This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Last week, we said markets were at an inflection point after a sharp retracement since July. Easier financial conditions could lead to Central Banks hiking further and harder, with markets far too relaxed about sharp rises in power prices amid supply concerns, we cautioned.

Fast forward a week, and government bond yields are moving sharply higher, with energy prices and security of supply topping market fears.

Overnight index swaps are now pricing in +194 bps of further rate hikes from the ECB (in addition to 50 bps in July) by June 2023, as investors price in increasingly aggressive moves. The iTraxx Crossover also took fright and hit 550bps this week, almost 100bps wider than last week’s tights.

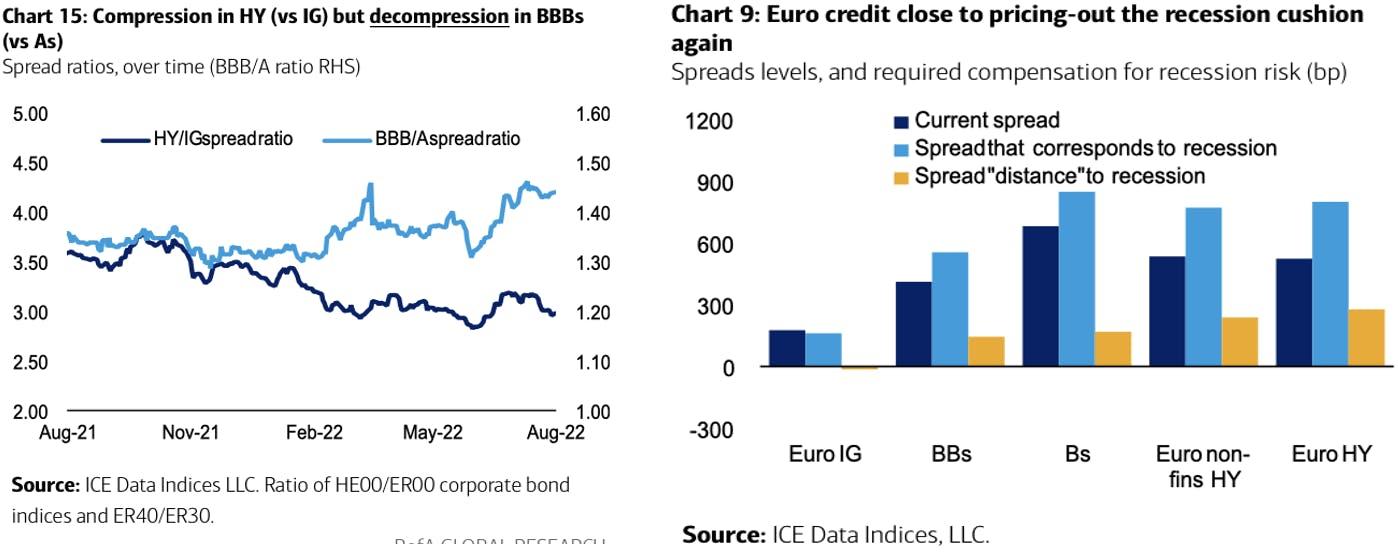

Some might think we are moving into fairer value territory here for HY, but as BofA cautions the spread compression to IG over the summer to 2.9x, looks tight, and is not pricing in recession risk. In addition, HY leverage rose marginally in Q2 to 6.3x, which is 0.7x wider this year.

Source: BofA credit research

While in general Q2 reports have been encouraging and supportive for risk assets, as pricing power remained strong with some catch-up from lag effects, the third quarter could be very different as economies slow and the cost of living crisis bites.

In addition, the fourth quarter will throw up even greater uncertainty. Despite some decent progress on gas storage. Will we be able to power our businesses and heat our homes (even if you could still afford to) as energy supply concerns mount?

For now, the surge in gas and power prices shows no signs of abating.

If anything, spot prices are accelerating, with European natural gas futures hitting another record high of €292 per megawatt-hour on Wednesday. Gazprom has another maintenance shutdown for Nordstream 1 in early September, and there was further bad news that Freeport LNG’s Texas gas terminal will not restart until mid-November rather than October as previously guided.

