This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Friday Workout — Reverse Currency; View from the Top of Gherkin

Chris Haffenden

•14 min read

One of the fundamental mistakes of trading and investing is to try and pick turning points and misinterpret data to fit into your new narrative. The trend is your friend is one of the biggest trading truisms. But human nature is your biggest enemy, evidenced once again this week as US CPI numbers crashed the recent dash for trash narrative. US equity markets ended up with their worse day since June 2020 and the charts on a technical basis look awful.

As analysts from Oanda wrote this week: “There appears to have been a tendency in recent months to front-run certain releases in the hope that it’s going to prove to be the “pivot” moment when everything starts to look-up, central banks can ease of the brake and risk assets will have bottomed.”

The effect on rate expectations didn’t take long to filter through, with futures now pricing over a 30% chance that the Fed will hike by 100 bps at their upcoming meeting. It couldn’t have come at the worst time with the jumbo Citrix US HY deal just launched and signs of a tentative reopening in Europe. (The docs on that deal are a new low btw – and 9fin was first to highlight the absurd RP capacity builder).

While there is undoubtedly some pent up demand boosting appetite for reopening, it is becoming glaringly apparent just how expensive it will be for borrowers to come to market. Lottomatica, the first EHY deal to come in September priced its latest euro offering at 9.75%, a huge 175 bps premium to existing paper, according to one buysider. It was a decent credit to restart, the Italian gaming business has performed well since last year’s print, alleviating some concerns about add-backs. Sponsor Apollo has two acquisitions lined up (allegedly at 11x EV/EBITDA) which may have contributed to their timing to come to market. This deal is further evidence the days of using cheap funding to drive value are over.

Reverse Currency

Rising rates and hikes in risk premia are one worry for sponsors and company CFO’s, another less publicised concern is FX strains, as stress in the financial system are showing up in currencies. Not only could this affect their competitiveness, but it also exposes any funding and cost mismatches.

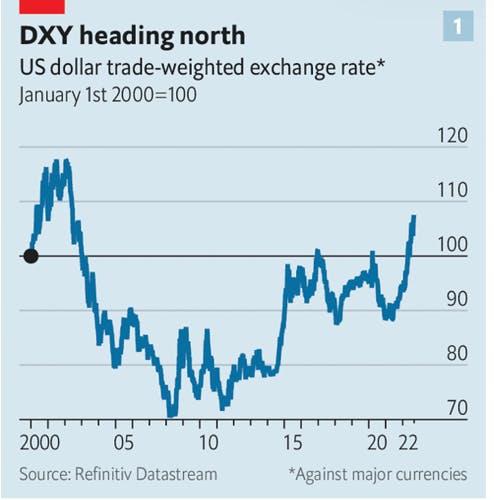

Much has been written about the strength in the dollar (up 20% in the past year) and the damage it is inflicting on Emerging Market Sovereigns and corporates. As the Man Institute outlined in their recent report EM distressed is now 80% of the total up from 10% at the time of the GFC. Since the end of 2019, hard currency EM Sovereign debt trading at distressed prices (over 1000 bps) has more than tripled, while distressed EM Corporate debt has expanded by 2.5x.

Investors are fleeing in their droves – around $20bn of outflows year-to-date from EM corporates. For context, the amount of external EM HY bonds is $1.8bn (approx. 50:50 sov/corps) compared to around $775bn for European LevFin.

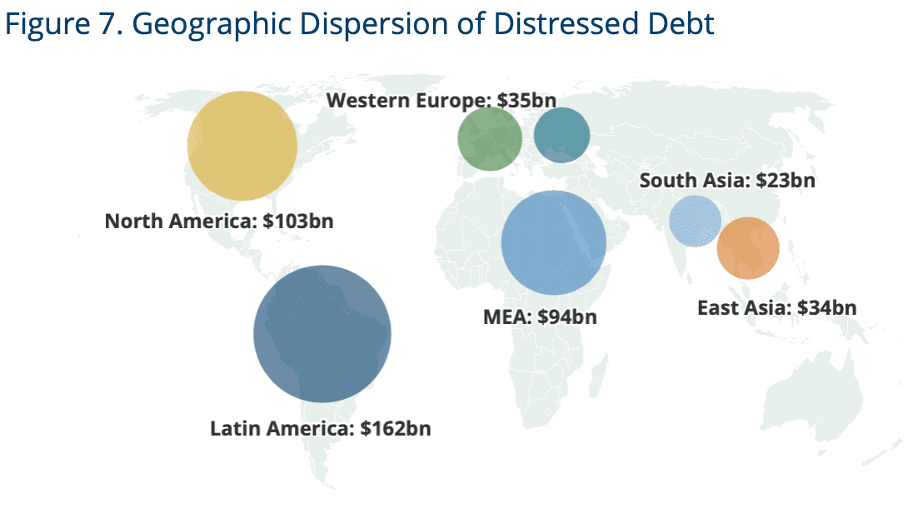

The size and geographic spread of the problem is highlighted below – yes, Latam distressed debt is bigger than US!

