This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Friday Workout - Dead Cats Society; NOTWIRE, Reservoir Dogs Tullow

Chris Haffenden

•13 min read

Magicians are not Masters of delusion, they are the Masters of misdirection. Our overconfidence and instant assessments on what is put in front of us makes us open to manipulation. As Tim Harford says in a piece in yesterday’s FT (speaking about fake news)

It could easily apply to corporate frauds and our misreading of company financials and offering memos. “The things right in front of us are often the hardest to see,” said Apollo Robbins, the theatrical pickpocket. “The things you look at every day, that you’re blinded to.”

Even if things start to look bad, in political communications there is always what is known by strategists as the dead cat strategy. A crude misdirection, if events turn awkward, throw a dead cat onto the table, it might outrage, but you will have changed the subject and diverted attention from where you don’t want them to look.

Looking back, many corporate frauds are easy to spot, as most were hidden in plain sight.

There are various degrees of manipulation, however.

Things can start as easily as trying to smooth earnings, inflate cash positions, to make the numbers appear a bit better, maybe by just enough to hit targets. Surely, it is the corporate equivalent of massaging a CV, doesn’t everyone do this to some degree?

But covering up over time and trying to extricate yourself can get out of control, think of what happened to Nick Leeson.

A private court session for the Virgin Active Sanction hearing last Friday, provided an unexpected bonus, it allowed time to listen into Grenke’s investor update.

Grenke shares and bonds tanked last September, as short-seller Viceroy highlighted deficiencies in the leasing companies franchise model – claiming it overpaid and overstated goodwill with many purchases made on a related-party basis, many with Wolfgang Grenke, the founder and chairman. It led to a BaFin investigation via Mazars, and KPMG brought in by the company to do an internal audit.

Grenke promised to bring the remaining franchises onboard in the next two years and tried to reassure investors with new hires and improved processes. While the cash balances appear genuine (we do question why they need to be so high) and the top 10 franchises appear to be legit, there is still a lot of work to do. An interim report from Mazars in February critical of compliance and internal processes led to the departure of the COO Mark Kindermann.

Management in my eyes (and a couple of analysts who were conversing online with me) failed to impress on the call. The CEO remains in charge of internal audit (a potential red flag) and couldn’t disclose how much costs would rise to improve processes, despite full audit reports to land by the end of this month. Continued access to unsecured funding (none undertaken so far in 2021) and whether Grenke Bank (deposits fund a third of lending) will face heavier regulation from BaFin, were other concerns expressed by questionners.

As the call was drawn to a close, after almost an hour of questions, there was a curveball, a recent Suddeutsche Zeitung interview with Wolfgang Grenke, who is stepping down as Chairman, who mentions that his oldest son Moritz will be taking his board seat.

The call had so many issues, with management statements riddled with inconsistencies, said one. “They then wrap up with the clanger that Moritz, son of Wolfang, wants his dad’s former board seat. He’s worked for Grenke and for a board member’s firm, [it is] not exactly fixing governance.”