German Power prices are an incredible €643 per megawatt-hour, up from €513 last Wednesday and today, OFGEM announced the UK’s energy price cap will rise 80% to £3,549.

Wepa Wipes poor Q1

Sometimes all this can just sound like a bunch of numbers. It can take real world examples to fully understand the effects of the volatility and uncertainty on high energy using corporates.

Wepa is one of the these. It is having a rollercoaster year, and it’s time to buckle up, as the ups and downs in the second half might result in an even more scary ride than in the first half.

In Q1 22, the German tissue products and kitchen paper producer saw most of its profitability wiped out, generating just €2.5m of EBITDA for the quarter. Margins were tissue paper thin falling from 7.7% at FY 21 to just 1.2%.

Roll to Q2, and it cleaned up the mess from Q1 with €36.9m of EBITDA with margins a much thicker 8.9%. Some way below its 11-13% target, and may struggle to hit a 7-handle for FY 22.

The reason for the impressive turnaround, was the impact of price increases – on average they are up 38% since mid 2021 (most came into effect in Q2) - with energy costs stable to lower during the quarter (it had also implemented a ‘temporary’ energy surcharge to customers).

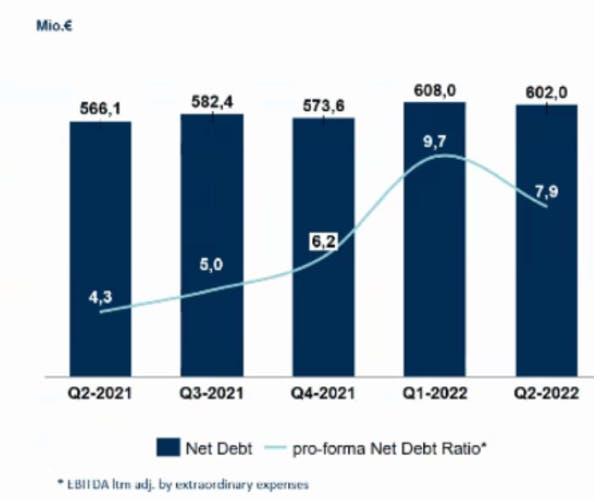

But since the end of the quarter, it has seen prices rise dramatically for pulp, packaging, paper for recycling and energy (60% of their production costs) as their slide below illustrates:

Incredibly, since early 2021, gas prices have risen by more than 15x, and electricity by 12x.

Wepa says it has deliberately underhedged itself compared to historic levels and is 55% hedged overall for the rest of 2022. Given the current ‘tremendously’ high prices, management said they will continue to hedge at the lower end of historical percentage ranges for their rolling hedges - set for one-to-three years. Citing commercial sensitivities, they declined to detail how much existing hedges had benefited the second quarter earnings. However, low cost hedges are rolling off and more expensive hedges have been taken on at elevated prices, they cautioned.

But the main concern for management is energy supply, gas in particular, with its German and Italian plants the most impacted, with Netherlands, France, Poland, and the UK less so.

Wepa has modelled a number of risk scenarios and expects gas rationing of around 20-30% in Germany this winter. Contingency planning - including shifting production runs, producing semi-finished goods, and using alternative fuel sources – can halve the impact of any energy curtailment, it says. It continues to lobby government via industry associations but at the moment there is no sign that the authorities would deem it a protected industry, management cautioned.

Given the ‘tremendous’ volatility in energy and input prices the delta for the fourth quarter could be huge. It is very difficult to predict if and exactly when industrial producers might see their energy and gas supplies cut, it could even be as late as the same day, management said. (I would recommend hiring weather forecasters as outages are likely to be linked to cold spells).

Worst still, some countries have capped gas prices for certain periods of time, others have not creating severe imbalances within European industries, notes Wepa.

