This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Friday Workout - Capital Punishment; Core-Minus; Cashing-out of Diebold

Chris Haffenden

•18 min read

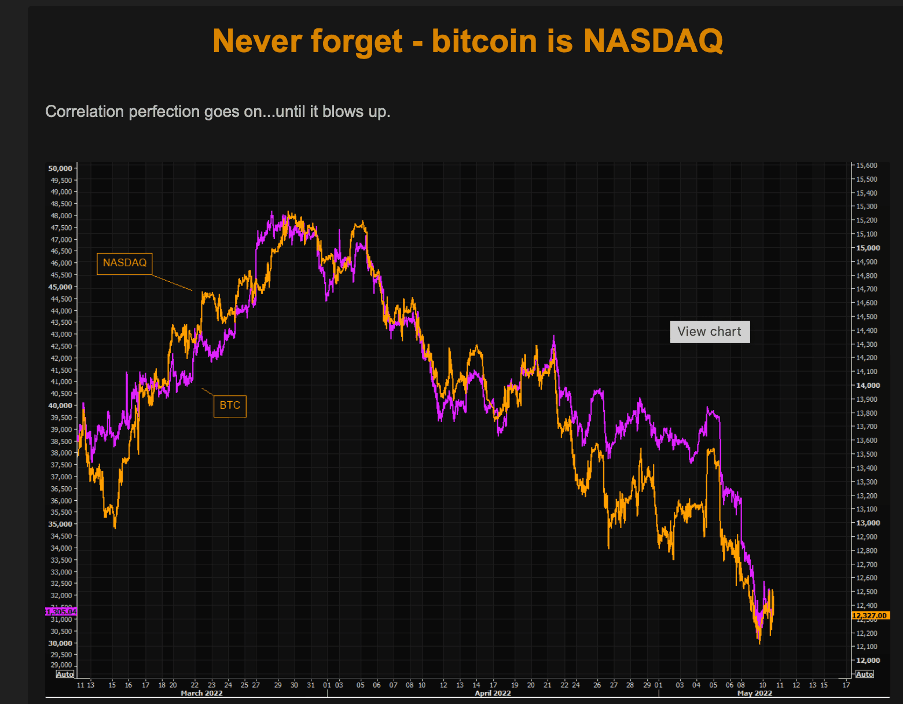

Last Friday afternoon, it felt like the capitulation trade was well and truly underway. Our internal pricing alerts went crazy, with dozens of intra-day price movers of over 2%. Investors’ capital was getting punished. Even the leveraged loan market got in the act, as US stonks and crypto (have you seen the correlation between the NASDAQ and Bitcoin?) broke key support levels and investors rushed for the exits. Scarily, when I run the search late pm, 108 European High Yield issuers (out of 554 companies we cover) had weekly price moves of more than 3%.

The ugly price action and volatility continued into Monday, with the US 10-year at hitting 3.20% but closed -9.3bps lower at 3.03% and broke back through the 3% barrier the next day.

As stocks continued to come under pressure (we narrowly avoided a bear market -20% close on Thursday for the S&P 500), the flight into the safety of government bonds continued, with the US 10yr closing last night at a 2.85% yield.

Crypto wasn’t so lucky, as the buck was untethered and coin(de)base(d), albeit for a short while.

The Itraxx Crossover closed Monday at a lofty 469 bps, over 200bps wider than the beginning of January, but dropped back below 450 by Wednesday close as we saw some bargain hunters emerge in High Yield, then widened a little, failing to keep pace with govvies.