NOTWIRE – nothing to see, move on

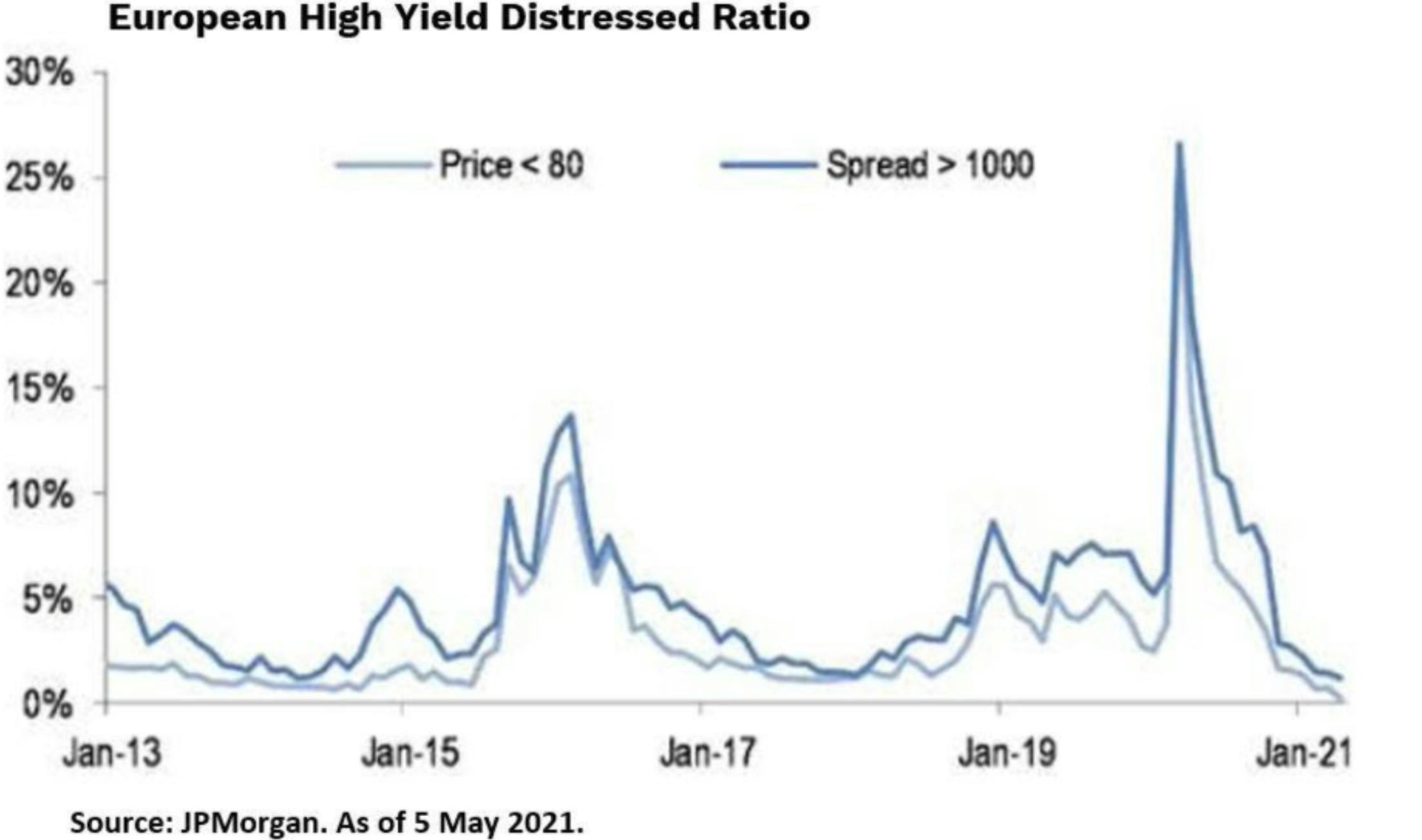

Regular readers of the workout know my views on the pricing of risk. Despite elevated leverage and business uncertainty, we have many stressed and even distressed businesses trading above 90. The chart below from JPMorgan illustrates this perfectly, the number of deals priced below 80 and with a spread above 1000bps is the lowest since 2013.

We are deep in earnings season and on the lookout for businesses which may be showing signs of distress, which may be not priced in by investors. But it is not easy to spot the signs, often we only have time to skip through the management presentations which are dressed to impress and focus on the positives. What is omitted, or not emphasised is where we should be looking. This is the magician's equivalent of a white dove - our eyes are directed elsewhere as it flies upwards.

Paying attention shouldn’t be hard, but the overarching lesson of the psychology of misdirection is we are blind to our own blindness, says Tim Harford.

This is where good fundamental and forensic credit analysis comes in. I’m amazed how a good analyst can put a set of financial figures into a spreadsheet and pick up anomalies and/or trends that we’ve missed in the presentation. But this takes time, and the universe to analyse is growing each day.

With so many businesses with ample liquidity, no near-term triggers and ready access to funding ,a lot of companies appear to be saying in their presentations “nothing to see here, move on.”

This reminds me of a product idea that I had with a few ex-colleagues.

We had to provide ‘actionable intelligence’. Journalists even filed their copy as ‘opportunities’. But often content was more prosaic, under pressure to write regular ‘updates’ on long running situations or having to doorstep multiple company execs for clues on corporate actions.

