This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Friday Workout - Red Flags and Red Lines are Never-Grande; Supply teaches lessons

Chris Haffenden

•16 min read

The Friday Workout returns after a week spent in reset mode ahead the expected frantic run into the year-end. Aside from doing admin and asset servicing neglected in the past few months, there was time to think about the bigger picture – for risk markets and our 9fin editorial offering. I hope you found Owen Sanderson’s Excess Spread a useful addition and compensation for a lack of workout activity.

I didn’t completely disengage; you might have spotted my Red Flags post on LinkedIn:

Two of the greatest risks to the Goldilocks scenario for global risk assets are the bursting of the Chinese credit bubble and/or the potential for a Crypto collapse causing systemic shocks.

In recent weeks, a number of red flags (pun intended) were raised in relation to China. Political interventions have caused a crash in Chinese tech stocks; and their belated attempts to rein-in property lending may mean the government countenancing an orderly default for Evergrande, which no longer feels like being too big to fail.

Leaving aside President Xi’s Orwellian digital agenda - and where it could end-up - there has clearly been a change in attitude by the Government to Chinese Corporates in recent weeks.

Since my post, the troubles at Evergrande have accelerated, with a hard default more likely. But the wider effects so far are minimal, as I posted last week:

But looking at other risk markets, you would be hard pressed to know that this is happening. Where is the contagion? Why is there no correlation between Chinese HY - now yielding 13% and HY in Europe and the US, which remain at all-time lows and have barely moved?

Arguably, September European High Yield sentiment is even more bullish – witness Spain-based gaming operator Cirsa’s ability to print €615m of bonds this week at 4.5% - prompting a US FinTwit to post: “F*ck. CIRSA is still a thing? And they borrow with a four handle? Europeans are nuts.”

I digress, back to Red Flags:

During 2018 and 2019, the collective belief was that China is the biggest driver of world demand and therefore the swing factor for markets. Shifts in trade tensions between the US and China would move stock markets 3-5% in either direction on daily news flow.

So, what has changed? Why are we so insulated now from the clear value destruction going on in China? Do we believe that the Chinese Government has this in hand and can engineer a soft landing while still taking the excesses out of the system?

I agree with Wolf Richter and The Economist. Foreign investors were suckered into believing that the Chinese government would bailout property developers given concerns about systemic risk. Chinese property is intrinsically linked to the entire economy (around 28% of GDP) and the household wealth of its population: “housing often serves as collateral, nest-egg, speculative investment, bride-price and ticket to a good school. Housing makes up three-quarters of household wealth,” says the Economist.

Talk of an impending Chinese property crash was rife for years – with pictures of Ghost Cities going viral – the Beijing Morning Post reporting in 2018 that the number of empty apartment properties in ghost cities may be as high as 50 million – 22% of all urban housing stock, and set to double by 2020. The estimate came from the State Grid Corporation of China, based on the number of completed apartment buildings that have not used electricity for six months.

But each market wobble for developers prompted indirect and direct state support. Therefore, Foreign investors were happy to buy bonds from developers with little documentary protections at entities as far from the operating assets as they were from Beijing at high single-digit yields, often with little due diligence, buying into the moral hazard argument. Chinese retail investors were encouraged to buy wealth management products offering leveraged exposure to the overheated property market at similar yields. Blurring the boundaries even further some developers such as Evergrande became increasingly reliant on offering these products to shore-up their own financing.

This summer the Chinese Authorities doubled down on their concerted efforts to reduce inflows into the property sector, removing exemptions on disclosure on funding sources such as CP, imposing restrictions on mortgage approvals, with talk of a national property tax. The collapse of China Huarong Asset Management and its subsequent rescue plan by CITIC has sent shockwaves across the sector - yesterday it put up $58.8bn of bad assets up for sale.

It’s now clear that the government may be willing to let private developers’ default.

The key questions are do offshore bondholders take the biggest hit; can the local banks and more importantly SOEs survive the effects; and are we too complacent on whether this could trigger a wider financial crisis?

After all, it is only when the tide goes out, we find out who is swimming naked.