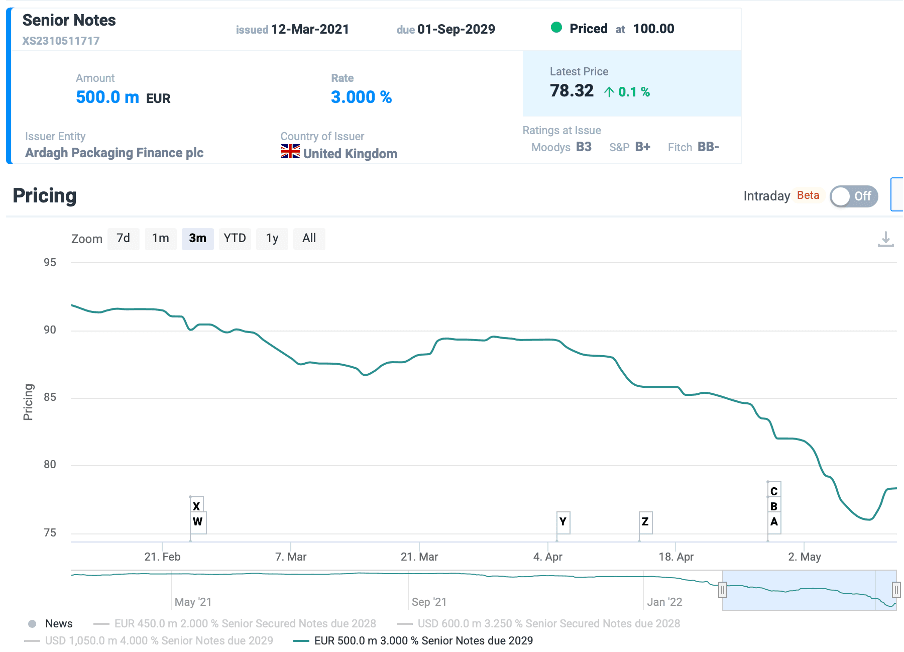

To show how much this spread widening and rising rates has affected EHY prices, let’s take a look at an example - Ardagh Metal Packaging SUNs, issued last March at 3% and par – yes, you were buying single-B rated subs at 3% this time last year!

On a spread basis, the bond widened by around 200bps, pretty much in line with the rest of the market. Last week, it reported flattish EBITDA with leverage rising 0.5x to 4.2x (back to the same as at issue) the bonds are currently at 78.32-mid - that’s a helluva lot of capital punishment!

At least buyers now are truly buying High Yielding paper, the bonds now yield 6.8% YTW.

Our bonds screeners show just how widespread the capital hit is.

We now have 481 bonds trading below 90, from 239 issuers. From this sample, 101 from 64 issuers trade below 80. That’s a lot of potential capital appreciation. A year ago, the vast majority were above par, we now have just 220 bonds, from 132 companies.

This week was characterised by sharp daily movements in certain names of more than 10 points as tape bombs exploded for Corestate and Diebold Nixdorf. There were yet more developments and updates at Adler and Aggregate, and could it be nappy ever after for Ontex from M&A – holders will hope so, the Q1 numbers gave off a nasty whiff. More on these later….

Avoiding imposition of Capital Punishment

As BofA wrote in their Credit Strategy – Europe this week, “Risk assets are feeling the pinch from the end of the era of financial repression. The adjustment to a world where central banks swing from the seat of buyer of first resort to seller of first resort is proving a painful process. Global bonds are reeling in 2022, on track to deliver annualized returns of -24%.”

Their analysts make an interesting point about the lack of HY supply in Europe, we had a 10-week hiatus, the longest on record. While this helped technically to deal with fund outflows, there are €47bn of bonds to refinance by year end. Refinancing concerns narrative will get louder, and BofA suggest spreads are at risk of sharp repricing wider from the first deals coming to market. 14 out of 17 sectors must refinance at a higher (weighted) coupon than their maturing notes.

I can envisage the return of generous new issue premia to help get deals away, and as my 9fin colleagues have written ad nauseum in recent weeks, most deals were heavily pre-sounded and pre-marketed, to the point where books are covered at launch. But the risk is that rather than seeing primary issues with decent NIPs tightening into secondary levels, the opposite happens and primary drives spreads wider. Chatter about private credit and their ability to take paper off leads is getting louder too, is High Yield in danger of talking itself into disenfranchisement?

