This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Friday Workout - Tweets, Beats, and Repeats; Rescissionary pressures; Getting forensic on Adler

Chris Haffenden

•19 min read

An interesting, exhilarating, but also tiring week at 9fin Towers. Our Twitter debt financing explainer, podcast and tweets elicited a lot of interaction from FinTwit. Our Tweets on Elon’s bank financing started trending with some conversations going for several hours. Respondents were right across the bandwidth of debt knowledge, with a lot of misconceptions about the debt package and the metrics.

We even offered @elonmusk some advice in shaving a few bps off his funding costs and freebie access to finance grads.

Our long and hectic week had started early, with weekend reading of the 121-page KPMG Forensic report into Viceroy’s allegations against Adler Group. Despite new Chairman Stefan Kirsten telling investors last Friday that there was no confirmation of a smoking gun in the report, on deeper reading a lot of concerns were raised by KPMG – more later in the Workout.

Klaxons blared on Monday with the return of primary after a 77-day absence, as we were scrabbled to our desks to work on the various QuickTakes. A single-B sterling deal for Miller Homes, sponsored by Apollo, wasn’t the deal we’d expected to reopen the EHY market.

But, despite the issuance hiatus and a reasonable credit story, the deal wasn’t going to the moon.

Price talk widened as the week progressed. At the time of writing pricing is north of 8% for the fixed tranche. This is well up from initial whispers of low 7’s, which then rose to 7.5-7.75%. Bookbuild wasn’t helped by news that around £1.07bn of Morrison’s SSNs were privately placed at a 8.3% yield . It carried a much better rating than Miller — bagged by undisclosed shoppers at a heavily discounted price to the leads’ pricing caps. Put simply — more reasons to shop at Morrisons.

It showed how severe repricing for HY is, and how stormy the market remains with the crossover back above 400bps this week. Head-Windy Miller Homes could be re-housed in FRNs.

With the 120-day reporting window for FY results set to close, we saw a phenomenal number of earnings on Thursday, with plenty more expected today.

Despite our superior tech in uploading financials, our large analyst and journalist team couldn’t cover-off all the earnings calls and I will have to skip read 40-50 investor presentations and revisit a few replays early next week. Surely, HY analysts can push for companies to coordinate their releases to avoid overcrowding, or do some companies like to hide in the melee?

As well as a few earnings beats and plenty of repeated misses, there was more clarity around Russia and Ukraine impacts in Q1 updates, as Russia ramped up pressure for gas payments in Roubles. Worryingly it appears that corporates resolve appears less firm that governments.

Wepa, Ardagh and Atalian were suspects of concern for us this week, but other fixed-rate price penalties were dished out to Diebold Nixdorf, Ideal Standard, Oriflame, Upfield Flora, Bulgaria Energy Holdings, Upfield, Rallye and Douglas – all 5% plus decliners, as were our German RE friends (or should that be friendless), Adler, Aggregate and Corestate who topped the movers.

East/West relations

Many of those directly affected by Russia/Ukraine update have made significant progress on their plans to protect their operations. But in their attempts to ring-fence their operations and prevent contagion in their Western European operations is bondholder long-term value being deprived?

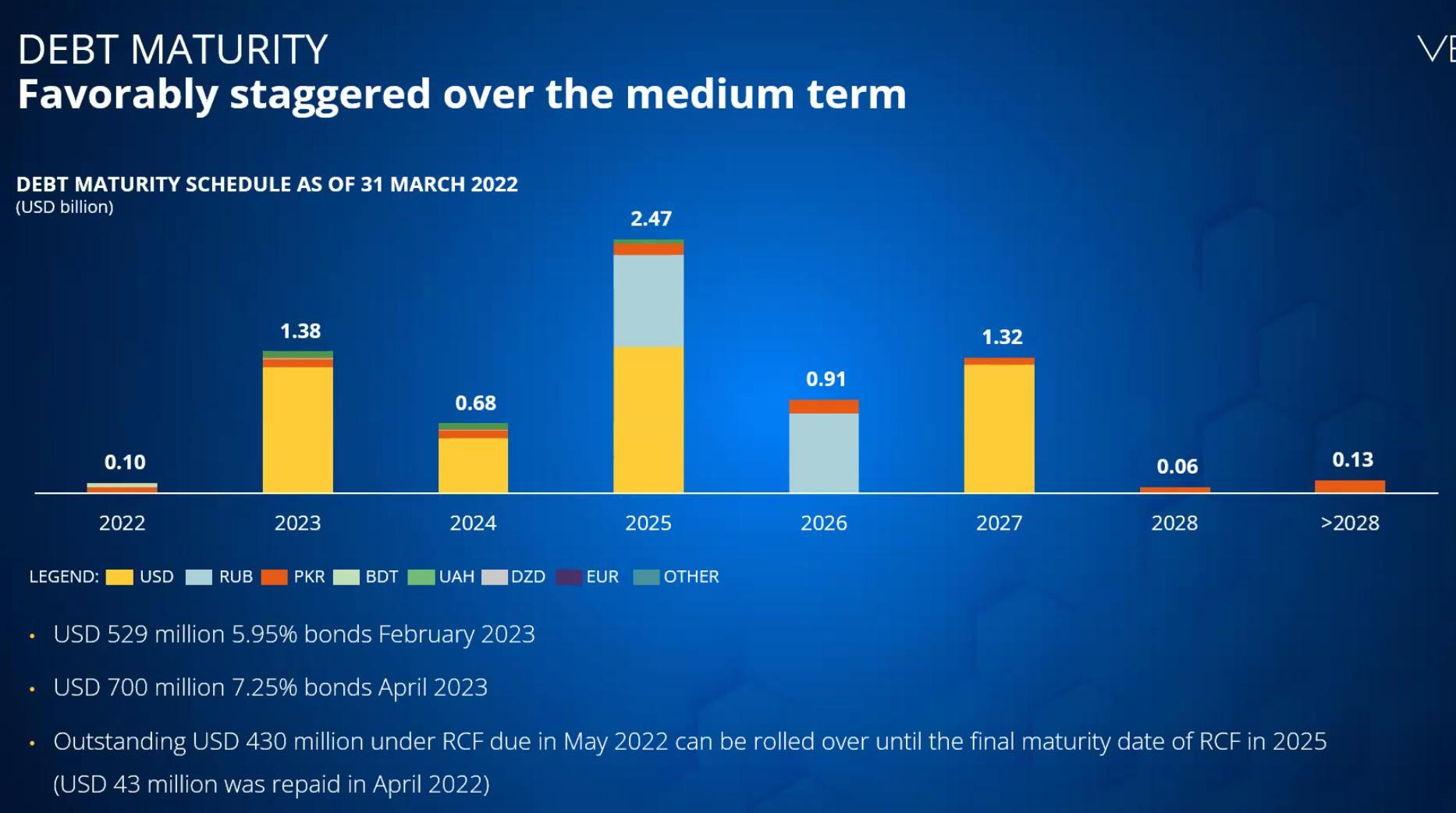

Russia and Ukraine made-up 64% of Veon’s Q1 EBITDA. With a sanctioned oligarch as beneficial owner, and an early March 2022 maturity, the Dutch-headquartered Telco had to act fast.

With Mikhail Fridman’s LetterOne owning a 48.7% stake, Veon’s dollar bonds were hit hard in late February over concerns on access to facilities to repay the March 2022 notes, diving to around 40 cents in the dollar. Fridman has since resigned as CEO and from the board, with company emphasising it is not sanctioned. Revolver access was maintained to allow repayment of a March bond maturity, with no further maturities at Dutch BV level in 2022. It’s dollar bonds, however, still trade at distressed levels despite a 20-point recovery into the low-to-mid 60’s.

On an update call yesterday, management said that Kazakh operations would be transferred to BV level to provide credit support to the bonds. A RUB 30bn loan to VTB was recently repaid, meaning that there is no further exposure to the sanctioned Russian bank. It points out holders of the rouble MTN notes issued out of the Dutch BV parent can still elect to be paid in dollars.

In a move to separate financing of its Vimplecom subsidiary and its operations, loans made by Sberbank and Alfa bank, totalling RUB 90bn ($1.07bn) were recently novated to Vimplecom, the Russian subsidiary. This resulted in the release of former borrower Veon Finance Ireland and former guarantor Veon Holdings BV. Following this move, the “external debt” is now $4bn of dollar bonds, RUB 50bn ($690m) of rouble bonds and $430m of drawn RCF (used to repay the March 2022 notes from the $692m committed facility).

There remains around RUB 57bn of inter-company debt with Vimplecom, and $125m the other way between it and the Dutch BV, said management. No cash would be upstreamed from Russia this year, they added. There is a Russian law forbidding this, but an application for a C account license from the Russian Central Bank to transfer funds out of the country is being made.

Net leverage is 2.4x, but this rises to 4.6x if you de-consolidate Russia and Ukraine. $1.229bn of dollar bonds are due early next year, and while non-operating assets sales are planned to boost liquidity, releasing guarantees against the main earners will make it harder to extract value, as you are relying on dividends from Vimplecom to the parent.

Bondholders have reportedly hired Houlihan and Milbank, and if things turn sour, it could be one of the biggest restructurings of 2023, with over $5bn of debt to reschedule.

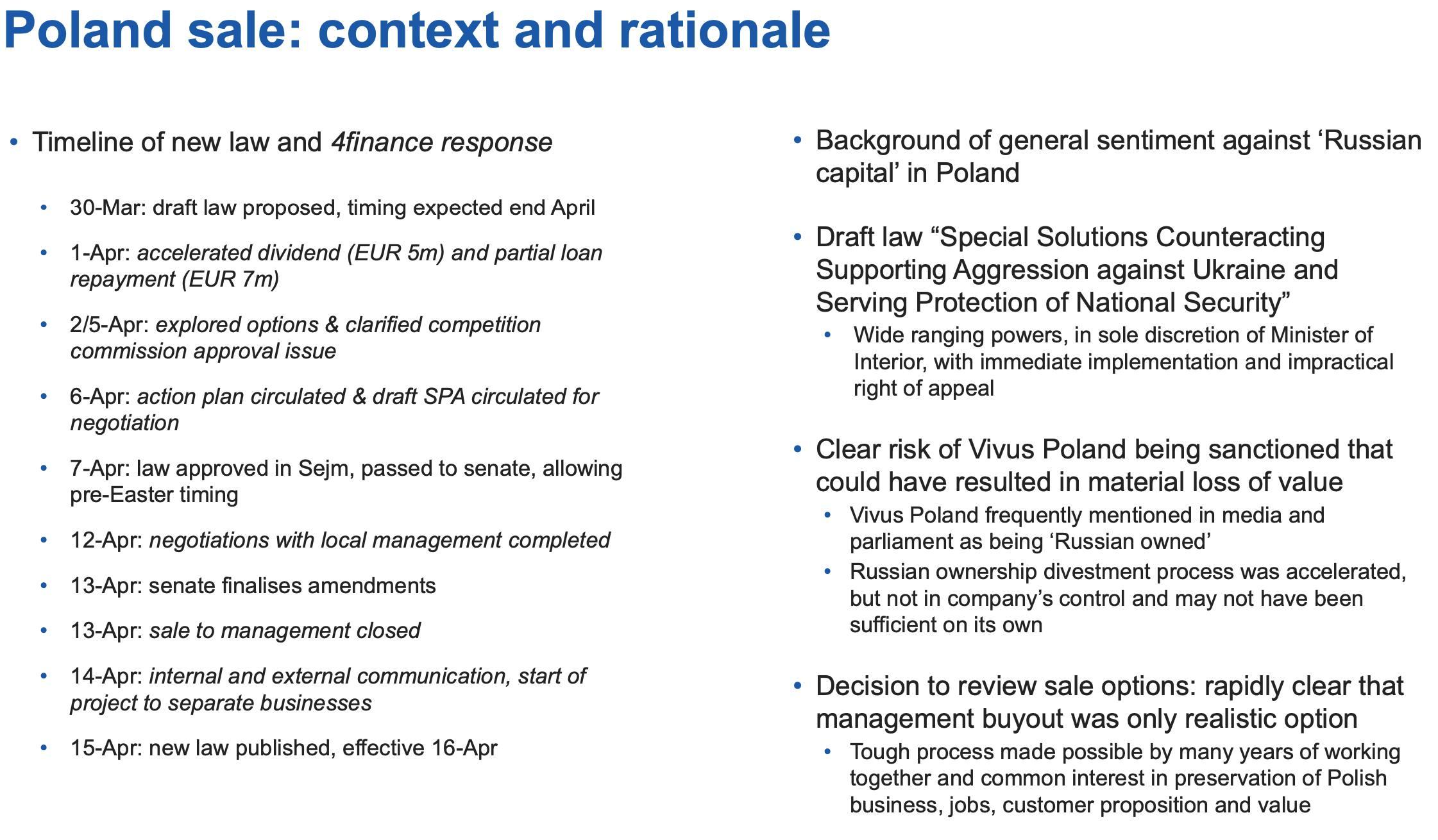

4Finance’s Russian connections have also created problems for the subprime small loan lender, causing it to distance itself from its prime revenue earner. The largest beneficial owner, Vera Boiko, is a Russian citizen (albeit like Fridman with Ukrainian family members and donations to Ukraine) and this has created a stir within Poland, 4Finance’s most profitable market.

Boiko has now sold her 49% stake, but this wasn’t enough to remove sanctions risk in Poland. 4Finance said it had explored sale options as per the slide below, but decided that a MBO was the only option.

Source: 4Finance investor update

In total just €18m is being paid by the Polish management team, in three instalments, with a €30m loan from 4Finance remaining in place. The price paid is at the higher 3-5x peer multiples, with the company adding that covenant compliance has been reviewed by bond lawyers. Our legal team also took a look, but as it is not a NY style bond, they say the covenants are uncomplicated, with no requirement to apply proceeds of the asset sale to the bonds.

Holders have lost an asset which contributed around 20% of EBITDA to the group in 2021. As S&P outlines, some related risks remain, outside the bond perimeter, the intermediate parent owns a 55% stake in Ferrymill Ltd, a Russian single payment loan provider. “As a result, we think that any problems in realising the value of the investment in Russia could also have a financial impact on 4Finance, through the related party loan.”

Alleviating Rescission(ary) pressures?

The legal complaint lodged by UMBM — the Intralot 2024 trustee in the Southern District Court of NY — came in too late for last Friday’s Workout.

The successor trustee alleges various breaches of the 2024 bond indenture provisions “in connection with a collusive and coercive integrated transaction engineered by the Intralot Entities to impermissibly strip the 2024 Notes of their bargained-for credit protection of the Intralot Entities’ most valuable asset…” via which it says is “an illicit scheme.”

Damages and equitable relief are sought by the trustee, who has also asked for rescission (something that I had to look up in the legal dictionary) — that is for the contracts to be set aside and the parties put back to their previous positions.

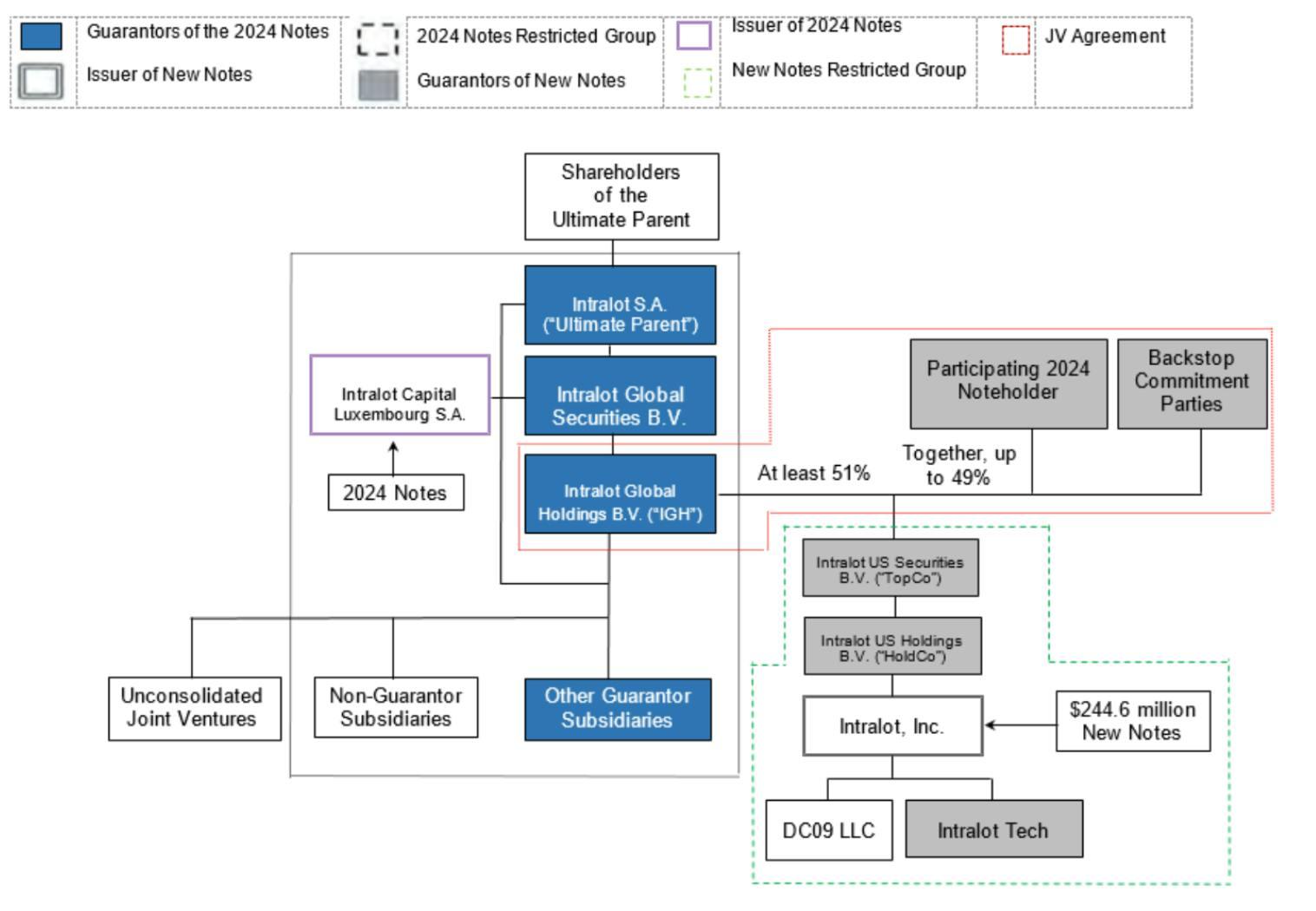

As reported, last August’s restructuring plan gave disparate treatment to the 2024s compared to the pari passu 2021s. The €250m September 2021 SUNs were exchanged for new $244.6m senior secured notes due 2025, issued by its US subsidiary Intralot Inc. The 2024s however, were offered a partial exchange into 49% of Intralot Inc equity, and to avoid breaching restrictions on secured/priority debt incurrence, Intralot designated the new US topco and its subsidiaries as Unrestricted Subsidiaries, resulting in the US group no longer being subject to 2024 notes restricted covenants, triggering the release of the 2024 Notes guarantee from Intralot Inc, the issuer of the new 2025 secured notes.

With 2024 holders holding a blocking stake in the 2021s, Intralot took an innovative, two-step approach to achieve the necessary 90% consent threshold – partially redeeming the 2021 Notes and then replacing them with additional locked-up / consenting notes.

Regular readers will be aware of the legal arguments for the first European restructuring to use a drop-down Unrestricted Subsidiary financing structure, borrowing elements from J Crew.

As outlined in our analysis on 7 July there are two main arguments being advanced by the 2024s.

The first is that Intralot is unable to use three baskets – a Restricted Payments general basket, plus Permitted Investments general and investments in joint ventures baskets. The 2024s believe under their interpretation, the company can only use either RP or PI capacity, not a combination.

Secondly, the 2024s believe that the US business, which provides the bulk of wider group profits, constitutes “substantially all” of the group’s assets and therefore would trip the change of control and/or the merger covenants under the 2024 notes indenture.

Until now, the full mechanics and the cleverness (or deviousness depending on your view) of the transaction lawyers were not known. There was some hint on how to reduce the fair market value to allow the transfer in a hearing last August for a temporary restraining order, but the exact sequencing was laid out in the latest complaint by Quinn Emanuel, their legal counsel.

The sequencing transaction consisted of four-steps, allege the 2024s in their complaint.

Firstly, at midnight the 2024 notes that elected (mostly a cross holder group) to exchange their SUNs for a share in the US Topco resulting in a reduction in ownership from 100% to 65%

Secondly, €202m equivalent of dollar debt was created at Intralot Inc for no consideration. The 2021s were exchanged for new notes at Intralot Inc (the crown jewel) — at this point no liens were granted as this was not permitted under the 2024 indenture, meaning they were unsecured, albeit only briefly

Thirdly, at 12.01am, Intralot was moved into an unrestricted subsidiary, using the reduced 65% interest in Topco and €202m of debt to reduce the FMV and,

Fourthly at 12.02am, a €202m lien was issued for the notes at Intralot Inc, stripping the previous credit backing used by the subsidiary for the 2024s.

We subsequently discovered another legal action, lodged by funds holding 2024 notes in early February for fraudulent conveyance and insider privilege. It is highly likely these two filings will be combined and the company side will seek to dismiss, said a source close to the situation. An exchange of letters is likely in the next three weeks, and a hearing likely in the early summer.

But as in all great stories, there is another late twist.

Just one business day from the court filing, the company announced a planned capital increase for up to 150% of paid up capital adding it had signed an MOU with “Standard General Master Fund II LP” a Delaware vehicle who will acquire non-exercised preemption rights.

Intralot will also enter into a share purchase agreement to purchase 33.32% of Intralot US Securities BV for $121.279m — the Topco which owns Intralot Inc the issuer of the restructured 2021s — of which 35% is owned by the exchanging former 2024 note holders.

We are still trying to establish the possible machinations and motivations of the latest moves and if they are connected to the litigation. Questions that immediately spring to mind are:

Could it build RP capacity? Perhaps to allow issuance to repay the outstanding 2024s?

Is it part of the rescission process, to unwind the former restructuring with more steps to come? (NB it does return 100% ownership of Intralot Inc, but it remains an unrestricted sub)

A spoiler to make it more complicated to unravel the prior restructuring?

A mechanism to cash out the 2024s, allowing them to crystallise value?

Provide valuation counterpoint for the FMV? (its close to FMV alleged in the August hearing)

Who exactly is SGMF? Are they a vehicle of an existing stakeholder, or a third party providing funding, and if so what are the motivations?

With more time to digest the 121-page report earlier this week we provided a summary of the key aspects and which areas might require further investigation.

The KPMG report expresses frustration in their inability to secure enough relevant information from Adler and in a timely manner. On multiple occasions, they say that specific allegations from Viceroy could not be refuted “on the basis of the documents submitted and the additional information provided.”

It is worth noting a number of documents were withheld due to legal privilege, which may suggest an ongoing or potential legal action. In total 3.1m emails and documents were disclosed with 800,000 held back.

We summarised the key takeaways with links to the pages in the KPMG report. Our aim is over time to explore some of these in more detail. Unfortunately, I may not have the time to spend months locked in a windowless room like the FT’s Dan McCrum did for Wirecard — for expediency extended bullets were the way forward.

Here are a few selected bullets (non-subscribers please DM for a full copy of our summary):

Cevdet Caner alleged exercise of control: Viceroy allegations can neither be verified nor refuted. Number of Adler RE transactions with Caner related parties were made without a selection process of a business partner and with limited documentation

Consultancy fees: Caner received €2m and €10.6m in fees [invoiced in March 2018 and September 2019 respectively]- despite no evidence of services provided or performance. Payments were made in instalments and in advance of deal completion. A €5.3m payment to a Turkish bank account in 2019 “did not go through”

Involvement in personnel decisions:Caner in several cases involved himself in personnel matters at Consus and Adler RE “and in some cases actively influenced decisions.”

Adler holds several positions in Aggregate bonds: As a related party from July 2020 to February 2022, Adler Group traded in several transactions. On 20 September 2021 they “significantly increased their share” in Aggregate Group’s 6.875% 2025 bond.

Gerresheim transaction:As a result of the special investigation, KPMG confirmed the sale of the project company was made indirectly to Caner’s brother-in-law. Whether he acted on behalf of Cevdet Caner “could neither be verified nor refuted.” The allegation that the sales price for the project company was excessive “cannot be refuted on the basis of the documents submitted and the additional information provided.”