Wepa has so far increased its prices by an average of 38% after attempting to push through three rises of 15%, 15% and 10%. Another price round will be attempted in September, with management saying that it would be higher than the 15% rounds, as this would not be sufficient to cover the ‘tremendous’ increase in costs.

Customer contract lengths were reduced from 12 months on average to three months to enable more frequent price rises. Management admitted they would “have to stay fair” with their customers and pass on any future input price reductions as “it cuts both ways”.

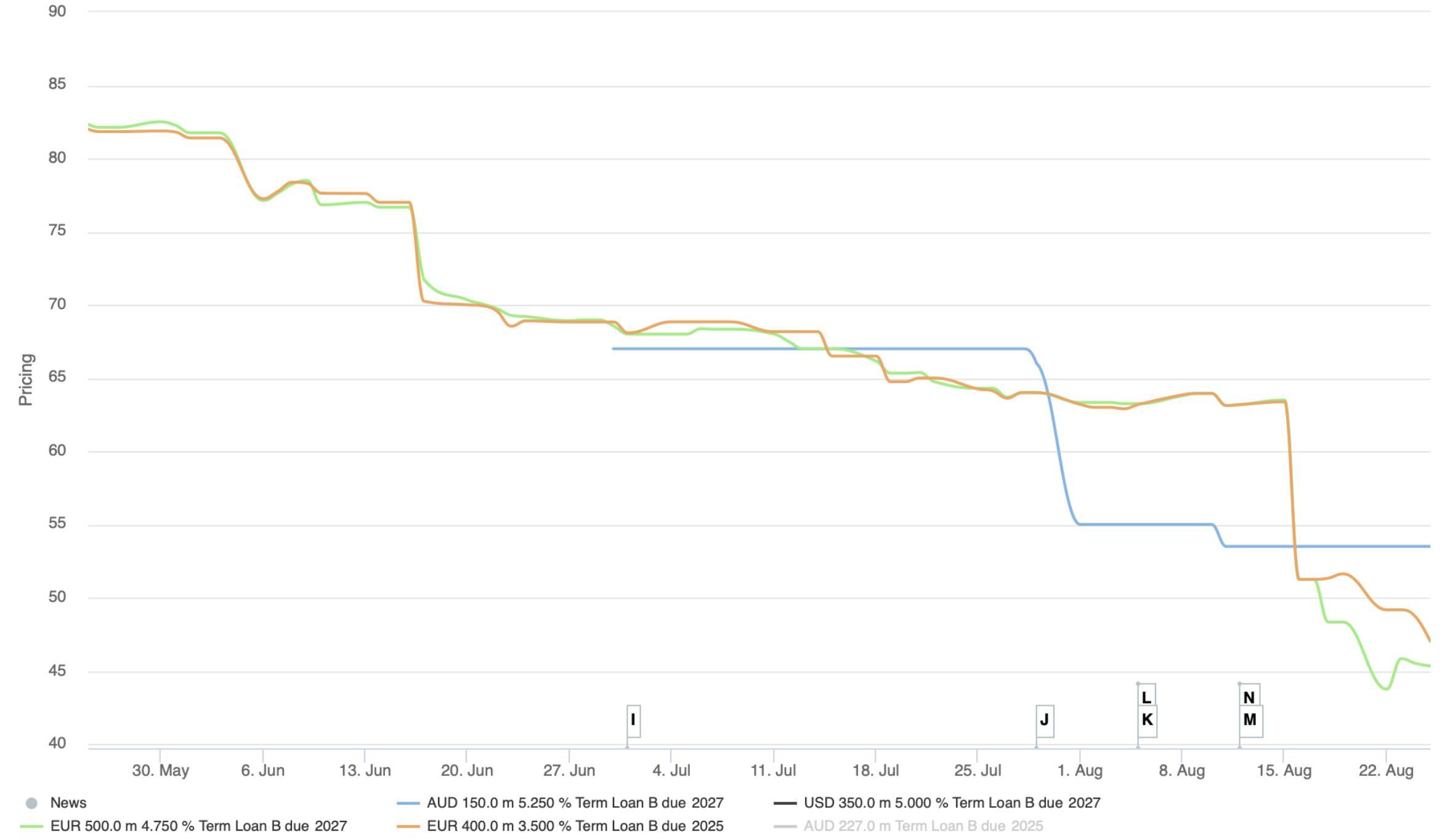

Wepa’s bonds are trading in stressed territory - their leverage has risen sharply this year - but this reduced to 7.9x in Q2 from 9.7x in Q1. Given the wide range of outcomes it is difficult to forecast where it will be in 2023. S&P yesterday put its B+ rating on negative outlook and now expects 7-7.5x leverage for FY 22 and 5-6x in 2023.

On a more positive note, some of the liquidity concerns were alleviated after the non-recourse receivables June 2023 ABS facility line was extended for five years and increased to €220m. No drawings were made under the €75m RCF, and given their preference for the ABS line, they said there was no need to negotiate with the banks over waiving the springing covenant.

After peaking at 9.25% last month, do you still see value in the bonds at around 7.75% yield? Better to wait for greater visibility after the Q3 earnings?

Why Wait?

One of the lessons of 2022 is that those borrowers which decided to ride out the volatility and wait for better conditions and better pricing got it badly wrong.

As maturities loom and debt goes current – if due in less than one year auditors and ratings agencies get twitchy - pressure ratchets up on management, whose attention should be better spent running their businesses during these increasingly difficult times.

Earlier this year, the Workout might have been more empathetic towards some names, who were waiting to show a better track record of post-Covid recovery to investors. As the year goes on, and we spend more time looking at individual refinancing candidates, we are much less sympathetic despite the tricky financing market.

Our often cited example is Schustermann & Borenstein (renamed BestSecret). At close to the worst point of the market (in mid-July) it priced €315m of Senior Secured FRNs at E+600 bps at 85, with a 1% floor - an all-in margin in double digits. Our May 2021 deal prediction suggested they could have refinanced (potentially with a dividend recap) with a 5.5% coupon.

Hope is not an investing refinancing strategy