LaLiga, as the only HY deal in the market was always going to be illustrative, setting the near-term narrative for EHY primary. It is admittedly not the easiest credit to get your head around, in many ways a structured credit HY bond for CVCs silent participation with a very bespoke covenant package – kudos to my 9fin colleagues for their excellent and incredibly detailed coverage – with 7.125% yield talk for a BB credit, that’s some premium and a tad wider than IPTs. The 6.5% coupon suggests where GS underwriting cap is. Sure, there is some risk around Barcelona and Real not joining CVCs scheme and staring a rival league, but there are protections built in. We will watch the eventual pricing and how it trades after the break with interest.

The worsening economic landscape was well flagged in advance, most notably in this newsletter, but nonetheless it has still tanked risk assets of late. So, is it already showing up in earnings numbers – we are deep in the middle of Q1 releases, after all. Earnings are mixed thus far, some decent topline growth has protected margins, but I mostly agree with BofA that second quarter numbers will be a lot worse, as demand softens, and pricing power wanes.

Anecdotally, looking through our earnings flashes, the number of deals where leverage has increased quarter-on-quarter has grown markedly in recent weeks. According to BofA – HY has retraced 93% of its pandemic increase in leverage, averaging 5x (vs 4.85x in Q4 19), but it still looks elevated historically, not a great position to withstand further shocks, methinks.

David Allen from Albacore seems to agree, in 9Questions he says:

Ratings upgrades are slowing, the rising stars narrative at the start of the year from HY research houses has quietly disappeared, and whisper it, downgrades are starting to outpace upgrades.

Several borrowers dropped into triple-hook in recent weeks – Adler, Standard Profil, Corestate, Diebold Nixdorf, Veon, Frigoglass, Schur Flexibles, Haya Real Estate amongst others.

Core-minus

I’ve always assumed that Corestate got its name as a play on words, a mash-up from Core and Real Estate. In a past life, I listened to Real Estate bankers talk about core assets – meant to be Class A real estate in great locations with high-quality tenants bought with little or no debt.

But just as an estate agent stretches civic boundaries to make a property seem more desirable – I remember once being marketed a property as being in Greater Dulwich, tbf it does sound a lot better than Peckham - bankers like to stretch definitions too. Who can forget near-prime lending? It ended up closer to sub-Prime than Prime!

Core Plus emerged similarly, it sounds even better than core, right?

Not quite, it is meant to mean assets in slight need of improvement, with opportunity to raise the quality of tenants and obtain higher rentals. Leverage for Core Plus is typically around 45-60%, projecting around 8-10% of annual returns.

In recent weeks, the news flow around German Real Estate names would lead you to think that these assets should be renamed Core-minus, after a raft of revaluations and negative shocks.

Similar to Adler, Corestate management have faced disgruntled investors on several occasions in recent months, facing questions on sudden departures of senior managers, delayed audits and more lately goodwill write-downs and risk provisions which halved FY 21 EBITDA.

Late on Monday, it disclosed it had hired an unnamed financial advisor “to evaluate and, if necessary, prepare the options for refinancing both instruments (November 2022 convertibles and its April 2023 SUNs), including potential alternative scenarios. Corestate April 2023 fell more than 17 points on the news to around 40. The shares fell 47%, it now has a market capitalisation of just €146.2m.

The next day the bad news kept coming with its Q1 22 release. Citing a market slowdown and uncertainty due to the Russia/Ukraine conflict and rising rate environment, Corestate withdrew its financial outlook for 2022. The company “no longer considers it sufficiently probable that it will achieve the financial targets originally planned for the financial year. A concrete deviation cannot be reliably quantified at present.”

And there was more, the troubled Giessen shopping centre asset, which was in exclusivity for almost a year is now being re-marketed in the third quarter, “after completion of the modernisation work with a clear focus on optimising the sales price.”

As reported, after several deadline delays, on 8 March, Corestate said that the buyer was close to arranging financing and had told management they could close at end-April. Corestate had previously indicated the Giessen proceeds would be in excess of €90m. Unfortunately, when asked if the sale was cancelled by the buyer or by the company, the webcast cut out (this also happened to many other UK-based diallers) – we know several analysts that have emailed the company for their answer.