ADO/Adler RE merger at inflated price: Caner received €10.6m consultancy fee (1.5%), despite legal firms and investment banks being engaged to provide advice. A full due diligence was not carried out. No valuation memoranda nor fairness opinions were submitted to KPMG. The redacted bank’s legal department “does not wish to issue any further documents regarding the fairness opinion dated 15 December 2019.” KPMG could not identify the beneficial owners in all cases

CG Grupe value inflation:Valuation of the group was significantly lower than in the prior close to its acquisition by Consus. Implied value of 60% over a finalised valuation. “The increase in value of 50% of the shares from €49m to €872m within one year - is not comprehensible.” [Bearer] bonds issued by Consus RE [as part payment] would not have been accepted on the market by reputable financial institutions. KPMG couldn’t verify whether Aggregate holds these bonds

KPMG Forensic estimates the development portfolio is worth 17.3% less than an external valuer. Correcting the fair value from the Gerresheim transaction and including other financial liabilities (and not including assets held for sale) Adler was in breach of its 60% LTV covenants in Q3 19.

Auditors KPMG (an unrelated department) are currently working on the production of FY 21 accounts due by 30 April. It will be interesting to see if it adopts any of the recommendations of its peers, and if it impairs its holdings of Aggregate bonds (now in the 40s).

Today Viceroy ramped up the pressure in their response to the forensic report saying “Without such [internal] controls, Viceroy do not believe it is possible that auditors can make reasonable assurances that Adler’s accounts are free from misstatements”. An update call for investors is scheduled for 3 May.

What we are reading this week

My US colleagues were all over Carvana this week, a deal for a loss-making US used car dealer owned by Apollo, which I would have love to have previewed. It seems to be betting the dealership on a huge acquisition. They even have a seven-storey car dispenser!

Our excellently written piece from William Hoffman is a must read, explaining the pros and (mostly) cons (we are not talking about the criminal record of founder Ernest Garcia) of the investment decision as the pricing pushed north of 10%.

Our colleagues at Petition as usual turned up the dial and with plenty of explosive emoji’s

But how could we avoid the story of the week, Elon Musk’s bid for Twitter, as journalists scratched around for his motivations. With so much copy, it was hard to find insight.

In my view, the best analysis and most thought provoking piece was from Ranjan Roy from Margins — titled Elon’s giant package (no he hasn’t seen him in the shower, it relates to his jumbo bonus from Tesla). Ranjan offers five theories.

Firstly Twitter is existential, Musk might have paid fines for his tweeting but it is essential to every element of his business and he must retain access

Secondly, it is a way to kill the SEC — to make sure his account not be limited nor banned.

Third, it’s the next package to get him to a trillion, Tesla is massively overvalued, he needs another vehicle

Fourth, the imagination deficit — robot taxis, cyber trucks, moonshots are looking tired, “Musk buying Twitter has generated the conversational energy that rockets and robots once did.”

Fifth and final theory, others are already selling Tesla — there will never be a confluence of factors to reward him as before — time to cash in, after all Tesla is up 1,700% from January 2018

Marina Hyde of the Guardian isn’t a financial journalist, but is the Twitter acquisition really about finance? Some great copy here:

“He’ll assume control of a platform where the people on the right are incredibly angry about free speech, and those on the left are incredibly angry about hate speech. Which is to say: they have so much in common.....People who seem to spend half their lives complaining about Twitter, on Twitter, seem stunned by the idea that a sh*tposter would ultimately buy it. Catch up! It doesn’t feel like a complete coincidence that all social media platforms are owned by men you’d run a mile from socially. Musk is one of them – a brilliant, horrid, ridiculous and very occasionally endearing grotesque. A sort of intergalactically successful Dominic Cummings. And yet, despite Elon’s give-a-toss gift for making himself what Twitter users might call the “main character” I cannot detest him entirely.”

Sometimes the headline and the first line are enough for you to click — Hertz faces new false arrest claim for cars reported as stolen — their CEO is vowing to eradicate instances where customers were arrested at gunpoint over erroneous reports that they stole cars they rented!

My colleagues at the FT have been all over Archageos’ Bill Hwang indictment. This will be our weekend reading — for those interested it is available in full here

For those lucky to be at Anfield on Wednesday — our Liverpool supporting CEO Steven Hunter wasn’t, btw he’s open to invites to the final — I hope you bought the programme, its a work of art (NB for non football fans, Villarreal are known as the yellow submarines)