I recall a financial advisor telling me post GFC how he had to explain to small Norwegian Town treasurers and mid-Western US Mayors via painful conference calls, his slow progress on retrieving asset value for topmost AAA tranches in structured investment vehicles (their recoveries were much closer to zero than par, btw).

In a past life, I remember the whole trading floor at my Investment Bank hanging on my every word at our morning meeting as Russia flirted with default, with the entire capital markets division worried about and experiencing the fallout via contagion. Perhaps it’s relative – the August 1998 default wiped out the entire FIG P&L for that year not just for us, but also for Deutsche, BNP and Credit Suisse.

I will leave those thoughts hanging, but in the meantime, while I don’t profess to be an expert on Chinese Property, let’s survey the situation at Evergrande.

Never-Grande

Founded in 1996, Evergrande is the second largest property developer in China with an estimated $305bn of outstanding debt, with concerns there may be more. Despite diversifying into hotels, finance, internet, healthcare, tourism, and electric vehicles, property development still made up 97.5% of revenues in FY20. Chairman Hui Ka Yan and his wife retain a 76.6% stake, but the stock now trades for cents (strong support at zero).

In August 2020, concerned about excessive leverage in the property market China introduced its three red lines policy with criteria set to encourage developers to deleverage.

The three red lines were:

Total liabilities/Total assets ratio less than 70%; Net debt to equity less than 100%; and cash/short-term borrowings greater than 1x.

Companies are scored red/orange/green depending on how many lines they cross - those in the red cannot grow their debt burdens annually. Scarily, UBS in January 2021 said that just five out of 52 large developers were in the green.

Evergrande by this time was highly dependent on its lending banks to roll over debts as it was unable to tap offshore bond markets since January 2020. It needed to maintain a healthy level of pre-sales of properties – these had risen 20% YoY in FY20, but as Bloomberg reported in September 2020, their latest sales round came with a 30% price cut promotion – the deepest discount ever.

Evergrande said in March that it would seek to reduce its debt load by 51% from January 2021 to June 2023 mainly from equity raises, reductions in its land bank and sales of non-core assets. But despite these measures it said it would be unable to pass the red lines test until the end of 2022.

Earlier this year the Chairman exhausted the generosity of his poker playing buddies to raise funds. By mid-summer it was apparent that Evergrande was struggling to monetise its assets, despite offering deeper and deeper discounts to book values, with talk that it had approached SOEs to sell property projects – its land reserve was valued at CNY 490bn at end 2020.

With the SEC tightening disclosure requirements for Chinese companies, it was becoming harder to list businesses abroad, most notably its Fangchebao real estate and automotive matching platform. Worst still if it couldn’t list it on a suitable exchange by April 2022 for CNY 150bn – it would have to buy the $2.2bn of shares earlier this year in a pre-IPO sale to a group of investors at a 15% premium.

In August, Evergrande’s situation became yet more precarious. It failed to pay suppliers and contractors and warned of a possible default if it was unable to raise further funds. Talk emerged that it was offering properties in lieu of payment to some contractors.

As Capital Economics outlines pre-completion deposits from households now account for the bulk of the company’s liabilities.They estimate that Evergrande had RMB1.3trn in presale liabilities at the end of June, equivalent to roughly 1.4 million individual properties that it has committed to complete.

Last week, Chinese regulators signed off on an Evergrande group proposal to renegotiate payment deadlines. This week the Chinese Housing Authority notified Chinese Banks that no interest payments would be made on 20 September. On Monday, wealth products investors protested in front of the group’s headquarters with many unwilling to agree to a two-year deferral offer on repayments. The company said that online speculation about its restructuring and bankruptcy were “totally untrue.”

Evergrande Bonds which were trading in the 50s in early August (and over 80 in May) dived into the 20s and 30s this week. But some participants believe recoveries could be even lower.

So, what happens next?

My gut feel is that this will get political - will they prioritise the wealth management products to protect retail investors, and/or give away value to trade creditors and those who have put down deposits at expense of foreign creditors?