Last night, I listened into the Q2 22 conference call replay for LimaCorporate, another name on my refi watchlist. After an impressive Q1 and with a looming August 2023 maturity, earlier this year I was surprised by management’s inaction.

In the interregnum they had managed to extend their RCF to July 2023. Nice work gents, but surely getting the bonds extended first would have been better - and given more RCF runway?

It’s difficult to understand why the company is complicating this so much.

The Italian manufacturer of medical and dental instruments and supplies is doing well. Sales for Q2 22 were up +14.8% YoY, EBITDA was up +2.2% YoY, and net leverage fell by -0.1x to 4.9x versus Q1 22. The group was marginally FCF positive in the first half, boosting its cash position by €8.2m to €29.7m (admittedly €54m of the €60m RCF is drawn).

Back to the Q2 call. It was dominated by investor questions on the bond refinancing options. I have reproduced their answer in full (without editing) - to show the full orthopaedic trauma:

“On the refinancing, it is my priority, my priorities, something that I’m working on. So maybe some months we have done kind of step one down the road of the right financing, the buying of some more time. Let’s put it this way. So as I mentioned before, to expand the RCF maturity until July 2023. So then we we had some more time to think about all this. Nevertheless, nevertheless, we are working on all different dimensions of how to make and resonating with our shareholder.

So in I don’t know if you had the time to like download the presentation before for all of us on page 11 we say that on the fourth bullet that we’ve been able to postpone the RCF maturity and then we say LimaCorporate may at any time and from time to time seek to refinance outstanding debt in the open market to purchase this or privately negotiate a transaction or otherwise.

So with this kind of open sentence that we say that we are kind of busy on all in all ways to, you know, making the right financing. And we don’t, you know, close the door on on any opportunities that they may come. As I say that I’m working through this myself personally, actually, with my team, of course, and and ready to see the time. It is difficult to call because, you know, you see that the market volatility in this last month or since February, I would say, when the war begun is very high, not only the stock market. Sometimes we read that one day plus 5%. The following day. Now there were -5%. But also the you know, the volatility in the in the bond market, in the notes floating notes market is not helpful. Unfortunately, we’re not in the same situation, which we were in 2017 when we opened up with this bond and that we’re all conscious that the interest rate that we will be paying them will not be the 3.75% that we are paying now.”

