This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Friday Workout — Put into Deep Freeze; Property is Heft

Chris Haffenden

•19 min read

Post the publication of last Friday’s Workout, Jerome Powell’s Jackson Hole comments confirmed our suspicions, we’ve had the inflection point, credit spreads are going wider, and rates will be higher for longer. Inflation remains rampant in Europe, with GS talking about it peaking at 22% in the UK, and with Eurozone CPI closing in on double digits. On a more positive note, power and natural gas prices stopped going parabolic and reversed most of last week’s gains. But the effects of the energy crisis are with us already, and even the most ardent conservatives losing Truss in the governments’ ability to cushion the pain.

It is starting to get serious, it is not Chicken Feed. Our electricity direct debits are already soaring and there is talk that whole swathes of pubs could go under due to quadrupling energy bills (even more reason for 9finest to visit the Wenlock Arms). Beer supplies could also be affected by lack of Co2 with CF Industries last week saying last week it will halt production and Yara, the largest ammonia producer in Europe, saying they are reducing to just 35% of capacity. The only positive I can see is that publicans might have to switch more keg lines to cask.

Calls for the government to freeze energy prices are getting louder, with hope for more fizz from Liz when she stops trying to win the votes of disgusted from Tunbridge Wells pensioners. There is talk that the Treasury is working on a government backed lending scheme for energy suppliers which could lead to a freezing of energy bills.

But as Deutsche analysts post in a recent note, the costs of doing so are high, the limited version would cost £12bn (for £400 per household), rising to over £50bn if a full price freeze came into effect from January, and £30bn if it came in April. While expensive, there are benefits too as it would reduce headline CPI and reduce the risk of an inflationary spiral while saving around £10bn in interest costs (UK heavy issuance of index-linkers is not looking so smart now btw).

None’s gone to Iceland, earnings are best served cold

Sticking with deep freezes, it’s worth remembering that significant energy using businesses such as Iceland Foods will not benefit from the Government’s plan.

Iceland might be the first company to coin the term EBITDAE – no, not earnings before everything, even it that seems so for many LevFin companies – but earnings before exceptional energy costs. In their frosty Q2 22 release yesterday, EBITDA margins fell to a measly 2% with their P&L unlikely to defrost any time soon.

Malcolm Walker is an entrepreneur to his fingertips. Born in Yorkshire in 1946, his first venture was as a dance promoter while he was still at grammar school. Leaving without conspicuous academic qualifications, he immediately identified retailing as the way to make his fortune and began work as a trainee manager at Woolworths. Iceland was founded as a side-line in 1970 with a single small shop in Oswestry selling loose frozen food, and a starting capital of just £30.

Malcolm has only ever had three paid jobs, and so far, he’s been fired from two of them. Discovery of his extracurricular interest in frozen food prompted his dismissal by Woolworths in 1971, but luckily this provided the catalyst for a rapid expansion of Iceland into a national chain.

The loss of Woolie’s pick n’mix is surely outweighed by Iceland’s Skittles crazy sour-flavoured Ice Cream - some aficionados think these are pickle flavoured – do they taste better than they look?

Apologies for going all tangential so early on in the Workout.

Lets get back to the frozen food retailers’ ice rage, as 9fin’s Ben Hoskin and Laura Thompson reported:

“Iceland revealed the extent of its own energy crisis today, with EBITDA of £16.9m in Q1 23 (end June) drubbed by £19m of unhedged exposure to surging electricity prices - excluding the energy hit EBITDA would have come in at £35.9m…Management didn’t dress up the energy impact. The government needs to step in and help, otherwise suppliers will struggle, and the company would need to reassess its store openings across the UK.”

It gets worse, as the first quarter could just be the tip of the iceberg, as investors were told there is only a “small portion” of energy hedged for the rest of the year, with the next four-to-six weeks fully bought. Beyond that, the company is very much at the mercy of markets. Management said they are working on a long term fix and are “in discussions with five or six organisations”, but any solution wouldn’t come into effect until at least the next calendar year.

But ‘money doesn’t grow on freeze’ and delayed payment terms have yet to impact cash flows, which are likely to melt away in the next quarter. Luckily, the block of cash is decent at £162.6m.

Investors would like management to use some of their frozen dough to buy back their bonds at a discount (the 25s are in the mid 70s, 28s in the mid 60s), but little has been purchased so far.

