This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Friday Workout - Fighting the Fed; Tip of the Iceberg; BaFin(al) straw?

Chris Haffenden

•15 min read

This week as stocks were back in a bull market (NASDAQ is up 20% from lows) and US Treasury yields fell sharply, several Fed officials sought to reiterate their hawkish tone that inflationary pressures remained strong, and a slowing economy would not temper interest rate rises. But markets are not listening, they think the terminal rate will be much lower than the fed governors’ dot plots, they think that recessionary fears will mean that the Fed will start cutting rates in less than a year, with inflation forecast to drop sharply thereafter.

Not everyone believes the market’s Goldilocks scenario fairy-tale. As 9fin’s designated Cassandra and perma-bear, and being more grey-haired than my youthful colleagues I can (just) remember when inflation wasn’t so acceptable in the 80s. So, I’m less Trusstful than most.

Whoever is right, I can’t remember a time when the markets and central bankers were so divergent in their views. The Bank of England yesterday said that inflation would hit 13% in the UK and would still be 9% in a year’s time, with a year-long recession.

Fancy buying 10-year Gilts at 1.85% anyone? Negative (real) yields are still alive and well.

What about easier financial conditions? The latest moves in stocks and rates means that central banks must do more work to have the desired effects. If risk markets rally too far here, faster, and bigger interest rate rises are needed to normalise interest policy, let alone set restrictive rates. It is not beyond the bounds of possibility that US terminal rates can easily hit 5-6% IMHO.

Lower commodity prices (oil might soon break key support at $90) and easing of supply chain pressures might be bullish near-term signals, but that is not necessarily enough for inflation to come back down sharply and quickly, so that European LevFin can party again like its 2019.

Stubbornly high energy prices, wage inflation and a general economic downturn (we’ve barely seen a reversal of QE liquidity yet btw) could mean that secondary and tertiary effects take over.

As I said last week:

“While the first wave of the bear market was a correction of markets and assets inflated by excess liquidity, geopolitical concerns, and supply shocks, which may now be finally abating, could there be a second wave from weaker earnings and economic stresses? Is price risk about to turn into volume risk?”

And what if inflation is structural rather than caused by supply chain and demand? My favourite big thinker economist Zoltan Pozsar thinks so, and in his latest report doesn’t he hold back:

“Markets expect the surge of consumer prices will soon peak and central banks will become less hawkish, but there’s a high risk that global cost pressures will remain elevated,” the Credit Suisse economist said in a client note. The world is being wracked by an economic war that’s undermining the deflationary relationships that have prevailed in recent decades where Russia and China supplied goods and services to more developed nations, he said.

“Think of the economic war as a fight between the consumer-driven West, where the level of demand has been maximised, and the production-driven East, where the level of supply has been maximised to serve the needs of the West,” he says.

Therefore, there is a risk rates might have to rise to 5% or 6% to create a substantial and sustained reduction of aggregate demand to match the tighter supply profile, he continues.

“Interest Rates may be kept high for a while to ensure that rate cuts won’t cause an economic rebound (an ‘L’ and not a ‘V’),” otherwise it might trigger a renewed bout of inflation.

Source: Zoltan Pozsar

We were reminded about supply and political risks as Nancy Pelosi got the fly past she wasn’t expecting (or wanting) on her visit to Taiwan and European gas prices spiked yet further as Gazprom once again tightened the valves.

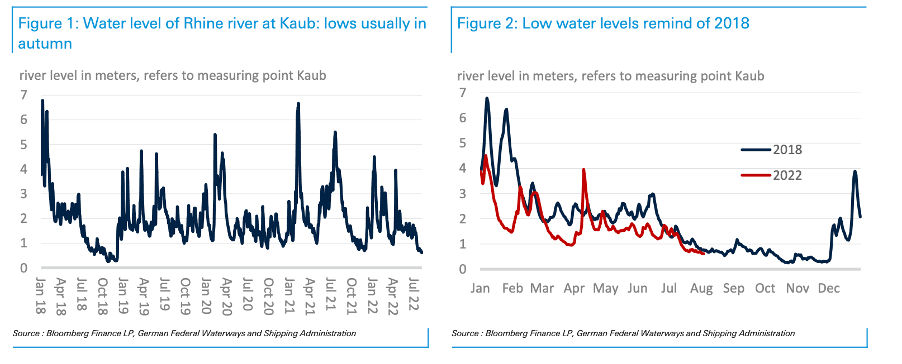

If that wasn’t enough to deal with, the climate emergency might make the short-term economic picture even worse. Low river levels in the Rhine and Garonne are likely to affect German economic activity (and coal deliveries for the reopened power stations) and cooling for France’s nuclear power stations, which might have to go offline, we learned this week.