The Q&A session got off to a lively start, with a short-seller keen to pressure management on what was happening at its real estate fund management business HFS. As reported, the €1.2bn of mezzanine funds at HFS are on-lent to developers at margins in the mid-to-high teens.

According to the Q1 report increases in performance fees during the quarter “was chiefly attributable to prolongations of Stratos II [one of their mezz funds] bonds that strengthened the nominal base and thereby increased the fund’s profitability.” The questioner wanted to establish if this related to the PIK loans being extended, leading to increased fees being booked as the principal further accrues or as the loans are re-struck and re-priced.

Management said that it wasn’t quite right that they were prolongated, leading to the questioner to forcefully remind them of, and to repeat the language reproduced above. Could Corestate also detail how many loans had their maturities changed in the past couple of years?

Management said that they couldn’t disclose as this was non-public info, just reiterating the 1.5-year average term of its mezzanine loans. The questioner was then abruptly cut-off when asked whether any loans were made to related parties or to previous related parties, with management saying they wanted to take questions from others on the call.

Interestingly, according to one analyst, HFS loan level info was available in 2018. A significant number of mezzanine development loans were to CG Gruppe that subsequently became part of Consus and then Adler. A number of these developments were significantly delayed, and Adler recently impaired goodwill at Consus by €1bn.

After its own fractious conference call last week, Adler on Tuesday released some additional materials, which it called a “Supplementary Update”

It included a statement on auditor’s KPMG’s opinion which contained disclaimers of opinion – Adler still maintains, however, that it has satisfied the conditions under its bonds – note there was no sign of publishing the legal opinion from White & Case. We understand that some bondholders have their own legal opinion which disputes this interpretation. But surely it will be tough to convince a bond trustee to call a default and accelerate without at least one more legal opinion, let alone some form of indemnity to protect it against wrongful acceleration.

There was also a statement on the €265.2m upstream loan from Adler RE to Adler Group. Proceeds from asset disposals were transferred as a short-term loan structured as a liquidity transfer comparable to a cash pooling system, said Adler. This was switched into a long-term loan in March. With most upcoming maturities sitting at Adler RE level, holders may be nervous that this cash leakage can happen to Adler Group, but in theory the loan still gives them an asset and a claim.

There was more info on the portfolio sale to KKR and claimed “high certainty in project sales” and some more detail on secured bank debt and their maturities (banks are listed as 1-10).

The next round between Adler and its detractors is set for 17 May when it updates on corporate governance, and it will then publish its Q1 22 results on 31 May.

The third member of the unholy trinity of German RE HY companies, Aggregate Holdings, announced it is to sell its most valuable asset, Quartier Heidestrassse – a 230k sqm mixed-use Berlin development close to the railway station. It has previously said that it is a key part of Build and Hold segment with SAP as anchor tenant with completion expected next year.

We immediately wondered if this was to help repay its VIC Properties converts. But any sale would take too long to complete, as it needs to find around €280m by the end of May. Aggregate says the QH sale will enable it to materially de-lever its business. But is concerning it is selling its best asset, leaving us to wonder whether a managed wind-down is underway.

As reported, VIC properties convertible holders have exercised their put option, which allows them to demand repayment at 114%. Aggregate has talked about a VIC refinancing transaction, which suggests that collateral might need to be granted at its Portuguese subsidiary’s level, or stakes sold to raise cash. We understand a chunk of the VIC converts was bought by a distressed RE player, who might be motivated to do a deal with the company, or even finance a take out.