Nice, straight to the point, very clear and concise.

If you are digging a hole for yourself, stop digging. But management gets a bigger shovel and mixes metaphors for good measure:

“But um, you know, the more the market that will stabilise, so basically we have to be the, to say we have to be really, you know, if you throw the arrow when you know the we see a good window in the market if we catch. So we want to be ready. We will be ready right after the summer. And as soon as there’s a proper window, you know, we will jump on the window to collect the proper opportunities. So I would say from from September on, there will be, you know, ready sitting there by the river, you know, to ready to jump in to grab the opportunity to make a proper refinancing. And the least of course of cost as possible.”

Hope is not an investing strategy. After further questioning:

“We are, you know, active in all possible scenarios. So refinancing the debt or private lenders or anything that we’re looking at. Of course, this terrible solutions are in terms of cost, which are evident, of course, and that we will make in such a way, you know, so so we don’t we don’t you know, we don’t close the doors to anyone for the time being. But we will be very wise in taking the opportunities that the market will bring.”

I will leave it to Workout readers to decide on their wisdom. Getting a little more serious for a moment, interest costs are likely to double, and with minimal FCF generation and €54m of RCF to clean down, they could need more support from their shareholder to get a refi away.

The shareholder support question came up on the call - the response didn’t entirely convince:

“I'm sure the shareholders will do what is needed to help the refinancing. All that I mean, I, I don't know of course is that is needed on all of these that we're a bit too early in the process. But but it'll be easier sitting next to us/”

Too early in the process? The €20m of shareholder funds injected during the pandemic was cited as evidence of their support. Despite all of this, the bonds appear relatively unfazed - quoted at 96.5-mid - but is 3.5-points upside for a year enough in the current climate?

Everything is looking Peach now

Deciding to wait can also backfire if you in are an industry that suffers a change in sentiment and/or a rerating. A great example is the German Real Estate sector, and aside from the troubles at Adler and Aggregate, there are a couple of names with upcoming maturities which demand our attention - Peach Properties and Accentro.

Peach is reporting next week and we will spend more time on it, in our upcoming second part of Blessed to be Stressed (with Veon), so I will concentrate on the latter.

Accentro is an interesting sit. It has €250m of bonds due in February 2023, recent performance looks decent on first blush and has significant amounts of cash and cash equivalents (€158.9m). Elsewhere in the debt structure are €100m of private placement notes due in 2026, which should leave plenty of room for an A&E, if you decide to use some of the cash to sweeten the deal.

One problem is that you would end up with a small illiquid deal, and if you needed a cash sweep too, the 2026s might block. But what about if you issued more 2026s - surely that could work?

But why are the bonds indicated at 54-mid?

Could it be down to concerns over the Azeri ownership and their alleged connections to former owner Adler, and potentially as short-seller Viceroy suggests, to our old friend Cevdet Caner?

There are some serious complications and a lot more nuance to the credit than first meets the eye. All will be revealed in our piece next week, so, I won’t spoil the surprise.

Hurry up and wait

For some companies it has paid for them to wait, but they are outliers. Raffinerie Heide comes to mind, with a once in a generation boost from record refining margins.

For every Heide, there are many more Matalan’s.

Last weekend, Mark Kleinman at Sky (often the favourite forum for leaking and shaking things up) said that founder John Hargreaves’ planned contribution of £25m to £50m would not be enough and that creditors wanted a sale. I suspect this is mostly posturing and a agreement is still more likely (but John, it probably needs more than a Hawaii). I would love to know how close they got to covering the book in February, and at what price.