Source: Man Institute

While EM is not really the preserve of 9fin coverage, there is some overlap, most notably Turkey, which is a significant trading partner of Europe with $35bn of corporate Eurobonds (many held by HY investors).

Turkey is avoiding default by doing swaps with local bank’s foreign currency assets, otherwise its international reserves would be negative $64bn, notes Fitch. It is so desperate for foreign currency reserves, that it is happy to take inflows that it can’t account for – an incredible $24.4bn YTD – which Tim Ash from Bluebay suggests could be down to Russia oligarchs moving assets and could show the true extent of Russian capital flight since the conflict began.

So why is the dollar so strong?

I part agree with the Economist that it is a refuge in troubled times with Europe seen in a much worse position due to the energy crisis (and the UK even worse) and by differences in monetary policy (the US is seen as a high yielding currency with the ECB much less aggressive).

But surely a strong dollar is a good thing for European producers, as it gives their exporters a competitive edge?

In reality, it is not so simple, energy disruptions are hampering their ability to take advantage, and worst-still most commodities are priced in dollars, so while these costs may have eased of late, in euro terms the benefit is much less.

After years of no-one caring about currencies, we could soon see mass interventions.

The Japanese Central Bank (big holder of US Treasuries btw) is already talking about holding the line at 145, and China is also under pressure to do the same at 7.

Jon Tuerek of JST Advisors recently cautioned about a dollar doom loop as dollar appreciation slows global growth, leading to more investors heading to it for perceived safety. Trying to break the dollar dominance is a frequent theme – with China promoting its digital currency for trading partners. China, India, and some desperate European buyers now paying in Rubles for their Russian oil and gas. Non-dollar usage is set to soar, and we can’t rule out China and Japan selling out of their big holdings in Treasuries.

Could as Zoltan Poznar suggests, we see the dollar lose its reserve currency status? If it did it would ease pressure on the Eurozone, as otherwise the ECB may have to tighten even harder than it would like to avoid further drops in the Euro. There is a fascinating discussion this week on Bloomberg’s Odd Lots podcast about this with Zoltan and one of his former collaborators.

So, when will the dollar stop being a reserve currency and reverse?

I’m a credit and restructuring guy, not an economist, so will recuse myself. But I can’t help feeling that FX may overtake rates as the top story in coming months.

View from the top of the Gherkin

This week after a three-year Covid-related absence, we returned to the Gherkin for Kirkland & Ellis’ restructuring cocktail reception at the top of the iconic building. Memories of interesting conversations in dark corners with advisors and funds while at the same time trying to avoid other journalists overhearing and stealing potential scoops, came flooding back. It was refreshing to see how many old faces were still there and apologies to anyone I missed at the great event.

This year we were also treated to a presentation from K&E lawyers on the market outlook for the various regions, recent deal flow and some new restructuring techniques.

The highlights included insights on the difficulties on handling Crypto insolvencies – incredibly many Celsius users signed over their holdings when they adopted the platform (this brings back painful memories of re-hypothecation in Lehman) – and disclosure, the judges want to know who the creditors are, but if you identify holders, it makes their wallets vulnerable to hackers!

The main topic of conversation as we moved upstairs for drinks, however, was up-tiering transactions coming to Europe. These were euphemistically called ‘liability management’ by their lawyers — we think ‘creditor-on-creditor violence’ is more apt. The room was evenly split whether it could happen over here.

Regular readers may remember Envision, and our musing on Intralot, arguably the first European example of being J.Screwed. The Greek gaming company was however, admittedly, seen as an outlier as it wasn’t a sponsor deal. Coincidently, Max Frumes from LevFin insights last week wrote a great summary of the Envision deal and the evolution of the tactic from PetSmart, Chewy, Revlon, J.Crew, and Incora in a LinkedIn post which is a great starting point to get up to speed.