We cruelly called these NOTWIRE alerts - nothing happening, no new info - not actionable.

Almost a decade ago, on a long lunchtime walk to the much-missed Fuzzy’s grub, a few of us decided it could actually be a business opportunity, rather than just a satire opportunity.

Bankers, Advisors and funds spend a lot of time scouring companies and services like ours for mandates and transactions - what if we narrowed the field, and showed where not to look?

We already had the content, it just required some new tags and keywords - ‘never in a blue moon’, ‘over my dead body,’ nothing to see, etc.

Unfortunately, our bosses failed to see beyond the satire.

But a decade later, with so much information overload from a variety of news and data services and a need to filter out the noise, it may be time to bring back the NOTWIRE idea.

Reservoir Dogs Tullow

Not for every credit are we starved of information and lacking background knowledge. There are some credits this particular journalist has covered for years, knows the business well, and more importantly which are the smarter investors and analysts who know the credit best.

Tullow Oil is one of these names. Our preview ended up being a deep dive.

Their 2021 converts and 2022 bonds hit the mid-20s last March, as oil prices dived. The company hired advisors earlier this year for a refinancing. We had expected an A&E with some cash paydown and an exchange into new 2026s, with a springing maturity to 2025, if the 2025 SUNs were not refinanced.

The motivation to take out the $1.7bn Reserve-based lending facility with the $1.8bn of new senior secured notes was one of the key questions.

Had lenders decided to demand repayment under the 18-month liquidity test?

Or had the company decided that the six-month redetermination process was too onerous? With estimates that the RBL paid around 6%, their funding costs were set to rise, but default risk has reduced, after taking out the 2021 converts and 2022 SUNs.

With decent hedges in place (which limits the upside as well as the downside) it gives Tullow runway for at least 2-3 years. However, the E&P company is more about production risk than a bet on oil prices, noted an analyst bullish on the name.

After a string of exploration failures, the new management team has pivoted towards producing Ghanaian fields, and away from East Africa and South America. But reserve levels at TEN and Jubilee have fallen in recent years, which the new management team is seeking to stablise by using new technologies and drilling adjacent to existing Ghanaian fields.

2P reserve levels of $3bn do cover the debt stack, but Tullow counts gas reserves in here, which it flares or pipes to Ghana National Gas Company for no cost. There is also a $356m disputed tax bill from the Ghanaian government, with concerns that the West African nation is seeking to exert more power over oil companies. The sale of minor partners Occidental’s stakes in the TEN and Jubilee fields will be closely watched, the $500m figure quoted by Reuters, would leave Tullow deep underwater on a sum of parts basis.

Failure rate of new drilling and success in stabilising TEN and Jubilee production is likely to be key. We thought the new SSNs would price with a 9-handle, but printed at a wide 10.25%.

Let the games begin

There are some sectors which divide opinion. Debt collectors were one, but in recent months, a consensus has emerged, with many performing well during lockdown, with Lowell’s A&E seen as a turning point for sentiment last Autumn.

Gaming companies are in a difficult position during the pandemic, especially those with a poor online platform. As one advisor acting on one active name said last week, social pressures and increased regulation are never far away. But conversely, although governments don’t like them, they rely on these businesses for tax revenues and use them as cash cows when they can. But in the Covid pandemic many have granted tax deferrals and are likely to provide more support, he added.

We had highlighted risks to German arcade operator, Lowen Play in our deep dive in January. It faces a new regulatory framework on 1 July 2021 which alters the number and type of machines which it would be allowed to operate. The group faced tight liquidity and is almost entirely reliant on support payments from the German Government to survive until lockdowns ease. Auditors EY have expressed material uncertainty about the Group’s ability to continue as a going concern. But the company says “assuming that all arcades will be open on 1 July and that monthly revenue will initially amount to €14.2m to €17.2m and on planned cash inflows from the requested government aid (our emphasis), the management boards believes that the Group will more likely than not have sufficient liquidity in the forecast period. This failed to move the August 22 bonds, which are quoted around 97-mid.

We will have to wait until 20 May to listen to management.

Greek gaming company Intralot released its FY20 report earlier this week. Revenues decreased by 16.6% to €437.7m, but EBITDA increased by 2.5% to €64.6m, mostly driven by improvements in its US operations. Liquidity dropped from €171m in December 2019, to €100m at year-end.

