This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Friday Workout - Keepwell clear of Black Rhinos; Clear but not inert Gas; Green Restructurings

Chris Haffenden

•12 min read

After complaining last week about the lack of contagion from Evergrande, earlier this week virtually every article in the financial media was a primer on the Chinese property developer and why it could (or not) be China’s Lehman moment. Stonks pulled back for the first time in ages as Evergrande finally entered into the wider global public consciousness.

Evergrande isn’t a Black Swan – Citron Research called it out in 2012 - It's a Black Rhino: we knew it was out there, but not if/when it would charge and who can get out of the way in time.

Ernest Hemmingway was once asked: “How did you go bankrupt?”

His answer: “In two ways, gradually, then suddenly.”

With offshore bond interest on 23 September going unpaid (don’t panic there is a 30-day grace period), we saw conflicting headlines here and here on what the Chinese authorities would do after the inevitable default. Avoiding a disorderly default and limiting panic in other property developers I think is high on their list, I suspect international bond funds are less so.

Speaking to a number of advisors, it seems that everyone is angling for mandates of some description. Houlihan Lokey are already company side, and Kirkland & Ellis and Moelis act for a cross-group of bondholders, but with very different security packages for the two bond groups, the smart money is on more committees. Will holders sit and wait for their fate or try to secure some of the equity stakes pledges as collateral?

I expect to see some legal action around the Keepwell agreement (similar to comfort letters) for Evergrande’s Henga bonds with an undertaking that the parent will purchase an equity interest to service the notes– a good explainer here– with some legal thoughts and case analysis here. Similar to the latest Evergrenade news flow there are legal case precedents to offer encouragement for optimists and pessimists alike, but I would caution that for situations of this size politics often trumps the rule of law.

Gnarled EM veterans will remember how useless comfort letters from Kazakhstan's sovereign wealth fund were to Astana Finance bondholders (from 2010 restructuring presentation docs):

Most buyers thought they were buying Sovereign risk but got recoveries of just 22.2% after a six-year restructuring battle which one committee member quipped: “lasted longer than the second world war and wasn’t without its casualties.”

For those who think that history repeats, we are now in the second year of standstills for Nostrum Oil & Gas – the Kazakhstani oil producer. I’m reliably informed there is some recent progress, however.

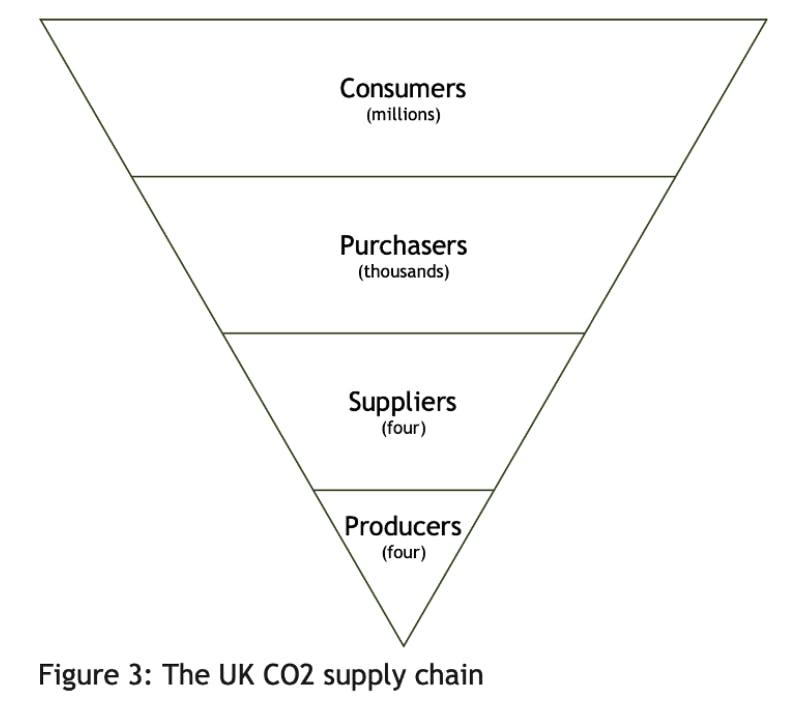

Second on the list of internet searches on Monday was for CO2 – and a slew of ‘what is the CO2 shortage and how it affects the food industry?” primer articles. Who knew most of the UK’s supply came from two US-owned fertilizer plants who would switch off supply if their energy costs rose too high? Probably no-one a week ago, but I suspect a straw poll in the pub tonight would result in a majority of know-it-alls.

This harks back to my second theme of last week - that the foundations of the latest supply issues could stem from pre-pandemic instabilities, reducing resilience.

The BFDF summary reads: “Few people realise that CO2 plays a role in everything from the production of fresh meat to the modified atmospheric packaging that keeps our salads and baked goods fresh. The events in the summer of 2018 showed a lack of resilience in the CO2 supply chain.”

The full report adds: “The UK CO2 chain has a structural weakness: the drivers of supply are unconnected to the drivers of demand. Due to the very low margins on its manufacture, CO2 is only produced in the UK as a by-product of the manufacture of two products with significantly higher value: ammonia and bioethanol. As a result, the supply of CO2 is detached from demand, creating a significant structural weakness.”

At one point this week, we had the bosses of LevFin borrowers Iceland Foods and Boparan calling for government intervention within minutes of each other on national TV and radio, predicting further chaos in their businesses. Remember, this is on top of sharp increases in raw material and transport costs amid unprecedented staff shortages.

In the end the Government caved stepped in and bribed did a deal with the US supplier. But keeping one plant open by paying ‘several millions’ for three weeks as we wait for two continental plants to come online doesn’t feel like a satisfactory solution. I’m not sure I buy into the efficient market’s hypothesis spouted from business secretary Kwasi Kwarteng that the consequent big rise in CO2 prices will suddenly fix the supply/demand balance. In any event, it will further increase the cost pressures on CO2 consumers such as Boparan – whose perfect storm intensifies. Look out for our deep-dive on Boparan - it will be released soon.

Few are talking about the closure of the UK’s Rough gas storage facility in 2017, which used to help with demand/supply imbalances. All this is all happening before the winter season - are we too complacent on security of supply and set for a winter of discontent?

Is this another Rhino?

Green Restructuring

ESG has permeated most areas of finance, most notably LevFin primary, but has evaded restructuring. Some restructuring advisors have often been accused of having egos the size of planets, but up to now caring about our planet hadn’t entered into the factual matrix of restructuring negotiations.

Belize’s sovereign debt restructuring could be the first completed with an ESG element in mind, as this excellent FT piece outlines. Rather than push for 60 cents in the dollar, holders are being asked to take 55 cents in a buyback funded by Nature Conservancy, an environmental group based in the US. Belize will pre-fund an endowment to support marine projects including the world’s second largest barrier reef in return.

Belize is helped by Lee Buchheit, the legendary sovereign debt lawyer - seemingly more busy after his retirement from Cleary Gottlieb than when in full employment, having previously advised Venezuela’s opposition leader on a proposed debt restructuring plan. Reserving a portion of government funds dedicated towards ESG avoids it being misspent, a perennial problem in EM debt borrowers, as the Belize PM candidly says in the FT piece.

I can see how ESG aspects could be used to encourage Sovereigns and large corporations to speed up their energy transition in return for more favourable treatment in workouts, and open up wider sources of funding for their recoveries. It reportedly was under discussion for Ecuador, but the most likely future candidate is Eskom.

South Africa’s energy utility is in desperate need of a restructuring, but it is what my tutors used to say - a wicked problem – something which is difficult or impossible to solve due to incomplete, contradictory, and changing requirements.

Eskom generates energy from around 80% coal – a mix of old inefficient plants which are constantly breaking down, and two huge new plants – Medupi and Kusile, which were partially financed from a $3.75bn green loan from the World Bank in 2010. Massively over budget and beset with operational problems, they were only fully operational this year. The FGD and Nox scrubbers and battery storage plant for World Bank to designate as clean coal green lending never arrived. Worst still South Africa has given Eskom a pass until 2025 to retrofit pollution reducing technology for its ageing clunkers.

Financially, it is only surviving from support from the South African government as it splits into three divisions, generation, transmission, and distribution. It has an eye watering ZAR 440bn ($29.86bn) of debt, much of it backed by contingent guarantees by the South African Government which if crystalised could add another 6% of debt-to-GDP and trigger a double-notch Sovereign downgrade.

The support kicks-in at bond-by-bond level however, meaning that the government will make the payment after 30-days if missed, but this doesn’t trigger a cross-default. Around ZAR 100bn of the debt is held by the Public Investment Corporation – the Government employee pension fund – which floated a debt/equity swap last summer, but this failed to gain political support.

South Africa does have an energy transition plan, the Integrated Resource Plan developed in 2019, which is seeking to reduce the mix from 85% to 59% by 2030.

In recent weeks, there has been a change in position. In July, Deputy Finance Minister David Masondo floated the idea of a sovereign-level debt for climate swap, whereby creditors would forgive Eskom debt in exchange for commitments to cut emissions by shutting down more Eskom coal plants coupled with an injection of equity. But he stressed that these were his personal views, and not the National Treasury.

This week, South Africa adopted a more ambitious greenhouse gas emission target ahead of COP26 next month to 350-420 megatons down from 398-614 megatons set in 2015, suggesting an acceleration in the pace of its energy transition. But it is unlikely to be able to do so without finding a solution for Eskom and a structure to attract ESG-investors into funding the transition. We have heard a lot of talk about blended finance, where DFIs act alongside private investors. Can it solve this wicked problem?

9fin coverage

Nordic Aviation’s forbearance agreement was extended this week from 20 September to 30 September. 9fin’s Laura Thompson outlined that the aircraft lessor is pivoting to narrow bodies requiring additional funding from creditors who are set to take over the business, with some lenders deciding to repossess their collateral instead.

This morning, NAC provided more details of its upcoming restructuring, with a substantial debt/equity swap and $500m of new money ($300m rights and $200m RCF) to fund an aircraft investment programme. Confirming some of Laura’s coverage on aircraft values, it has taken a material impairment on aircraft values leading to a loss of $2.36bn.

KME didn’t explicitly say on its conference call whether it would repay their 2023 bonds with the €200m of net proceeds from the sale of its Special Products division which is expected to close at the end of this year. It expects to complete a borrowing base extension by year-end.“Copper is the new Oil,” they said. But the Germany-based copper products group is seeing strong demand for its end products. However, to fully take advantage it must manage its working capital carefully and preserve liquidity amid sharp rises in copper prices, heavily relying on tolling agreements, borrowing base and factoring facilities.

In brief

There were mixed fortunes for stressed gaming companies in recent weeks.

Cirsa was able to sell €615m of new HY notes at an impressive 4.5% last week, up from €400m initially. But its peer Codere has been less impressive, deciding not to pay the coupon on its bonds this month, but roll this into the restructuring, whose docs were released late on Friday – a massive 13.8MB and 1,845 pages. The aim is to complete the restructuring on bonfire night (5 November). We are working on a closing restructuring review.

Intralot posted an impressive set of earnings last week prompting an equally impressive surge in its 2024 notes which has risen from around 60 at end-August to 87 today. There has been talk of litigation funders and activist hedge funds buying into the debt in recent months to pursue legal action against the Greek gaming company and its controversial restructuring which favoured its 2021 notes. Given the cost and likely length of proceedings – most likely via a fraudulent transfer case – many might be tempted to flip the notes at current levels.

Management on Lowen Play’s Q2 21 earnings call last Friday revealed that they are “heading forward with preparations” for a refinancing of their €350m 5.375% SSNs due 2022 “in the near future”. The regulatory uncertainty surrounding the Interstate Treaty in Germany - stipulating that gaming operators must reduce their multi-concession sites to single-concessionary sites - is near conclusion, helping the bonds rally.

What we are reading this week

Is ESG experiencing a backlash or at the very least a closer examination? We’ve seen the former heads of ESG criticise the attitudes of fund managers – is Larry Fink going to walk the walk – when he says that he doesn’t see Blackrock as a passive observer?

This thought-provoking article in Institutional investor alludes to a Kabuki play in five acts – with us currently in Act III: Ratings agencies, index providers, data firms, consultants, and other financial institutions rush to create environmental, social, and governance (ESG) products, highlighting the opportunity for companies and investors to deliver financial outperformance and social and environmental impact. The ultimate win-win.

But we are close to Act IV: Investors and others slowly recognize that ESG investing, as currently practiced, will not likely lead to financial outperformance and is mostly unconcerned with planetary impact. Act V is a Reawakening to the opportunities and limits of investing to address growing social and environmental challenges.