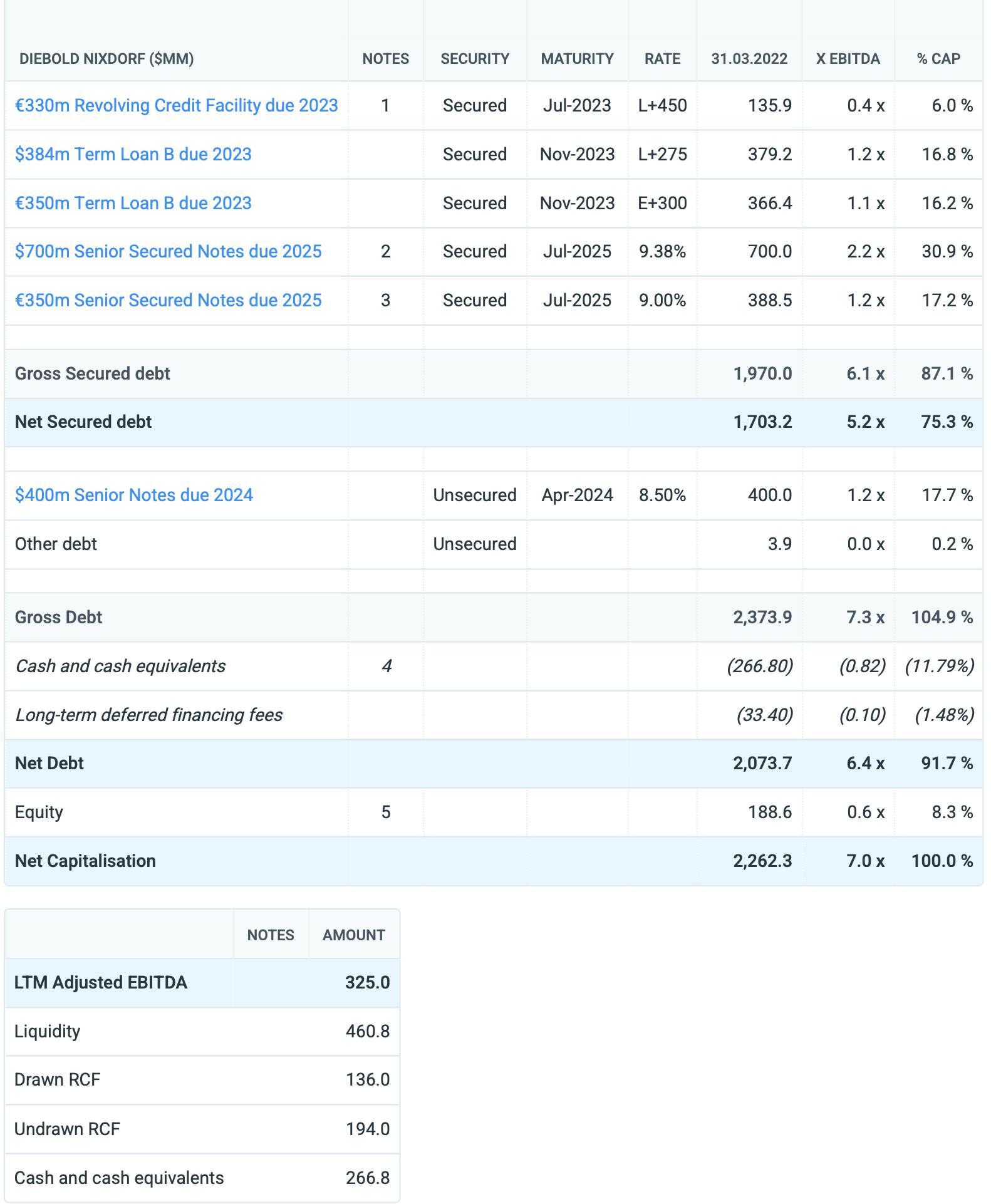

Investors cash-out of Diebold

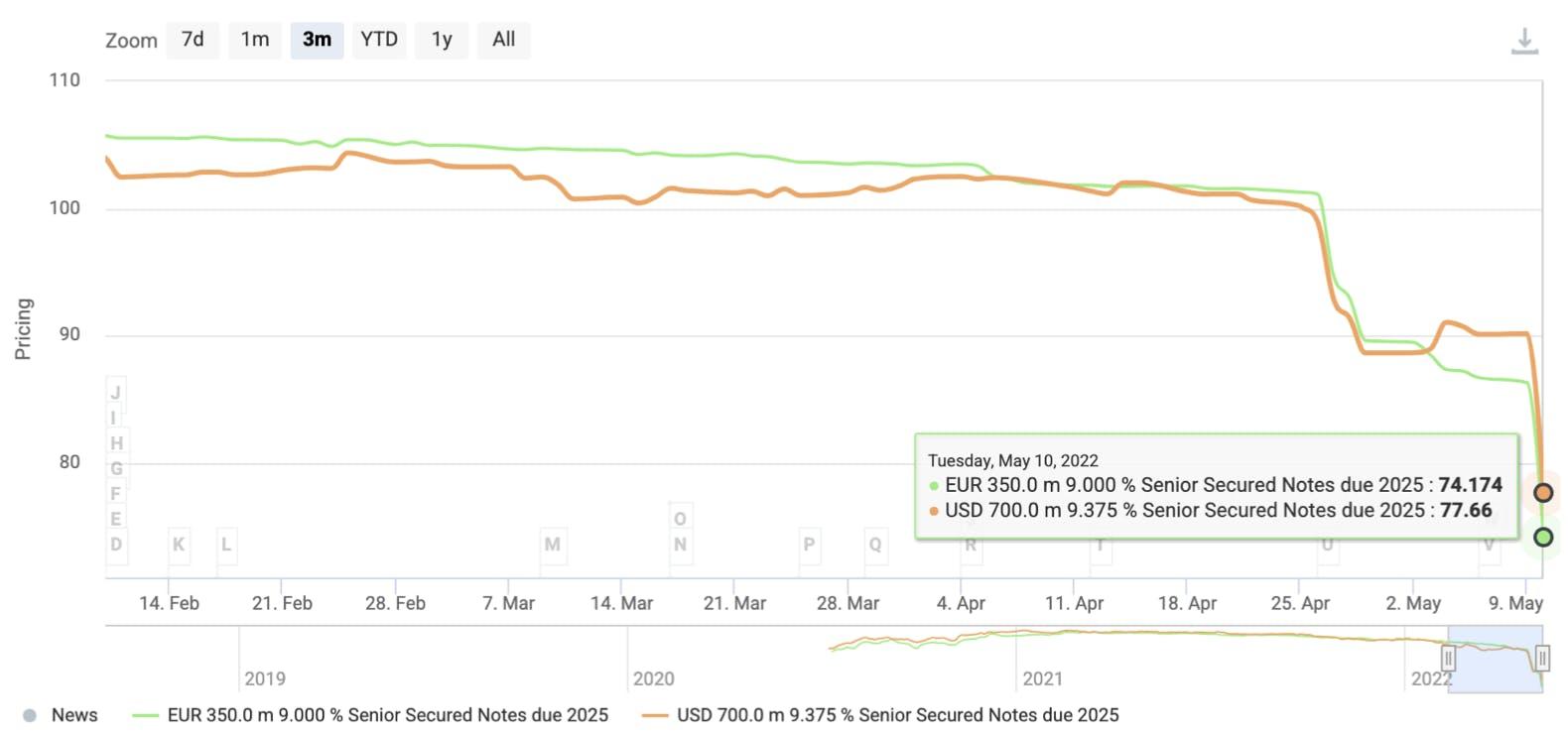

A couple of weeks ago, we were surprised to see Diebold Nixdorf bonds fall by over five points. There was no news at company level, but after a bit of ringing around we were told it was a result of poor results at its competitor NCR, and the subsequent read-across.

For those which sold out on that news, it might have been a timely withdrawal. Earlier this week the US-based ATM manufacturer released its Q1 results. Revenues fell 12% for the quarter compared to prior year, with just $9.4m of adjusted EBITDA down from $100.3m.

There was a big downward revision of revenues, EBITDA and free cash flow for FY 2022. Supply chain disruptions globally impacted Diebold’s efforts in converting order backlog into revenue. Rising input costs put a strain on margins, forcing management to take a more proactive approach at discussing repricing with customers, or suggesting the pre-payment of orders.