As Deutsche analysts reported yesterday “waterways could become an Achilles’ heel.” They cite data from April 2022, that coal, crude oil, and natural gas (13.8%) and coke and petroleum products (17.7%) accounted for a large share of the goods transported by inland navigation. Coal reserves at most power plant sites are only sufficient for about one week of full-load operation.

Levels at Kaub on the Middle Rhine are especially important, as below 75 cm depth a large container ship class has to reduce its upload by 30%. Low water levels are happening almost two months earlier than usual. High temperatures mean an increased demand for river water for cooling. More cargo ships are being booked to transport grain exports from Ukraine. Switching to overland is pricey, as a large Rhine barge carries a cargo equivalent to 150 heavy trucks.

Last year Victoria paid a 5.7x multiple for five acquisitions – however, it tells investors it should be valued at 10x – and handily it has unlimited EBITDA add backs for anticipated cost savings and synergies, subject to a 24-month time limit on its bond debt.

We also noted the potential for cash leakage – the preferred equity held by Koch. The company intends to repay in cash prior to their conversion (Nov 26, Dec 27), and management comments on plans to buy its threadbare shares which have fallen through the floor, in recent weeks.

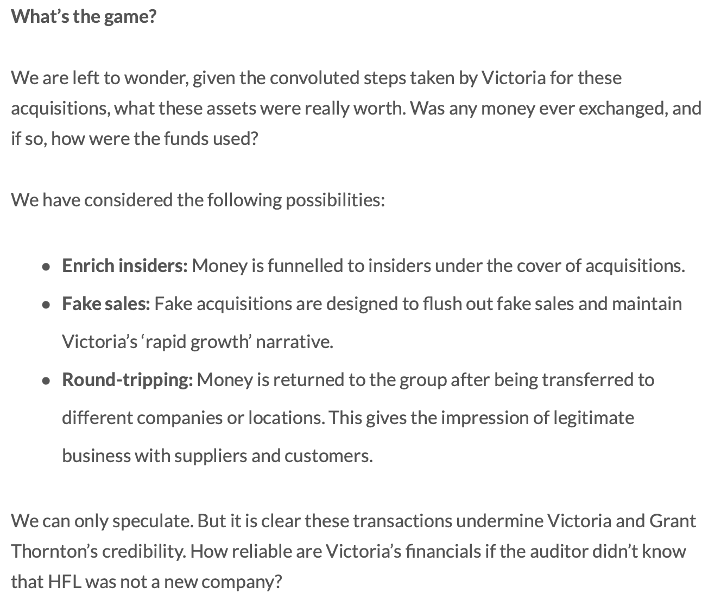

Over the past week, FinTwit has been active. With the shares at one point down 25% on a week earlier, clearly something was afoot. On Wednesday, it wasn’t a huge surprise when we received a report from short-seller Iceberg Research titled – Victoria Plc: Mites under the Rug – which alleges fraudulent activity relating to some group acquisitions.

Iceberg cites two transactions (Hanover Flooring Limited (HFL) and Ezi Floor Limited) which it claims were purchases of existing subsidiaries, renamed shortly before their acquisition. Saqib Karim, one of Victoria’s managers had founded Ezi Floor and had owned Hanover Carpets – a subsidiary of HFL.

Iceberg hits the floorer hard in their report:

At the time of writing, Victoria Plc has yet to formally respond to the allegations.

And as 9fin’s credit analyst Denitsa Stoyanova noted in an internal message, there may be nothing unusual here. The Karim family founded these businesses, and when Victoria acquires a small family run business they tend to lock-in the owners for at least four-years with promises of earn-outs, and according to management, most owners tend to stay beyond that.

Victoria (as allowed under IFRS 3 “Business Combinations”) bought the assets and placed them in dormant companies. The two deals are tiny compared to the overall acquisition activity – just 5% (£42m) of the £806m of cash outflow spent on buys in the past six years, mostly equity funded.

9fin understands the short seller is investigating other transactions. Victoria shorts will just have to hope that these transactions are just the tip of the Iceberg.

BaFin(al) straw for Adler?

Short sellers have had much more success with Adler Group in recent months. The troubled German Real Estate group got hit by a two punch combination this week, and either blow could be the final straw in its attempts to raise funds to meet upcoming maturities.

First-up BaFin’s investigation (Readers - don’t worry if this doesn’t make a lot of sense at first)

Adler got itself in front of the first piece of bad news by posting its response to a decision by BaFin, the German regulator, before its findings had been formally published. It disputes a detected error in Adler Real Estate (RE)’s 2019 report due to an overvaluation of its "Glasmacherviertel" real estate project in Düsseldorf-Gerresheim.

The determined overvaluation of at least €170m corresponds to the difference between the recognized value of €375m and the book value as of 30 June 2019, at €205m. Compared to the original acquisition costs of €142m, the overvaluation is at most €233m.