The offshore holders will probably organise – at least two separate groups likely (as debt sits at two very different levels) – the company side likely to seek forbearance and try to avoid cross defaults first.

I agree with Capital Economics that policymakers will likely prioritise those which have handed over deposits for unfinished properties. They suggest that over developers will take over these projects in exchange for a share of its land bank.

In the meantime, prices for bonds of other Chinese property developers are getting demolished. Fantasia Holdings bonds fell up to eight points yesterday despite a message from the company that it has funds escrowed to repay $208m of bonds due on 4 October. Its October 2022 bonds are bid at 50.

Supply teaches lessons

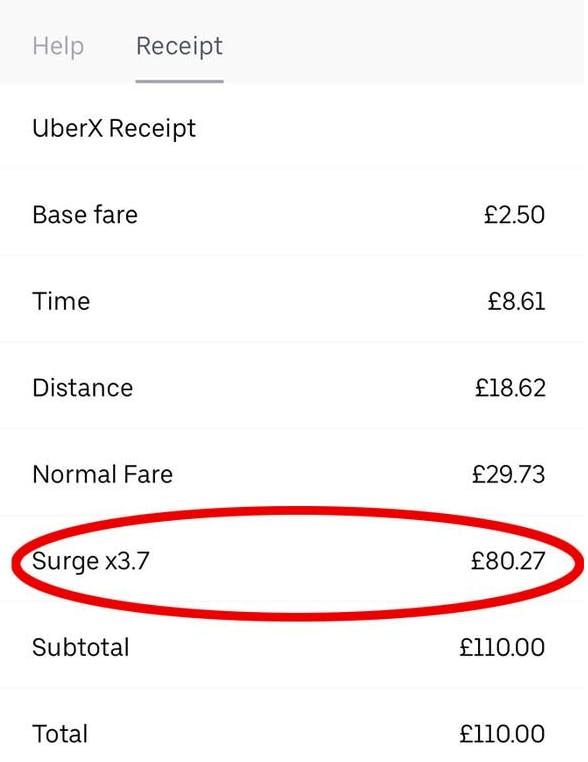

Earlier this week I got an email from Uber:

“Experienced a higher price than usual, Chris?

We always try to ensure our riders get a fair upfront price, and we apologise for any inconvenience this high surge pricing has caused you.”

I will save you the sob story. The background is that I paid more than double the cost of my expected journey back from Hackney’s finest craft beer and pizza combo to south of the river after the last DLR.

Speaking to friends and colleagues past and present it's clear that Uber prices and those for a number of other services have risen significantly since lockdown. Many blame lack of drivers, Brexit, and rising input costs, but is there something more fundamental at play here?

“At the time, everyone knew that Uber, and its tech economy cousins, were heavily subsidized by investors, with Uber losing up to $1 million a week. But the cheap rides were too good a deal to pass up. It couldn’t last forever, and it didn’t. Slowly, cabs, under pressure from ride shares, disappeared. Taxis had been a reasonable business in D.C., and the drivers had middle class lifestyles, but there was a tipping point, and the industry collapsed. Similarly, driving for Uber, once a reasonable side job, became worse as the firm cut the amount paid to drivers. Now, cabs are mostly gone. And today, ride shares are often a ten-to-twenty-minute wait, and more expensive. It’s not just a D.C. problem; nationally, Uber/Lyft prices up 92% over the last year and a half.”

We have all heard the stories of HGV drivers changing jobs during the pandemic to deliver for Amazon and the latest conundrum of record job vacancy levels despite lower than pre-pandemic employment numbers. Covid has changed our habits and our just in time supply chains and lean business structures were proven to be unable to cope. Shortages can encourage greater hoarding which makes the shortages and delivery times greater.

But Matt also believes that supply chain issues, goods and labour shortages may not just be the result of the disruptive effect of Covid and subsequent policy decisions to mitigate its effects. He cites a recent White House blog as evidence that monopolies (I would say Oligopolies, btw) manipulate prices and reduce supply in the food industry. Arguably, there are echoes in the private equity model of roll-ups and focus on market concentration and pricing power.

Over the years, supply chains have become less resilient as the number of players and buying options have become more concentrated. Parts are no longer sourced nearby, often they have to be procured from abroad, with more co-dependencies creating bottlenecks. The solution isn’t more container ships or containers – it is finding ways to process the 40 ships sitting outside Long Beach more quickly. The limiting factor is not capacity on board ships, but rather how many containers the ports and hinterland connections can manage, as well as storage space in temporary container yards and final destinations.

I may disagree somewhat with Matt’s political views, but I mostly agree with his conclusion:

“A lot of people look at the economy over the last year and a half and see the shortages that we’re having as a result of the pandemic and the resulting supply shock. But while Covid provided the spark, it also leveraged pre-existing fragilities existing all over the economy, including some shortages that were long standing before the disease emerged. What all of these examples I offered have in common is the basic idea that when a monopolist concentrates power, that monopolist also concentrates risk.”

In brief

This week saw a number of earnings releases for some recent stressed financings, for names such as McLaren, Tullow Oil plus special situations such as KME and Intralot.

We are revising our watchlist and will be working on a series of deep-dives and bespoke reports in the coming weeks, please bear with us as we play catch-up.

While we await legal moves from disgruntled Intralot 2024 holders, there was an impressive set of H1 earnings to digest on their earnings call on Monday. The performance of the US business was strong (save sports betting) but the Rest of the World was below expectations, which the company explained was due to future opportunities which did not materialise. The Greece-based gaming company said it was targeting €100m of EBITDA this year and says it will hit its 5x leverage target “in the near future.” More worrisome for 2024 holders - which lost value to the exchanged 2021s which grabbed security on its Intralot Inc, US subsidiary via a controversial restructuring - the company said on the call that it wanted to leverage its equity in the US business and create upside. Could this be an attempt to grab value before the 2024s have their day in court?

Travelex has tapped their bond investors for a third time in a year - with an additional £15m announced this week to support the recovery phase and the rest of 2021. The FX provider said that H1 had been significantly more difficult than forecast, with revenues at just 10-20£ of 2019 revenues in key territories. On a more positive note, all businesses outside APAC were in positive territory in August with £1m of positive EBITDA. It said EBITDA losses for FY21 “are unlikely to exceed £60m” with revenue recovery rates up to 32% by the end of the year. It projects £20-30m of EBITDA for 2022. As working capital increases to meet demand it will need additional funding requirements. Travelex says it is in conversations with existing shareholders and third-party financing providers.

Tullow Oil now sees value in its Kenyan assets. But the UK-based E&P producer needs strategic partners to fund the hefty development costs. In an investor call to accompany their H1 results, they confirmed their target of $1bn of FCF by 2025 to deleverage below 1.5x but admitted under questioning that most FCF would be back ended. If maintained, higher oil prices could help accelerate investment plans in declining Ghanaian fields to stabilise production and bring forward decarbonisation measures. Tullow management confirmed the recent receipt of a $471m tax bill from the Ghanaian Government, adding that the lack of any provisions for this in their accounts is due to confidence in their ‘strong legal position’.

What we are reading/watching this week

The SEC and US politicians’ attention on Stablecoins and their belated attempts to regulate Crypto, also feel like a Minsky moment. I would highly recommend Matt Levine’s piece on Coinbase’s Lend product difficulties - should they be regulated as securities or as a Bank?

One of the reasons for a sharp increase in shipping and container rates was the discipline from operators to avoid a capacity glut and break the boom bust cycle. But as Bimco outlines new ships are now being ordered, which could create oversupply in 2023/24 onwards.

Who can forget the Hindenburg takedown of the Nikkola electric truck slowly using gravity to power down a gentle slope? This week, the new CEO invited journalists to test rides, saying “It’s real I promise!”

Regular readers will already know my thoughts on the pricing of risk assets and the bizarre effects of policy actions over the past ten years and the apparent inability to reverse course. Matthew Piepenburg has summed it up perfectly:

“When it comes to modern markets, risk assets and the now normalized yet twisted tango of fiscal and monetary policy gone wild, it’s safe (rather than sensational) to simply confess that nothing is real.”