A business restructuring plan has been launched, to restore profitability to prior levels with estimated cash cost of $75m over the course of 2023/24. Aware of an upcoming maturity wall, the company disclosed that it had enlisted Evercore and Sullivan & Cromwell to advise on the refinancing of maturities coming due in 2023 and early 2024.

The bonds have reacted negatively to the results release and change in guidance, with the €350m 9.00% SSNs falling 17.5-points and $700m 9.375% SSNs by 15.5-points. Yields have shot up to 20.6% and 21.5%, respectively, with the shares collapsing by 30%.

Refinancing risks are mounting, but there was no clarity provided on the exact timing of the refinancing, with CFO Jeff Rutherford agreeing that there was no ‘straight path’ for the year to come. He did mention that they are in open dialogue with Evercore and Sullivan & Cromwell. The CEO added that a ABL facility (to replace the revolver) was more suitable and that security issues would need to be navigated.

To avoid a breach of covenants, Diebold negotiated covenant relief with investors on 11 March 2022, increasing the max net leverage ratio to 6.75x for Q1 22 & Q2 22. This will decrease thereafter to 6.5x and 5.5x for Q3 22 and Q4 22, respectively. As of Q1, the ratio stood at 6.4x.

Liquidity for the group was $314m supported by $194m of undrawn revolver and $120m of unrestricted cash. These liquidity lines are set to shrink further, with $75m of restructuring costs (which management were yet to factor in), having a large impact.

We’ve added Diebold and Corestate to our expected deals, and our growing list of names to QuickTake.

A Schur thing?

With Schur Flexibles TLB languishing in the low 50s, and a recent trade at 55 for a piece of the Supplier Credit Facility, do recovery prospects make the loans at current levels an attractive investment proposition?

We have tried to provide an answer by looking at recovery prospects for the Austria-based Flexible packaging maker in various scenarios and with two different earnings outlooks.

Blended recoveries for SFA lenders vary by scenario and earnings projections. We have put four different scenarios through a recovery model based on the company’s earnings projections and our 9fin stress test of those projections.

Subscribers can see our recovery projections and access the in-depth report here.

The deadline for heads of terms last Friday, came and went, being extended to today (Friday 13 May). As we outlined, two weeks ago Apollo submitted a proposal on behalf of the lender coordinating committee which offers a much deeper debt haircut of 75% and doubles the new money component to €150m to provide more of a liquidity buffer, according to a source familiar with the situation and a source close. The HoldCo PIK element has been dropped.

The company is supportive of the new lender proposal, but the three Austrian banks providing the supplier credit facility (SCF) submitted their own proposal seeking a higher debt reinstatement and preferential treatment to the SFA lenders and are unwilling to backstop the new money. Schur does not believe that the proposed capital structure under the SCF plan is sustainable. However, with a portion of the SCF recently trading at 55, with the seller believed to be RBI, the hope is that the SCF banks will exit and the new buyers roll into the revised deal.

As reported, on 19 April the company presented a lender update and floated a financing plan with the existing debt would be reinstated into Opco/Holdco debt (36c and 64c respectively). Existing lenders (TLB and Supplier Credit Facility (SCF) providers) would provide €60m of new money (paying 1200 bps PIK) on an interim and pro rata basis, to be refinanced at closing by a €75m super senior facility paying E+550 bps cash and 400 bps PIK due in September 2026.

But the €80m SCF (€77m drawn) provided by RBI, Unicredit and HCOB cannot be further drawn, and is subject to a standstill until 3 June. The €45m of finance leases and €52m of local bi-lateral facilities are structurally senior to the SCF and the €100m RCF (€15m drawn) and €475m TLB.

The new money would jump to €130m at closing if this were to be fully repaid and rise further to €145m under the financing proposal - ensuring €75m of minimum liquidity in February 2023.

A revised company side proposal is due today - watch this space for further updates.

In brief

Last year, we flagged in the workout, that Ontex might struggle to execute its turnaround plan and was poorly placed to pass on rising raw materials costs. Our deep-dive in February said whether a function of busyness or symbolic of the newness of the team - the former would be very understandable given the current environment, the December update presentation and subsequent conference call at times lacked substance.