Adler RE assumed in the valuation that the Gerresheim site can be developed as planned, although the necessary permits have not yet been obtained. This was based on assumptions about possible uses that were not certain as of 31 December 2019. In addition, the sales contract was not an orderly transaction between random market participants, BaFin said.

On Monday (1 August) Adler Group said it is appealing against BaFin’s decision. It said it will pursue legal remedies to move the resolution of this issue forward.

BaFin said in response to 9fin: “If Adler Real Estate appeals against our error finding, we will examine the objection and make a decision.”

So, what is this all about?

The Gerresheim transaction is one of Adler’s most contentious deals and was highlighted in Viceroy’s report last October. The 2019 sale of the 75% stake in the development project gave an implied total value of €350m, but the buyer only paid €36m upfront with €132m of bank loans arranged by Adler, including a bridge loan for capex spending. Adler booked this as a receivable, but after terming out repayments, it finally reversed the transaction in 2021. The site remains undeveloped, without planning permission with its neighbour Deutsche Bahn objecting to its plans.

Viceroy alleges that the sale of a 75% stake in the project company in September 2019 was made indirectly to the brother-in-law of Cevdet Caner, which resulted in a €233m fair value gain. The now infamous Austrian real estate ‘expert’ is alleged to have controlled Aggregate Holdings for several years. Until recently Aggregate had a 29.9% stake in Adler Group, and amazingly last month, Caner was unveiled as Aggregate’s new CEO.

KPMG Forensic, hired by Adler to investigate the Viceroy allegations said in their report whether he acted on behalf of Cevdet Caner “could neither be verified nor refuted.” They added that the agreed sales price was 80% higher than the company’s internally calculated value, there was a lack of documentation and due diligence despite the presence of an alternative bidder, they said.

BaFin’s statement suggests they are in full agreement with KPMG.

Why does this matter?

The Gerresheim asset is owned by BCP (Brack Capital Partners), which Adler is seeking to sell.

In December 2021, fellow German real estate company LEG bought a 24.1% stake in BCP from minority shareholders and a 6.8% stake from Adler, as reported. As part of the transaction, LEG was granted an option on Adler’s remaining stake in BCP at a strike price of €157 per share (€765 million for the remaining Adler stake) with a 30 September 2022 expiry.

The BCP sale and planned development project asset sales of €1bn - €1.2bn are key for Adler in being able to meet around €1bn of debt repayments in 2023.

Adler had previously expressed confidence that LEG would exercise its option, but yesterday (4 August) LEG said that it would refrain from exercising its option. Adler has said it would also market the stake with an aim to conclude a sale in September.

But with BaFin continuing to investigate 2019, 2020 and 2021 financial statements, there is a risk their probe deters potential bidders. After a strong run German commercial property market values are on the turn, there may be clues on how badly, when Corestate reports next week.

There is also the risk of restatement of accounts, as Adler struggles to find another auditor, which might create an event of default for bondholders.

Envisioning Upfield’s future

In the workout, we’ve sought to inform our European readers about the less genteel actions of creditors and sponsors in the US LevFin. Up-tiering transactions, J Crew’s and creditor on creditor violence are increasingly common stateside.

In Europe, the consensus is it couldn’t happen here – not withstanding what happened to Intralot last year (more later) – as sponsors wouldn’t want to be seen as the first to turn on creditors.

Advisors and investors have told 9fin that they are increasingly worried that when push comes to shove, it will eventually come to Europe. Many are suggesting that KKR’s Upfield (FloraFoods) transaction could be the first deal to do the unthinkable and to spread the US practice.

The Dutch margarine and plant-based food group’s total net leverage was 8.9x as of 31 March 2022, suggesting the sponsor’s investment may be already underwater. But there are few upcoming triggers, as at least two further turns of leverage can be incurred before their RCF springing covenant is triggered and there are no maturities until 2025.

But with its principal shareholder KKR having almost €2bn of equity investment to protect, and with the company’s bonds and loans trading at stressed levels, we wouldn’t be surprised if advisors are pitching the sponsor with aggressive suggestions. As 9fin’s Caitlin Carey and Christine Tognoli outlined this week there are a number of possible structures KKR could use to incur priming debt and undertake below-par buybacks/exchanges of its existing debt.

As we outline in our report KKR “is no stranger to creative structuring techniques to manage its portfolio companies’ capital structures.”

This spring, KKR portfolio company Envision Healthcare undertook a transaction that involved transferring around 80% of its AmSurg business, an ambulatory service unit which reportedly represented around half of Envision’s earnings in 2021, into an Unrestricted Subsidiary. This transfer resulted in the release of the existing lenders’ security over the transferred assets.