But we were not interested in the numbers, there had been radio silence since the group announced in January an aggressive plan with a group of 2021 holders to exchange their unsecured notes for new 2025 notes, which would benefit from security from its US business. The 2024 SUNs would be offered an exchange into 49% of the equity in the Intralot TopCo. But the 24s called foul and have threatened litigation if the company tries to implement the plan, potentially via an English Scheme. Our Intralot 2021 Bond Exchange – the Known Unknowns analysis goes into the issues.

In the release, Intralot says “it has entered into discussions during the last months with the aim of reaching an alternative agreement that will allow the parties to restructure the 2021 notes without recourse to a scheme of arrangement. Such negotiations are already at an advanced stage, and the company believes that it will be able to make a new announcement on the matter soon.”

This suggests some movement amongst advisors, and that the previous plan may have been a bluff. Their conference call on Monday, could be interesting.

Greece’s Olympic Entertainment saw fourth quarter revenues drop by 65.6%, with adjusted EBITDA turning to a loss of €0.3m. Bondholders may be ruing the loose docs, which has seen the online business and the Lithuanian business stripped from the restricted group.

Spain’s Codere has finally succumbed to a much-needed restructuring. A larger than expected €125m new money need resulting in a full-blown restructuring, as super-senior baskets weren’t enough to bridge liquidity. Senior noteholders will receive 95% of equity in a new TopCo, with 25% of their notes reinstated, and 29% exchanged into a PIK stapled to the equity. The senior secured bonds have traded strongly since the announcement from around 60 to 69. But the shareholders have not given up their litigation attempts, despite recent setbacks – with a key hearing in June.

Parking Plan charges

Virgin Active’s Sanction hearing continued into this week, but there was still time to put out an update on NCP Car Parks, which is seeking to impose a similar payment plan on its landlords. A Practice Statement Letter was issued last Friday. Advised by Deloitte and Kirkland & Ellis, the Car Park operator owned by Japan’s Park 24 and Development Bank of Japan, is looking to inject £120m into the troubled business which has suffered from a collapse in vehicle traffic during the Covid pandemic. The UK Plan will be split into six classes, with the landlord occupying four of these.

The Virgin Active judgment will be closely watched by the NCP ad hoc group. The Virgin landlords are challenging the UK Restructuring Plan on grounds of fairness. They complained about the lack of information and disclosure, most notably around the business plan and the assumptions made by Deloitte in a report to develop pay-outs under the UK Restructuring Plan, which seeks to impose sharp rental reductions on the majority of its landlords.

The Virgin Active case is likely to have widespread implications not just for landlords and the prospects of retailers, but for the implementation of cross-class cramdowns under UK Restructuring Plans. We will go into the key legal issues in-depth next week.

Plus, Minus

A scandal brewing for a small loss-making Spanish airline may have delayed and even scuppered the restructurings of Abengoa and Celsa. The investigation into Plus Ultra, which has close ties to Venezuela, has seen SEPI, the Spanish-government funded rescue fund to review all companies which have already requested aid and some will have to represent their proposal. It is reviewing all of its processes after the appointment on March 30, 2021 of Belén Gualda as president.

What are we reading/watching this week

There was an element of luxury to High Yield borrowers this week with TUI Cruises and Golden Goose. I discovered two new words this week, Sneakerisation and Experiental.

The biggest economic argument is over inflation and whether the extreme pressures we are seeing right now are temporary or could have wider implications. The global chip shortage and supply chain pressures are starting to feed through into reduced production and prices are starting to rise as a result. To understand how the chip shortage developed, read this Quartz article explainer.

What happens if most of your portfolio is yielding less than inflation? What assets are the best inflation hedges? I would argue that Crypto is not an inflation hedge, but a way of stopping excess liquidity getting into the money supply - as long as you HODL. Do we buy lumber or copper at 10-year highs, or laggards such as Gold?

As we detailed last week, the moratorium on winding up orders is due to expire at the end-June. British Retail consortium has asked the government that the £3bn of rental arrears from retailers under Covid should be ring fenced and granted another six-months protection