In Q1 margins for the Belgian nappy maker fell to 5.4% (they were 12.1% a year ago). Due to fixed-price contract exposure, Ontex is experiencing a hefty time-lag, especially for private label and institutional contracts, in passing through these costs to customers. An increase in inventory levels to accommodate for customer front-loading also provided unfavourable working capital dynamics and negative free cash flow for the quarter.

But rather than suffering nappy rash, there is a prospect of nappy ever after for bondholders after Ontex confirmed that a potential sale to American Industrial Partners. This led to a five-point jump in its bonds to around 88 on Wednesday. CEO Esther Berrozpe said talks are still in early stages with AIP, and no agreement has been met on how the combination could take shape.

Ellaktor’s long-suffering bondholders finally received some good news. A tender offer by Reggeborgh Invest for the remaining 69.5% of the Greek construction and concession group’s common shares could trigger a change of control. On 6 May, Motor Oil has also acquired a 29.87% stake in Ellaktor shares from previous shareholders Ioannis Kaymenakis and Dimitris Bakos, through their Greenhill Investments and Kiloman Holdings vehicles. This ends a lengthy period of disputes between the two previous shareholders and Reggeborgh. Motor Oil and Reggeborgh have also entered into a framework agreement for the acquisition by Motor Oil of a 75% stake in Ellaktor’s Renewable Energy Sources (RES) segment.

Concerns over Orpea’s ability to refinance short-term maturities amid a scandal at the French Care Home operator and an investigation by the French prosecutor were alleviated today. It announced a jumbo €1.733bn facility being negotiated with its banks via a concilliation procedure overseen by the Nanterre Court. We will follow-up on this in more detail in the coming days.

What we have been reading this week

I’m old enough to remember money market funds breaking the buck in September 2008, being worth less than their deposits, it was arguably the moment that the banking system collapsed.

This week, we might have seen the same happen for crypto. Stablecoins have a similar role, and on Wednesday after a sharp sell-off in digital coins, Tether did the same. There were past concerns about the assets backing the 1:1 peg, most notably the use of commercial paper. This Tweet from Octopus Capital outlines the issues and if we should be worried

Less well publicised was the breaking of the buck a week earlier, by TerraUSD, a algorithmic stable coin (I didn’t know they existed either). As this excellent Forbes article explains “UST uses a complicated setup with another token, LUNA, to try and maintain its peg. LUNA is a native token of the Luna blockchain, a decentralized platform like Ethereum...” Yes, I’m tuning out here too, but essentially something which shouldn’t fail, or far too clever for its own good technology has failed. Matt Levine’s subsequent piece is a must read.

Terra appears to have triggered the concerns over other stablecoins, with Janet Yellen this week voicing concerns about risks to financial stability - Tether has a market capitalisation of around $80bn - so any bailout should be manageable, but it could spill over into the much larger Crypto market - $1.21trn, down 6.87% on Thursday alone. If that causality wasn’t enough, look at the correlation between Bitcoin and the NASDAQ... Tether’s CTO’s interview with the FT doesn’t exactly convince, but he may be forced by the regulators to reveal its secret sauce. At time of writing Tether has re-tethered itself, and crypto prices are recovering (or at least not collapsing).

Source: The Market Ear

A plug for my US colleagues, who provided an update on HY Bitcoin babies being in trouble with Coinbase’s inaugural high yield bond dropping below 60 cents on the dollar this week, while the notes that MicroStrategy issued last June to fund the purchase of Bitcoin fell below 80.

Looking through Vivion’s financial statements, we saw something interesting relating to the Aggregate Bonds issued as part of the consideration for the Furst sale.

We wouldn’t rule out that the asset manager being Corestate. Oh what a tangled web we weave...

As we wonder whether White & Case will allow Adler to publish their legal advice - coincidently there is a new partner in their High Yield team in Frankfurt - to be clear, he is unconnected to the Real Estate Group of the same name.