In short, in Envision, some of the first lien after creative use of loose docs by some their fellow creditors and with assistance from the sponsor, eventually ended up as fourth lien. Max goes into great detail on how lenders were picked off and played off against each other and how the series of transactions were structured that led those from going first to fourth.

Our Gherkin hosts were the common denominator in the Envision and Intralot transactions. They are known as one of the most innovative and daring of restructuring advisors. I admit there may be an element of talking their book in the presentation. But openly stating that they are working with distressed funds who are actively talking to sponsors regarding stressed portfolio companies using loose docs to put in place priming financing certainly raised eyebrows in the room. It also appears in their recent literature under the Out-of-Court Solutions section.

The above might come as a shock to some of us in Europe.

The ad hoc committee often grabs the bulk of the fees and can get slightly better economics if they backstop rescue funding under an agreed restructuring plan. The offer to participate in the new money and headline terms are 99% of the time made available to the rest of the same class of creditors. They are not pitched against each other and don’t suffer widely diverging outcomes, that just isn’t the way its done over here.

Discussing above with a sample of fund managers and advisors over a glass or two of champers (the food was great btw), there was a sharp divergence of opinion of whether it could happen over here. After all the relationships between sponsors and investors are much more closely intertwined, as many sponsors have their own vehicles and/or are invested in CLOs and private credit funds. Surely, this would mean J’Screwing themselves. The question of reputation also came up. Being the first to make the move in Europe may be difficult, it’s so much easier to be second or even better third, when it becomes a trend and more friendly.

But the counterpoint is that if you have hundreds of millions (if not billions in the case of Upfield Flora) at stake, the LPs in your funds are likely to be much less concerned about reputation.

In the US, we’ve seen a few of these aggressive moves partly overturned after litigation, allowing disgruntled creditors to move up a lien or two. Over here, most of these deals will be done via exchanges and a series of transactions. The reason is that it is unlikely that Schemes or UK Restructuring Plans will be sanctioned by judges if the classes are fractured in two, as the concept of fairness and equitable treatment would invariably come into play.

As an interesting footnote, 9fin’s Owen Sanderson notes in this week’s Excess Spread CLOs are tweaking their documentation to allow themselves to participate in Asset Drop Down Transactions (J.Screwed’s) — perhaps the distressed funds won’t have it all their own way after all.

Standard Deviation

Another topic of conversation was the resilience (or lack of) for borrowers to deal with a sharp increase in interest costs when they eventually come back to market refinance. Many companies in our LevFin universe produce very limited operating cash flow, and the pace of deleveraging — in many cases interrupted by Covid and input cost rises — has been limited since issue.

While the bulk of the maturity wall is now in 2025 and 2026, this is not as far off as you think, noted one distressed analyst. Ideally you will want to deal with maturities at least a couple of years earlier. This could lead to a wave of companies having to come to market in the first half of 2023, and forced to take whatever price they can, he suggested.

I would add that buyers are likely to be more discerning than at the 2021 peak. Some sectors and credits are clearly not suitable for High Yield, as either they shouldn’t carry as much leverage and/or their businesses activity are too volatile. Retail names such as Matalan and Takko spring to mind, as does Raffinerie Heide, despite the recent once-in-lifetime quarter bailing them out, it should never have gone to HY, and shouldn't have been refi’d with yet more HY either.

Matalan isn’t a terrible business, but it is not a growth, roll-up, or transformation story. EBITDA has never really grown much above £100m. It would have been much better off using non-cash flow based borrowing such as ABL and receivables facilities. Having first and second lien bonds makes no sense, and as the Hargreaves family are finding out, the price to get acceptance to extend is much higher in 2022, reportedly as much as £100m, whereas last year stressed companies could get away with a mild coupon bump and not having to stump up cash.

Secondary prices in 2022 are not giving borrowers with a troubled history the benefit of the doubt, Ideal Standard and Tullow Oil being great examples.

The former has its July 2026 SSNs trading in the high 50s and yielding almost 23%. The Belgian manufacturer of bathroom products had a poor second quarter but reported leverage (note there are a lot of adjustments, including arrghh yet more restructuring costs) is only up by half a turn since launch to 4.3x. Cash flow from operating activities for the six-months to June 2022 was negative €40.3m after €42m of provisions, leading to its cash position falling to €47.7m from €89.4m. Cost of sales rose by 12%, with revenues up just 5.2%. Adjusted EBITDA for H1 22 was €38.7m (but included a €12.1m increase in restructuring costs) compared to €51.3m a year earlier.