The Unrestricted Subsidiary then raised $1.1bn of first lien debt and $1.3bn of second lien debt, structurally and effectively senior to Envision’s existing debt. Then, a portion of the proceeds was used to repurchase around $1.9bn of debt below par, with the remainder used to provide around $1bn of additional liquidity.

Some of these manoeuvres – in particular, the transfer of assets to an Unrestricted Subsidiary and raising of structurally senior debt outside the Restricted Group – could be permitted under Upfield’s bond covenants, we suggest. However, there are also some aspects where this would be more complicated in European debt structures.

The exact details we will leave for 9fin subscribers.

But as a teaser for non-subs, we estimate that conservatively they have around €800m of capacity under the docs, and more aggressively up to €1.27bn.

That’s your Intralot – as Inc dries on 2025 refi

Last year, we saw our first example of European creditor on creditor violence as Intralot 2021 SUNs came out on top in their fight with the 2024 SUNs.

The 2024s however, were offered a partial exchange into 49% of Intralot Inc’s TopCo’s equity, and to avoid breaching restrictions on secured/priority debt incurrence, Intralot designated the new US topco and its subsidiaries as Unrestricted Subsidiaries, resulting in the US group no longer being subject to 2024 notes restricted covenants, triggering the release of the 2024 Notes guarantee from Intralot Inc, the issuer of the new 2025 secured notes.

With 2024 holders holding a blocking stake in the 2021s, Intralot took an innovative, two-step approach to achieve the necessary 90% consent threshold – partially redeeming the 2021 Notes and then replacing them with additional locked-up / consenting notes.

Regular readers will be aware of the legal arguments that were made for the first European restructuring to use a drop-down Unrestricted Subsidiary financing structure, borrowing elements from J Crew. For a refresher, take a look at our analysis of the issues here.

And last Friday, Intralot said that it had fully refinanced the 2025 PIK toggle notes via a $230m three-year loan and $50m RCF led by KeyBank National and a syndicate of US financial institutions paying SOFR plus 300 bps.

In less than a year the 2021 SUNs and cross holders have got their exit, and a decent return.

The formerly pari passu 2024s remain, however, guaranteed by the less profitable part of the group at Intralot BV. They are currently indicated at 88.75-mid, to yield 11.4%.

Flip Flops

Our Top of the Flops for the second half of July landed in 9fin subscribers inboxes on Monday.

The report seeks to reveal the extent of stress and distress in European LevFin. We show how 9fin’s bond and loan screeners help funds and advisors locate opportunities and detect moves.

The market has certainly flipped for the flops, with the sharp drop in Government bond yields – five-year German bonds are now yielding 0.53% compared to 1.51% on 21 June, coupled with around 100 bps spread tightening leading to a sharp decrease in the number of deals trading below 90. The negative convexity effects in prior months have reversed to some extent.

From this sample, 167 bonds from 118 companies are stressed(STW 800-1200 bps) compared to 211 and 138 in Mid-July. In the past fortnight a large number of sterling deals became stressed – many are finance/insurance related – Domestic & General, Amigo Loans, Saga, and RAC.

Moving to distressed (over 1200 bps STW), we have 81 bonds from 59 borrowers – 26 bonds and 17 borrowers less than a month ago. New entrants into distressed in July include Cirsa PIKs, Group Casino SUNs and TDC June 2023 SUNs.

In our latest Flops report, we also looked at cash positions and cash burn.

Running a screener on the above we got 48 bonds on the above criteria. You can then sort the results by net change in cash to identify possible candidates.

Or you can look at companies with say less than 200m of cash and generating less than 50m of cash from their operating activities (btw its 94 bonds from 60 companies). This reduces to 28 from 18 if you additionally filter for above 5x leverage.

There is so much more you can search for – and we are using a number of searches to build 9fin’s watchlist – more on this in future editions of the workout.

What we are reading this week

As Nancy Pelosi’s visit heightens tensions, Ben Hunt suggests that Taiwan is now Arrakis – the fictional planet in Frank Herbert’s Dune – he who controls the spice controls the universe. As the world’s principal suppliers of semiconductors – the spice of our global empire – is now Taiwan.

“Taiwan is now Arrakis. It’s now the most important country on earth. And we WILL fight over it.”

Toucan Protocol, wanted to turn offsets into digital tokens – but Verra, the largest carbon offset brokerage, said it would ban tokenisation – as it was a “mind frying” level of abstraction and distance between an intangible financial instrument and the physical emissions it is meant to represent.

Finally, as the Premier League season starts again this weekend, it seems as if Brighton will lose player of the season and fan favourite Marc Cucurella to Chelsea (for a tidy £37.5m profit mind).

It will mean putting away the Cucurella wigs and we can finally apologise for probably the worst player song in the league: “Marc Cucurella, Marc Cucurella, he eats paella, he drinks Estrella, his hair is ******* massive.”