With leverage rising by half a turn to 5.3x and just 18-months before the 2025 bonds go current the path to deleveraging looks tough and interest cover is a mere 1x. This name could be another one for our watchlist (more on that next week).

Property is Heft

It’s been too long since the Workout has taken a look at German Real Estate, so this week we have a bumper edition of not just one, but three issuers. Two are deeply connected, while the third claims it’s very different, but its bonds are also trading at distressed levels, which shows how badly the sector is perceived by investors – for whom German property is heft.

Adler Group’s releases certainly stretch the boundaries of credulity.

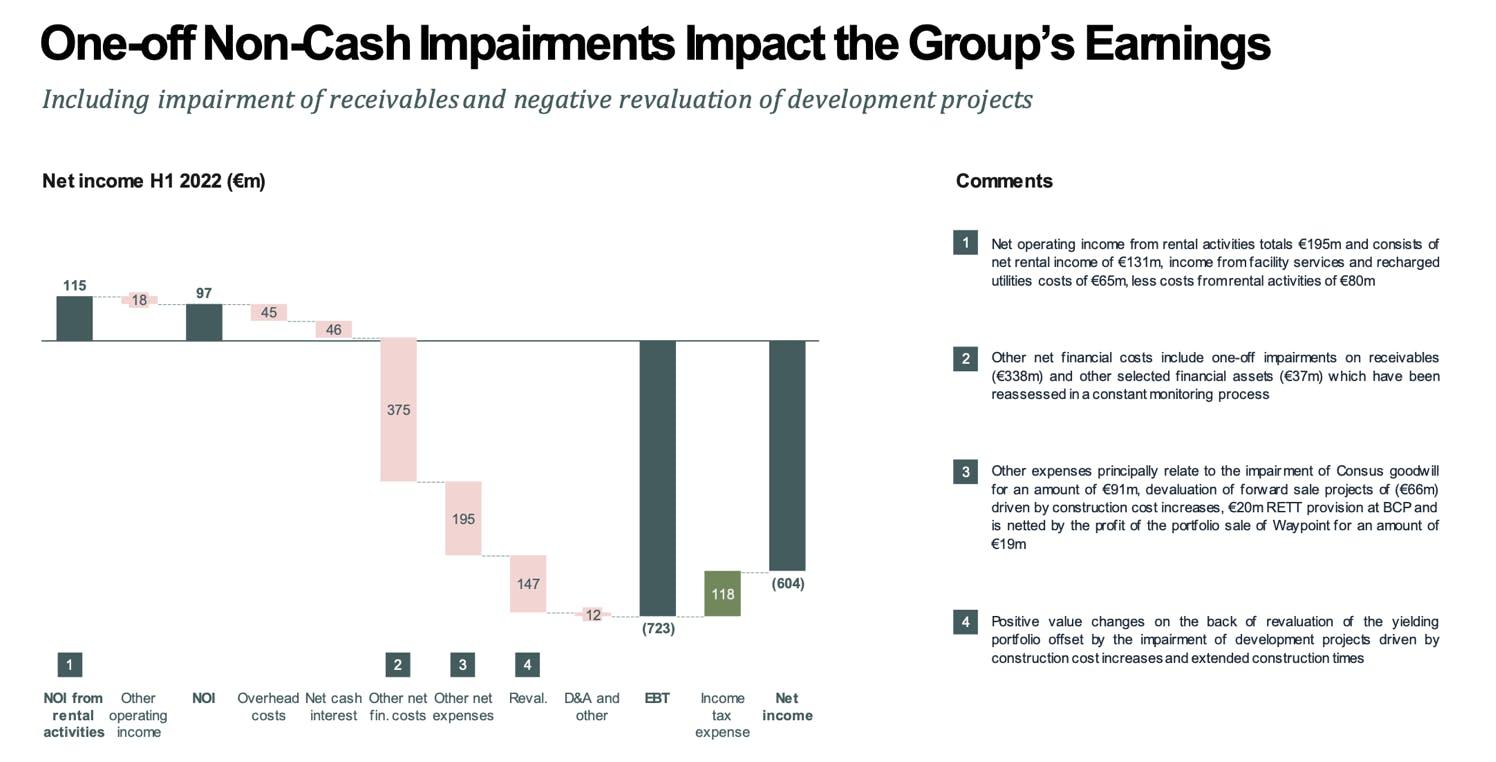

I’m not sure how they can say that their H1 performance has been robust. They posted a €604.4m loss after finally impairing the value of their development projects and receivables. The LTV rose from 52% to 58% during the past quarter.

If that wasn’t bad enough it faces ongoing BaFin and Luxembourg regulator investigations, with no applicants for the vacant auditor position and is reliant on rolling waivers from lenders LBBW and Commerzbank over the lack of consolidated accounts, to avoid termination of their loans.

As least they have found a CFO. In the end they decided to go with the interim CFO rather than the four ‘highly qualified’ candidates on their shortlist. We learned that White & Case is going through KPMG’s forensic report, being peer reviewed by Linklaters. PwC has almost finished their compliance report, whose results Chairman Stefan Kirsten said are ‘quite positive.’

But while Adler tries to convince investors it’s got its act together, it needs to raise cash and fast.

As reported, with LEG Immoblien deciding against exercising its option to buy the 74% of Brack Capital Partners it doesn’t already own, if it doesn’t find an alternative buyer Adler could struggle to meet its 2023 maturities of just over €1bn.

Adler admits (on Page 15) of its Q2 22 release that “the liquidity position for 2023 depends on the successful closing of up-front sales.” It adds that “due to the [debt incurrence] covenants falling below the thresholds no additional third party debt financing can be obtained without needing to procure waivers or consents of applicable creditors.”

Over the past year, Adler Group has sold a number of residential portfolios to raise cash, most notably two transactions with LEG and KKR for a cumulative value of €2.485bn. It has a number of development projects for sale with €438m (Gross Asset Value) of projects which it says have offers, letters-of-intent, or are in exclusivity. But under questioning management declined to give further details, save confirming that two projects which were communicated as sold in Q2 (from Q1 report) were back on the market – after the sales “were cancelled.”

In its Q2 22 release, Adler Group said: “Among other things, the management board is to be authorised to sell up to 22,301 apartments and commercial units from ADLER's portfolio. This authorisation is to be valid until the next annual General Meeting. Moreover, upfront sales of [its troubled subsidiary] Consus Real Estate AG, which are not classified as “build-to-hold”, are potential options, even if the sales price is below book value.”

NB Adler Group has 26,243 residential units as of Q2 22, many sit in its yielding portfolio. Effectively all of Adler’s assets are on the block, leading us to say – is Adler effectively in run-off?

The reason for the latest pivot is unclear, and Adler Group declined to comment when asked by 9fin. We can only speculate that it may be to provide further flexibility to make other sales to meet maturities if the planned BCP and development portfolio sales fail to materialise.

Notably, BCP sale proceeds are not included in the liquidity forecast for year-end, despite Adler saying they are confident of finding a solution within a reasonable period of time.

Adler is also seeking to squeeze out the remaining minorities at Adler Real Estate (it holds 96.7%), making it easier to consolidate the business and move cash around the group. But 9fin understands most of these shares are now owned by the K&E-represented Adler Real bondholder group, who previously warned the parent about intercompany loans and property sales which they view as leakage of value away from the bonds.

“Another area the shareholders request transparency on is the Company’s apparent strategy to address its maturities by selling up to nearly 95% of the Company’s residential and commercial units, as proposed by the 31 August agenda. Given that such transaction is not permitted under the terms and conditions of the Company’s outstanding corporate bonds, the Minority Shareholders demand to know how the Company intends to navigate these limitations and how it intends to use the proceeds from potential such asset sales.”

Adler says it is having active discussions with two bondholder groups.

But most of the ‘constructive dialogue’ appears to be with a larger Hengeler Mueller-advised cross-holding group representing over €3bn of bonds, which the company first spoke to in July and is meeting with in London next week.

The relationship with the K&E group didn’t start as well, with little responses to their initial written missives, which Chairman Stefan Kirsten put down on the earnings call as ‘misunderstandings and communication problems.’ They are due to meet in mid-September, he said.

The plot thickens

Last week, we gave a teaser on Accentro, formerly owned by Adler – now to detail the plot twist.

To recap, the German-real estate group has €250m of bonds due in February 2023. Recent performance looks decent on first blush with significant amounts of cash and cash equivalents (€158.9m). Elsewhere in the debt structure are €100m of private placement notes due in 2026, which should leave plenty of room for an A&E, if you decide to use some of the cash to sweeten the deal.

Houlihan Lokey and Milbank were appointed by a group of bondholders in the group’s 2023 notes in July. The company is working with Perella Weinberg and Latham & Watkins. Sources close to the situation are keen to suggest that an A&E with some cash payment and further funds from future assets sales should suffice.

But the bonds are in the mid-50s. Surely, they should be much higher, trading at least in the high 80’s if the solution is that simple – what’s the catch?

Is it concerns over the Azeri ownership of Accentro and their alleged connections to former owner Adler, or as short-seller Viceroy suggests, to our old friend Cevdet Caner?

Not quite. Let’s start by going back to the original transaction.

Accentro was formerly a subsidiary of Adler RE, until it was sold to Brookline Real Estate (RE) in 2017, who now holds an 83.1% stake. Brookline RE is advised by Vestigo Capital, led by Azeri investor Natig Ganiyer.

The sale of the 80% stake was for €181m, however only 20% was paid upfront, according to Adler RE’s 2017 report. The rest was booked as a receivable, with speculation that Adler had lent the money for the purchase.

After KPMG Forensic reviewed Adler’s accounts earlier this year, Adler admitted there was a risk it might not recover the amount still owed by Ganiyev, according to press reports.

An interim payment of €97.9m was made in 2019 following an extended payment term. Management further extended until 30 September 2021 but still no payment was made. In the fourth quarter of 2021 just €3.3m was received.

The KPMG Forensic report states that representatives of Adler RE had justified the granted postponed payments saying that in the event of a repatriation of shares in Accentro RE, Adler RE would have been under an obligation to submit a binding takeover bid. The transaction was carried out to stabilise or improve external ratings, which means the reversal of the transaction would have been contrary to strategic interests, they added.

According to Adler RE’s Q1 2022 report the purchase price receivable including interest from the sale of Accentro amounted to €59.3m, up from €59.1m in the previous year.

Adler now has a share pledge over the Accentro stake, and with the receivable due in May 2022, we were eagerly awaiting Adler’s Q2 report release to see if they would finally accelerate – after all as we’ve outlined above Adler is desperate for assets to sell.

But the shares might not just be pledged to Adler, as according to a filing in the Luxembourg companies register Brookline RE SARL also took out a €100m loan from a South Korean Bank called Nonghyup in July 2020, due to mature in July 2022. It is unclear as to whether this has been repaid or extended. As Brookline’s stake in Accentro is its largest asset, it may have pledged its shares against this loan too, a source familiar with the situation suggested.

Long suffering Adler watchers would not be surprised that in the Q2 22 report it was disclosed that the receivable maturity was further extended to 30 September 2022. But the report also mentions that the controlling shareholder (Brookline SARL) of Accentro RE is in financial restructuring and Adler part impaired the receivable by €37m.

Contrary to its troubled peers, who have turned more cautious, SIGNA Development remains upbeat on prospects for the German real estate market.

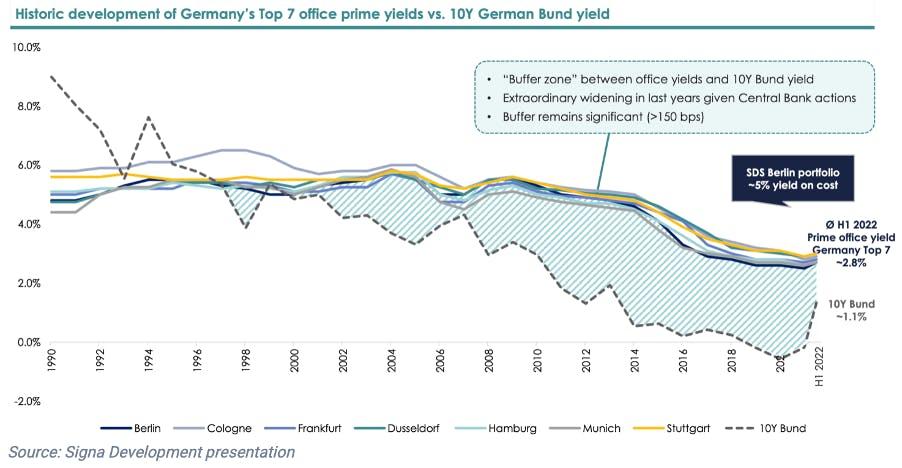

Management says that investment markets remain liquid, and yields remain stable. They cite Berlin rents rising over 8% in the past year, with near record levels of take-up for commercial offices, and added that most of Signa’s residential exposure is in higher yielding Austrian and Italian markets.

Signa management also dismissed concerns that rising interest rates would impact property yields and as a result lower asset prices saying there would be further rental growth if inflation persists. They cite the huge buffer zone between office and 10-year Bund yields in the slide below (NB the last time 10-year Bund yields were above 1%, prime office yields were nearer 5%)

As reported, over the past year, SIGNA management have spent a lot of time trying to convince investors that it should be viewed differently from Adler Group, Aggregate and Corestate, which trade at distressed levels. In previous earnings calls it took a sideswipe at its tainted peers saying it does not include receivables and net financial assets in its LTV calculations.

The German developer’s strategy is to forward sell at least 50% to property investors prior to project completion. Despite not receiving the sale funds until completion it books the revenues in its accounts using aggressive percentage of completion accounting treatment. This boosts EBITDA and reduces LTVs by increasing Gross Development Values.

As such these percentage of completion adjustments make up the largest component of group EBITDA, as we outlined last December. The group also uses fair value adjustments to boost reported numbers. Determining these adjustments is based on a number of factors, including future rental income, vacancy rate estimates, cap rates, average market rents, rentable areas, vacant space, and weighted average lease terms.

Signa says that forward sale volumes are €700m as of 30 June. It projects excess cash flow of around €800m over the next two years.

Aside from its €300m 5.5% green high yield bond, Signa Development also uses profit participation certificates and project finance debt to fund its development projects. Management said they have learned from the 2010 (sic) crisis to diversify their funding sources.

Profit participation certificates (PPCs) are subordinated to other debt and mature two years after the estimated project completion date. Interest is only paid out subject to profitability, and non-payment doesn’t trigger an event of default. PPCs issued at the project level are repaid around five months after a project has been sold or refinanced. Note ratings agencies treat these subordinated certificates as debt. However, Signa does not include them in LTV calculations.

In the first half, the company repaid most of its project debt, with just €400m remaining.

The equity capital markets also remain open. Unlike its peers, it has been successful at raising additional equity capital from institutional investors, and remarkably at Net Asset Value for the latest €200m fund raising (good quality listed peers trade at a 20-30% discount to NAV).

On their earnings call management said €500m of financing is needed to fund the business in the next two years. With a ‘very flexible’ funding structure, management said they were not concerned about their ability to raise the funds, and hinted this would be raised nearer to 2024.

Project debt is also attractive. German and Austrian banks were prepared to lend on a senior secured basis at margins of around 250 bps, with the average rate on the remaining project debt a mere 2%, they boasted.

Taking all this at face value, the bonds are a significant outlier. Why should they trade at 15%, which is almost twice the yield on offer to the PPCs which sit below in the capital structure? And despite a healthy €250m of cash on the balance sheet and claims of significantly cheaper and readily available funding sources, just €10m of the bonds have been bought at a discount so far.

Admittedly, we don’t know about its ability to issue fresh PPCs – the latest batch were recently extended by one year, or project debt – in light of the re-rating of the German RE market.

Is this just Signa versus noise from its German peers, or is something else afoot? There is a significant development pipeline much of which is not yet beyond the planning stage, after all.

Yesterday, we released the latest edition of our Top of the Flops report - for end August 2022.

Jerome Powell’s Jackson Hole comments last Friday and sharp rises in European gas and power prices over the past fortnight may have punctured the late summer price bubble and possibly dashed hopes of a resurgence in European LevFin activity in September. But the puncture could be a slow one. Despite a sharp increase in Government bond yields and widening of headline indices, the effect on cash bond spreads and loan prices has been muted.

To see the changes in numbers of bonds and loans in our stressed/distressed universe, plus new entrants and biggest movers click here.

Frigoglass negotiations with bondholders thaw

Fridge and glass manufacturer Frigoglass postponed the release of its Q2 earnings to later this month as it finalises debt discussions with holders of its €260m 6.875% 2025 senior secured notes. A committee of four noteholders, with around 60% of the outstanding notes, has been in negotiations with the company over the last month and are restricted from trading.

Committee members are expected to be cleansed some time in September, as the group should provide an update on the restructuring towards the end of the month, both sources told 9fin’s Bianca Boorer. The restructuring plan is still being discussed and may involve a debt extension or something more “severe”, the source close to the creditors said.

Head Windy Miller

While working capital is being hammered as wage inflation and cost increases hit, Stewart Lynes, group CEO of Miller Homes took pains to show the company was taking a measured approach on its Q2 earnings call. The UK-based house builder, bought by Apollo last year, is focusing on affordable housing and maintaining strong liquidity in face of serious macro pressures.

Management is considering what to do with its significant cash position – even though at £121.3m as of June 2022, it is almost half the size that it was a year earlier (£227m). Potential options include additional land purchases, bond redemptions, shareholder distributions or SSN purchases, according to the company’s quarterly presentation to 30 June 2022. Bondholder concerns seem limited, as was made clear during the Q&A session: No one asked any questions. Their SSNs did re-enter our stressed universe, however, yielding more than 11%.

Can Victoria make preferred equity redemptions ahead of the bonds?

9fin’s Denitsa Stoyanova outlined in her Q2 updateVictoria Plc’s true leverage looks very different from the 2.7x leverage figure reported in the consolidated financial statements. In a follow-up report, our legal team considers how leverage and EBITDA are calculated for purposes of the covenants for Victoria’s outstanding high yield bonds. This is especially relevant given that Victoria’s management have indicated that they are actively considering share buybacks and that they intend to fully redeem the £225m preferred equity issued to Koch Equity Development with cash prior to their conversion to ordinary shares, we also review Victoria’s capacity to send value out of the group to shareholders under the bond covenants.

KP is open to bond buybacks, but are these just peanuts?

Kloeckner Pentaplast management didn’t rule out the possibility of buying back its discounted debt in the secondary market on Wednesday’s (31 August) Q2 earnings call. Sequential margins were flat for the German plastic packaging firm, with cost inflation still being offset by pricing actions. The company burnt €50m of cash in the first half despite a €35m draw on the RCF, with net leverage ticking up to 9x on an IFRS 16 basis.

As 9fin’s Ben Hoskin says: “Performance has been okay but questions remain over whether the company can deleverage enough to cover the SUNs. The debt was issued in February 2021 on a well documented and heavily inflated EBITDA figure of €305.5m, which compares to a Jun-22 LTM figure of €234.4m. EBITDA guidance for FY 22 was “confirmed” at the lower end of a previously wider range, but now expected at €265-275m (versus €265-285m previously).”

Codere plays the long game

Spanish gaming company Codere reported strong Q2 results on 1 September, writes 9fin’s Lara Gibson. Revenues and EBITDA rose strongly year-on-year largely driven by a post Covid gaming boom and strong growth in Latin America. But investors are concerned if can maintain margins amid an economic slowdown and question if it should dial-back its aggressive expansion plans.

What we are reading/listening too this week

The list is a little smaller this week, as I was bogged down with earnings presentations and calls, and a raft of edits (our journalists are too productive – we still have a role open for an editor btw).

I’ve somehow missed the whole concept of Quiet Quitting which apparently went viral over the past few weeks. The WSJ decides to cover it from both sides, first stoking the outrage, then covering the consequent outrage – thanks to Will Caiger-Smith for spotting this one.

“The U.S. stock market remains very expensive and an increase in inflation like the one this year has always hurt multiples, although more slowly than normal this time. But now the fundamentals have also started to deteriorate enormously and surprisingly: between COVID in China, war in Europe, food and energy crises, record fiscal tightening, and more, the outlook is far grimmer than could have been foreseen in January. Longer term, a broad and permanent food and resource shortage is threatening, all made worse by accelerating climate damage.The current superbubble features an unprecedentedly dangerous mix of cross-asset overvaluation (with bonds, housing, and stocks all critically overpriced and now rapidly losing momentum), commodity shock, and Fed hawkishness. Each cycle is different and unique – but every historical parallel suggests that the worst is yet to come.”

Wowsa, even this perm-bear, needs some lighter relief, after that.

Brighton and Hove Albion continue to provide pain and delight in equal measure. Potterball is delivering results despite the cheapest starting 11 in the Premier League, and for five minutes last Saturday, we could sing “we are top of the league” before Man City turned their match around.

We could have been top for at least 24 hours if we had beaten Fulham on Tuesday, but lost 2-1. I suspect our usual struggles against lowly teams may repeat at home to Leicester on Sunday.

As someone once said, it’s not the despair, I can deal with that, it’s the hope.