But while this calculation is fairly standard, there is a deviation for Ideal Standard reporting as they continue to add in €14.2m of pro forma add backs to get to an LTM figure of €93.3m and a much healthier 12.7% margin.

Unfortunately, there is little else to glean as the MD&A doesn’t appear to contain much discussion and analysis and worse still it is another borrower that doesn’t allow non-bondholders on its calls. We would love to know from bondholders if they want to keep their Sanityware product or want to flush it out of their books.

On the face of it, Tullow Oil should be riding high and in a position to refinance at the end of this year, whether or not it completes its planned takeover of Capricorn Energy. Debt to EBITDAX should drop to near 1x, and if oil prices average $100/bbl it could generate another $1bn of FCF by 2025. There is potential upside from projects in Kenya (farm down expected by year-end) and production to come on stream in Ivory Coast and potential gas commercialisation from its Ghanaian fields.

The presentation was impressive but didn’t include any figs from the merger and the CEO was non-committal if they would increase their bid amid increased Capricorn shareholder disquiet.

Tullow Oil completed an expensive refi of its reserve-based lending facility last summer with a jumbo $1.8bn 10.25% SSN, leaving its 2025 SUNs in place and ahead in the maturity queue. It has failed to gain maximum value from the surge in oil prices as the HY bond kept the conservative hedging strategy demanded by its old commercial lenders in place. This and an investment programme to arrest the decline in output in its Ghana fields (and to drill for more) has led to negative cash flow in the first half and this metric will only hit $200m for the full year. But management said it is seeking to change their hedging strategy in 2023.

The 2026 SSNs are trading with a 93-handle. An early 2023 refi gives you seven points of upside in just 4-5 months and if they don’t there is an amortisation boost ($100m) each year. The 2025 SUNs are back down to the high 70s (they jumped into the low 90s on the Capricorn announcement) yielding 18.5%. That’s a healthy discount to put on a trade around the M&A.

Watching the Defectives

This week our friends at the pink ‘un, published their debt monsters in the downturn. We are not sure how much credit analysis went into the list – derived from ICE pricing at over 1000 bps spread to worst – but it was refreshing to see that they have abandoned price as an indicator of stress.

Coincidentally, later the same morning, as promised we detailed our own watchlist – with the working title – Watching the Defectives, but unlike the FT we showed our reasoning.

9fin’s approach is similar to our advisor and distressed funds clients. Firstly, we use 9fin’s extensive screeners to develop a long list. This is the first stage in seeking out potential mandates and investment opportunities.

Price is too blunt an instrument to identify stress/distress. To illustrate, over half the issuers in 9fin’s LevFin coverage have debt prices below 90, the traditional indicator of stress. Many debt instruments are down sharply in price due to duration and convexity in a rising rate environment, but many are showing little signs of stress from a credit perspective.

To strip out some of the noise we use spread to worst as our starting point. We can then use other metrics such as leverage, upcoming maturities, liquidity runway and interest cover to refine our searches. This reduces the number of names, and seeks to establish which deals might struggle to refinance, and those which might experience liquidity issues, etc.

Our Top of the Flops report is a good way to track new entrants into stressed and distressed.

It is not just the use of absolute figures and metrics; their trends and speed of development are at least as important. Our real time price data allows you to spot the biggest movers and then dig further into the financials, deal docs, news, and assess legal considerations.

In addition to quantitative factors, we also use qualitative information – such as early warning signs of potential candidates from our reporters’ sources, especially for loan names where up-to-date financials are less publicly available.

Upcoming triggers are another important factor in our decision making – is there anything likely to trigger stress in the next 6-12 months?

From all the above, we compile a manageable watchlist of 20-25 names, from an initial list of 250 plus bonds/loans.

Our initial 24 names and a few more up for consideration were detailed here for subscribers. We will provide regular updates of new entrants, those exiting or moving into expected.

What we are reading this week

Apologies for a shorter list this week, trying to clear the decks ahead of a week’s holiday.

Citi has decided the best move to attract junior bankers is to open up a Malaga hub – 9fin-ers have made their suggestions to senior management, will let you know where our next hub is.

