knows the industry well.

The company was very keen to stress owner Proman has a Trinidadian natural gas supplier sitting outside the restricted group providing around 1/6 of their total gas supply, but once again they were unwilling to provide any details on the terms. The investor said he left the meeting feeling sceptical on whether the commercial supply terms were more favourable to Proman than Consolidated Energy and given the lack of clarity it was almost impossible to have enough information to make an investment decision, he passed.

Given the raw material inputs, we were surprised to see very little movement in their bond prices this week. The company may be right, Methanol prices might be in a new super cycle, but historically it is a market with high cyclicality. We will be watching their first set of public earnings with interest.

Ice lands in stressed, Takko is back, oh

Another week, another dire warning from Iceland Foods MD Richard Walker. He seems to be everywhere, on TV and Radio constantly – I think he must be an insominiac, flipping from late night Newsnight to an early slot on the Today programme. If you’ve somehow managed to miss him, the former Brexiteer is telling everyone who will listen just how bad everything will be this year. Iceland’s electricity bill will be £20m higher in 2021, wages are £12m higher, green packaging another £10m, he says.

“We are not an endless sponge that can absorb all of these different cost increases,” he told the BBC Today programme. “Unfortunately, price rises are inevitable.”

One thing that did go in his favour as Iceland boss this year was the perfect timing of its bond issue in February. The bonds yesterday dropped below 90 – yielding 7%, which in the current market is in the stressed category.

But while Iceland is yet another name from the 2021 issuance crop to appear on our stressed list, another name is going the other way, amid a surprisingly strong recovery in Q2 earnings. You might be shocked to hear that Takko now yields below Iceland with its bonds rapidly approaching par.

While it is notoriously difficult to get hold of its earnings numbers, I am reliably informed that adjusted Q2 EBITDA was a record for the German discount fashion chain, generating an incredible triple-digit FCF number during the quarter. Remember, it was just six months ago that it was running out of cash after talks over a €75m KfW loan had broken down. It eventually raised €53.6m of new money consisting of a €23.6m super senior facility and €30m term loan. The facilities paid 7% cash interest, with the PIK element undisclosed.

With a cash balance now approaching €200m there is some speculation that they might seek to take out the interim financing, or even refinance the November 2023 bonds and FRNs. But with cotton prices rising sharply and shipping costs needing to be carefully managed, the group would prefer to keep a liquidity buffer, said an investor who was lucky enough to unearth the dial-in details in time.

What we are reading this week

The reading list is slightly reduced this week, as the author spent a lot of time editing QuickTakes and loan previews for primary, reducing time trawling the net for subjects of interest.

So please excuse me for blatantly plugging 9fin legal teams report on Modulaire. Within a couple of hours of launch we outlined “sponsor-friendly provisions too numerous to effectively summarise in a TLDR.” The summary was almost as long as our full reports with it being “among the worst covenant packages we’ve seen in EHY, and novel features not seen before.” Many of the most egregious covenants were dropped or amended for the loans. We then prepared a red-line analysis in double-quick time when the bond docs were also amended a day later – a rarity in the current hot market.

China might have not grabbed the headlines this week. But they may today, with Evergrande bondholders on a call this morning to discuss calling a default on the Jumbo Fortress Enterprises private notes. Their grace period ends today, which would result in a cross default if they enforce. Earlier this week, the FT’s Martin Wolf states why China’s reliance on real estate for demand and wealth generation must end.

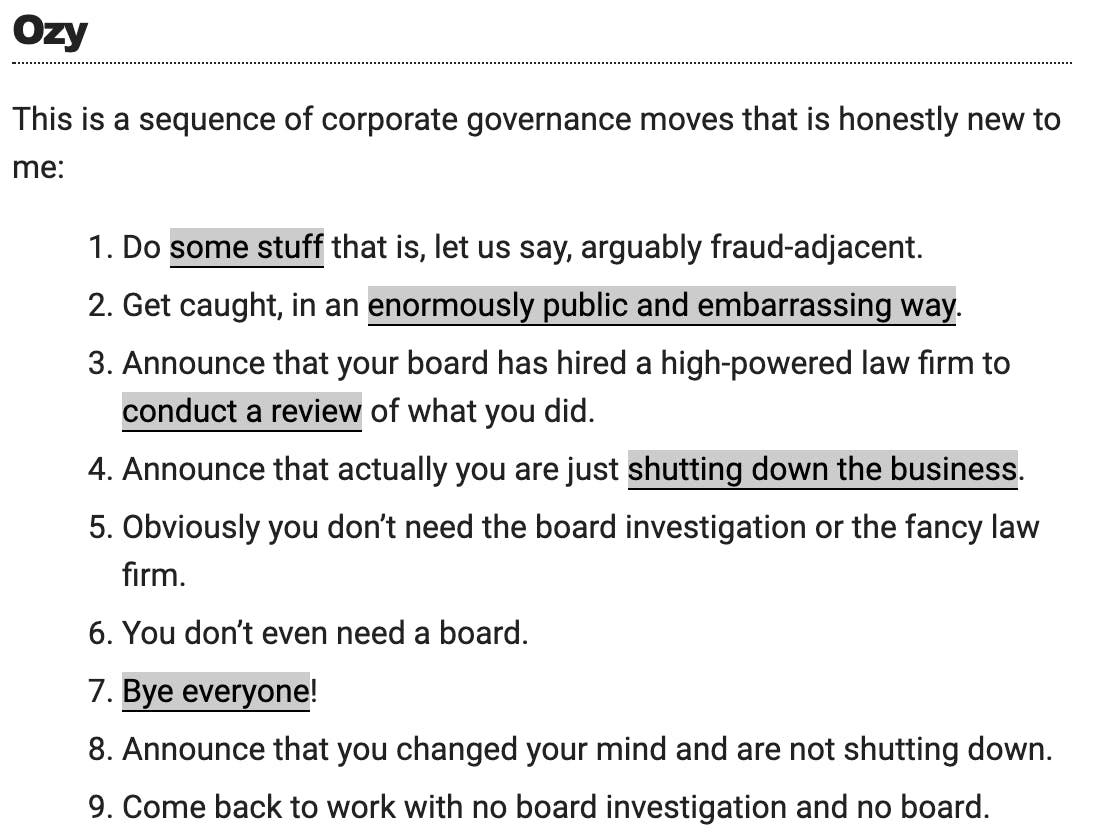

And finally, you remember the story about Ozy last week – the fake voice for a YouTube executive and subsequent shuttering of the New Media organisation. Matt Levine posts an update: