This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Friday Workout - Playing the Singles Market; default modes; HY as venture capital

Chris Haffenden

•15 min read

At the AFME Leveraged Finance Conference this week, lead arrangers, lawyers, and CLO investors alike remained confident the benign environment and the seemingly endless liquidity can take down record issuance for the remainder of 2021. Sponsors still have huge amounts of dry powder and can readily afford 50% plus equity cheques. The spectres of inflation, rising interest rates, supply chain challenges are not causing sleepless nights, say underwriters.

Deal pricing continues to tighten, with the healthy demand picture aiding and abetting yet more aggressive covenants for the latest crop of deals with the jumbo US-focused Medline LBO deal a standout. I’m told that next week, we will see a deal that will bring another step-change in covenants innovation and nastiness!

But with no immediate triggers and ample liquidity, many think the day of reckoning is several years into the future – so, do our concerns on docs really matter?

The standard investor argument we often hear at 9fin is, if it is a good credit, decent sponsor, then the docs will matter less.

But doc looseness is now filtering into single-B names and racier deals. As the performance of the 2021 vintage crop becomes increasingly divergent since launch - some names losing over 10-points, others above 103, docs matter. This week provided a reminder with Adler Real Estate and Haya Real Estate bonds dropping precipitously into the 80s, initial levels where distressed investors may start to care.

It is only at this point you might start to examine closely what is in your bond documents and reality bites.

You discover the lack of covenant protection and the almost unhindered ability for the sponsor/company to leak value from you. The default triggers you thought were there to give you first mover advantage in distress are not as straightforward.

NB remember to read the definitions carefully. Our legal analysts have been warning about this for months:

Then you might look more closely at the guarantor package and asset sale protections to see what collateral is backing your bonds and how secure it is from expropriation/monetisation. Are you prepared to be primed – do you know how much rescue/liquidity finance debt can they issue above/around you? Trying to establish what is available under the baskets is tricky – don’t worry, in private, sponsors and their lawyers will admit they often don’t know either. 9fin’s covenant capacity tool is a good starting point, however.

Another trend is substantially reduced guarantor coverage and J Crew blockers which don’t provide the protections they should. Another bugbear is the full consolidation of non-wholly owned subsidiaries. In a liquidation/workout scenario do you really know what value you can extract, how easy is it to secure/enforce our security? Do you understand the corporate structure fully - does it have a double LuxCo or DutchCo to protect against debtor filings in creditor unfriendly countries? Do the guarantees/pledges work in all jurisdictions?

For investors, even without external triggers, you will inevitably have the odd deal which enters into distress. Given the pricing environment your entry point is likely to be wrong, and for all the reasons above, recoveries for 2021 vintages are likely to be lower.

2021 deals have aggressive EBITDA add-backs with leverage in many cases much higher than marketed (to be fair this increases the EV multiple too) - our analysis suggests the average add-back in 2021 deals was 20.2%, an average leverage understatement of 0.85x. But if we instead look at the ‘top 10’, the average add-back swells to 88.6% (leverage impact of 3.57x). For the ‘top 20’, and ‘top 30’, this is 63.1% (2.62x) and 50.7% (2.09x) respectively. One AFME panellist commented that European regulators' 6x leverage caps for underwriters has most deals coming at 5.9x – adding that most deals are reverse engineered to hit this number.

HY as Venture Capital funding

To feed the insatiable demand for paper, the types of businesses and use of proceeds from High Yield transactions has changed massively since European deals emerged around the turn of the century.

I remember attending the roadshow for Travelex - one of the first EHY deals. In those days, the company presentation had to show a route to repayment or at the very least a substantial deleveraging. Free cash flow was king, there should be ample interest cover, a route to hard assets and watertight docs.

But it wasn’t long before High Yield became the route for more speculative use of proceeds as alternative telecom providers such as NTL, KPNQwest, Telewest, UPC and Colt Telecom splurged on dark fibre. The deals were sold on overinflated EBITDA and revenue expectations with the supposed asset-value of the fibre network and huge equity cushions (as the new economy hype inflated stock prices) underpinning the investment argument.

This was my first contact with the restructuring professional world, and finding nasties such as structural subordination, vanquished in the US but had been transferred to Europe by US-bankers. Credit to Martin Reeves and Stephen Mostyn-Williams for their subsequent hard work to banish it by the mid-2000s.

Ultimate recoveries for the alternative Telco’s were much lower than expected as the whole sector, with many in the mid-teens at best.

Fast forward to the present day, we have seen the Tech sector re-embrace the HY bond route, with names such as Tesla using it to plug financing gaps as they try and find a route to profitability before going bust. As in 2000-2001 the game is to gain a much higher valuation multiple from being seen as a tech play, with over 50% of companies now claiming to be part of the tech sector.

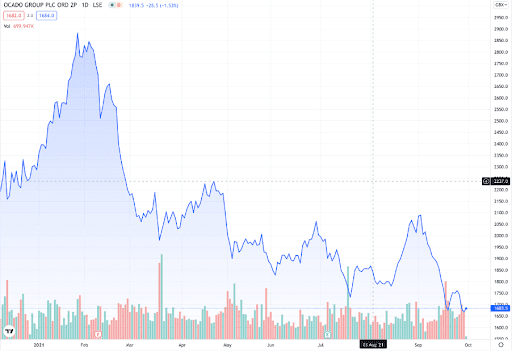

An similar example appeared this week in Ocado, which returned to the High Yield bond market raising an upsized €500m Senior Unsecured Bond, printing at an impressive 3.875%.

Looking at the marketing materials, there is a decent growth in user numbers, in a grocery market which has seen a compound growth rate of 6.8% from 2015 to 2020. Ocado says Covid-19 has accelerated the trend to move online claiming that 80-90% of pandemic surge buying will remain. LTM Consolidated Group adjusted EBITDA has grown to £114.3m to May 2021 from £43.3m to Dec-19. The deal is marketed off a £238m EBITDA figure whose adjustments includes £95m of fees received from ‘solutions partners.’

The LTV is a miniscule 9%, based on a £13bn market capitalisation. FT Alphaville has long pointed the finger at the lofty valuation attached to the business, given the vast majority of its revenues and EBITDA is from online grocery deliveries which should attract a much lower multiple. The shares have halved since their high in February, but still attract a stratospheric multiple. Ocado has taken advantage of rich valuations to issue two convertible bonds in 2019 and 2020, at much higher strike prices.

At this point, I suspect that some of you will want to highlight several new entrants into the online grocery market ranging from start-ups such as Gorilla to Amazon Prime. Competition is fierce.

But Ocado wants to be seen as a tech business not a grocery company. Its future revenue growth will come via Ocado Solutions – a smart platform providing “an end-to-end solution enabling existing grocery retailers to build their online offerings.”

But this division is burning huge amounts of capex and is unlikely to produce EBITDA until 2023 – Fitch estimates around £120m of EBITDA for FY 23. Moody’s expects “significantly negative free cash flows of around GBP600 million in fiscal 2021 and around GBP800-900 million a year in fiscal 2022 and 2023.” It adds that Ocado is likely to have a funding requirement by 2023 – despite a current cash balance of £1.8bn.

So as a bondholder how comfortable are you with Ocado as a business?

The retail joint venture with M&S has strong growth, but conversely, the solutions business is a huge cash drain. Ocado is taking out an existing HY bond, so surely investors must know the business and its credit dynamics already?

But here comes the twist, and it’s a biggie.

As our TLDR reads from our legal QuickTake says: “The Ocado Retail JV, which generates most of the group’s revenue and EBITDA, sits outside the Restricted Group, so will not be subject to the covenants or provide any credit support. There is significant covenant capacity to pay dividends and to invest further in the Ocado Retail JV and other entities outside the Restricted Group.”

That’s right, despite being consolidated under IFRS – the 50/50 JV with M&S which produces 93% of revenues and 91% of cash-adjusted EBITDA will not be subject to covenants or provide any credit support for the bonds. Worst still there is plenty of capacity for value leakage – for example, the company can pay up to 5% of market cap (that’s £650m per year!) in annual dividends.

So, what are you left with?

Bondholders appear to be funding the solutions business liquidity gap, with less than a year’s worth of headroom. If Fitch is correct, then leverage will be around 5x at this point, but what price do you factor in for execution risk? Is HY the appropriate funding instrument for this risk - isn’t equity or more converts the better option?

There are other potential headwinds too, Ocado is locked in a patent dispute with autostore over robot assisted technology patent breaches which has escalated fast and is currently in the US courts. Its robots have a habit for creating mischief too, causing a fire in its Erith fulfilment centre in July. According to the company this has cost £35m in lost revenue and £10m in lost EBITDA.

Ocado user personas are likely to be more ESG sensitive than most and might be interested in our ESG QuickTake. In 2021, Ocado delivery drivers went on strike after reports of less than minimum wage and poor working conditions under a third-party delivery provider. Ocado is quick to highlight their environmentally friendly fleet, its natural gas plant and a target of 1 in 3 LGVs being CNG trucks (running on blended biomethane) by 2021. However, as our analyst Jack David notes this is not likely to be the most efficient strategy given a CO2 saving of only 29% over traditional fuel use. In addition, it must transition its vehicle fleet to EVs by 2030, under UK government plans.

9fin coverage

Restructuring activity remains low, so in addition to looking at stressed refinancing candidates, we are focusing on underperforming single-B’s. Emmet McNally, our new distressed analyst has produced a report on Boparan whose bonds have fallen from par in Mid-March to the high-80s to yield 11%.

Despite the attractive return potential, the investment thesis is fraught with risk, according to our report, as the company contends with a growing list of challenges and the balance of potential triggers on the horizon appears more weighted to the downside. There are question marks in our minds as to whether the company can grow into its capital structure, even though the recent refinancing and the use of disposal proceeds reduced the capital stack; following on from the trend in previous years in which disposal proceeds were used to manage the balance sheet.

Those who have read our court coverage on the Caffe Nero CVA case will not be surprised that the single-landlord challenge has failed. Funded by EG, Ronald Young sought to overturn last year’s CVA. Nero Holdings Limited proposed a CVA offering unsecured creditors 30p in the pound, with landlord creditors receiving part payment for their arrears. The deadline for votes was Monday 30 November 2020. But, at 8.48pm on Sunday 29 November, Kirkland & Ellis, acting for EG sent an unsolicited offer to acquire 100% of the shares of Nero Holdings Limited for an EV of £350m to £400m on a cash free and debt free basis. It offered to pay landlord arrears in full.

In his Judgment, Justice Green said: “There is no basis to conclude that the EG Offer suddenly meant that if the CVA failed all the landlords’ rent arrears would be paid in full. Such a conclusion would be contrary to the way the relevant parties would have acted in their own commercial interests and could not therefore be considered a likely, still less the relevant, alternative to the CVA.”

We will publish a more detailed analysis of the ruling in due course.

In brief

Just after we had put in calls to stakeholders on the progress on the second Scheme - Amigo Loans finally provided an update this week. It has submitted the draft of its practice statement letter to the independent complaints committee and its regulator the FCA for comments before publication. As reported, it may have set up a burning platform by dramatically increasing its provisions for potential compensation claims. Accompanying the AGM statement, the UK guarantor lender gave an update on its cash position and its remaining loan book.

Italian ferry operator Moby appears to be in dual-track negotiations with its bondholders. Earlier this week it announced that it had entered into a non-binding Memorandum of Understanding (with an ad hoc group of bondholders who together hold in excess of thirty-three per cent of the €300,000,000 7.75% Senior Secured Notes due 2023) to engage in negotiations for “providing the additional financial resources necessary to support a new composition plan to be submitted to Moby Group financial creditors.”

But days later it emerged that Moby had filed a complaint in the US courts which claimed that “Italian vulture investor Antonello di Meo and Morgan Stanley and its subsidiaries attempted to illegally acquire control of Moby S.p.A., one the world’s largest passenger shipping companies based in Italy. They are doing so by trying to acquire a majority of Moby’s bonds at a substantial discount using inside information so that they can assume control of, liquidate and dismember the Company.”

Sticking with ferry operators, Norway’s Hurtigruten has secured a €75m subordinated shareholder loan which it says will be utilized for general corporate purposes, working capital needs and investments to drive growth as HRG is coming out of the pandemic. The funding will further strengthen HRG’s liquidity position when returning to full service over the coming months and demonstrates the strong support The Company has from its shareholders. Its bonds rose from 91.5 to around 95 on the news.

Spanish ferry operator Naviera Armas finally released details of its restructuring plan, which had been amended after the sale of its five Balearic route vessels to Grimaldi. There will be a conference call to discuss and present the proposal on 11 October. To summarise, following the release of an outline proposal in the spring, the M&A transaction was agreed, which according to Naviera will provide an additional €51.5m of additional liquidity and deleverage the capital structure by a further 1.1x. Watch out for a Restructuring QuickTake in the coming days.

It was a poor week for real estate names, but as far as we can tell the drivers were not Evergrande.

Haya Real Estate November 2022 bonds were hit hard by a local Spanish media report that Houlihan Lokey had been hired to restructure its debt by major shareholder Cerberus. Our gut feels this is more of a debt advisory role, with an A&E most likely rather than a full-blown restructuring. But nonetheless, the bonds took fright, dropping from 87 to around 82, before rebounding to 84, now.

The German Real Estate HY complex is traditionally skittish, with short-seller reports, concerns over opaque transactions and common-ownership causing sharp moves often with little evidence to back them up. But pressure is building, Berliners have voted to expropriate up to 240,000 properties from developers, with Adler having 20,000 in the city alone.

Add in uncertainty from the German election, a parliamentary inquiry into past deals, has caused Adler’s bonds to fall from 95 to 87 this week. Aggregate Holdings with a 26.6% stake in Adler fared even worse, their 6.875% 2025 bonds which were trading at 98 in early September fell from 88 to 80 this week.

What we are reading this week

The Workout tried (as much as possible) to avoid the doom and gloom around supply chains and speculative pieces on what is likely to happen to Evergrande this week.

The New Yorker has an incredible tale of Ozy, a digital media company trying to dupe Goldman that the head of digital programming for YouTube was on the call. In reality it was an Ozy employee whose voice had been altered. Not unsurprisingly, Goldman decided not to provide the financing, but this hasn’t stopped them raising funds elsewhere, with no-one being prosecuted for the attempted fraud.

One of the banker mantras is the ABCs – Always Be Collateralising.