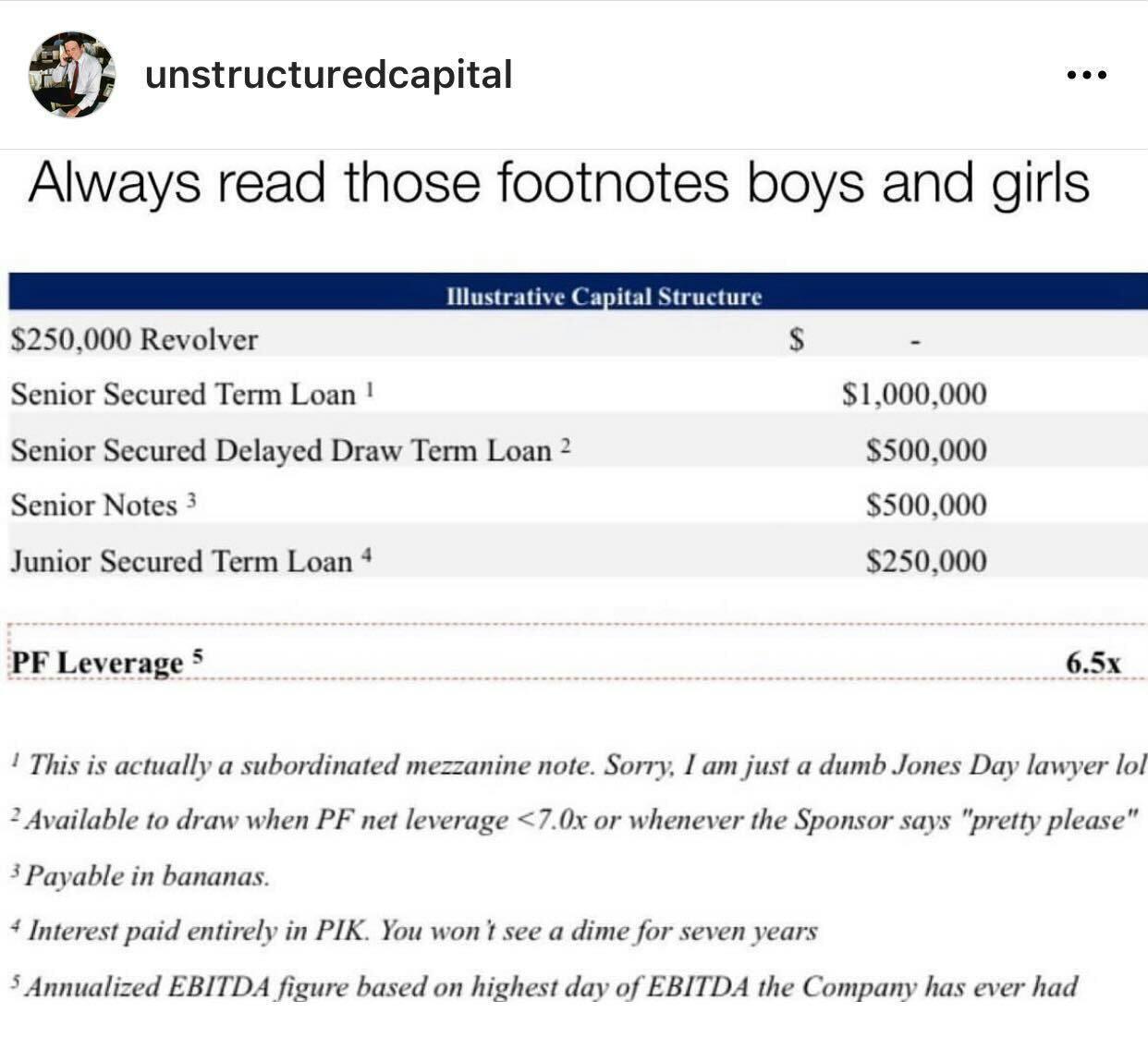

9fin’s credit and legal analysts are meticulous and renowned for their attention to detail. A good reminder to read the footnotes in cap tables.

And finally, a couple of plugs for 9fin content. Our Citrix coverage has resulted in a huge amount of inbound this week. The title should pique your interest:

Cloud9fin our weekly podcast had its first anniversary this week. Hosted by Kat Hidalgo, there have been some great episodes over the past year. Catch-up with the latest bonus episode on Citrix and the archive here.

The Friday Workout is escaping the Royal queues and heading South West for a week, it will return on 30 September.