The current financing hiatus does throw up some other options for companies. Do you tinker with some of your excess cash to buy back some of your 2023s at a discount? Gone are the days that they would trade just a point or so above or below par if they were due in less than a year, so the gains can be meaningful. But do you leave your order with a dealer, or launch a formal tender?

Peach Properties took this to another level, borrowing using senior secured paper to repay chunks of its 2023 bonds at a discount. If you don’t tender, you are at risk of being primed if they default at maturity or offer you an A&E. There is €181.29m out of the €250m original amount of bonds due in February 2023 after the last tender took out €19.21m at a price of 94. The 2025s yield around 10.6%, and trade with a 83-handle.

So if they want to, companies could even introduce some game theory into the equation, and even take advantage of low prices to do A&E exchanges at an implied price discount.

Kerry Jones sums it up well: So hurry up and wait. But what's worth waiting for? So join the queue me and you. Wait in line. It takes our time to be satisfied.

Whitelist Woes

I had an interesting conversation in 9fin Towers this week, with Excess Spread’s Owen Sanderson. One prominent bank trading desk was so concerned about the presence of whitelists for one distressed loan name - our highly-educated guess is that it was GenesisCare - it wasn’t willing to trade the name on fears that the sponsor would retrospectively tear-up trades.

Put in place as a protection by sponsors to stop distressed funds taking over their businesses via a loan-to-own strategy, their presence wasn’t seen as particularly egregious for CLOs at issue. After all in many stressed situations, they could be more aligned with the sponsors than someone who would want to extinguish most of the debt and drive the value via the equity.

But as Owen mentions in this week’s Excess Spread making it harder to sell to loan-to-own funds with a much diminished list of potential buyers will mean that price moves are often more severe. Existing lenders are unlikely to want to add to their positions (most are probably trying to exit) our aforesaid dealers are not motivated to run the paper as inventory, and are marking prices down.

I would add another point, it opens up more opportunity for the sponsor to take positions in their own debt at a discount. This can complicate eventual restructuring negotiations and weaken lenders hand, yet further.

The presence of whitelists can also mean that sponsors can preserve their optionality for much longer. This can be to the detriment of lenders. Speaking to one GenesisCare lender this week, they were concerned that sponsor KKR could keep mortgaging the oncology care business via sale and leasebacks to mitigate cash burn, reducing the asset coverage for creditors.

As reported, the sale proceeds for GenesisCare’s cardiovascular care business was less than expected, and the projected turnaround for the troubled 21st Century US business will take at least another 12-18 months. Their loans are now indicated at deeply distressed levels.

In brief

Our deep dive last week for PDA proved prescient. We had said that “on balance, we suggest the near-term risk profile for the bonds and TLB in PDA’s cap structure is weighted to the downside.”The Q2 earnings release for the Dutch domestic appliances producer caused its bonds to drop 5-7 points, with the CEO talking about a challenging market environment. Too much time on the investor call was spent on new product launches, however. There was limited disclosure and visibility on the outlook and the Q&A session was cut short. Our earnings review gives more detail here and Emmet talks in depth on this weeks Cloud9fin pod. We have subsequently spoken to the company - if you want to know more - get in touch.

Douglas quarterly earnings to end June served up few surprises, noted 9fin’s Emmet McNally and Lara Gibson. The Germany-based beauty group is bullish on consumer spending despite a cost of living crisis. But is is facing competition from on-line only players, and is prioritising getting customers into stores to maximise revenues rather than boosting margins. Despite having at least €90m of capacity to repay sub debt under RP provisions there are no plans to buy back their 2026 PIK notes which trade in the low-to-mid 60s.

Cineworld continues to react to negative press news about a possible Chapter 11 filing - which we hinted was the most likely option in last week’s workout. We were reminded this week of another casualty, Sand Grove Capital Management’s margin loan put in place in September 2020 - we suspect that this trade is no blockbuster - this is one listing they don’t want to Vue.

The list of companies with European operations filing for Chapter 11 is growing.

Altera Infrastructure L.P., a UK-based offshore oil and gas service vessel provider, commenced Chapter 11 proceedings on August 12, 2022 in the US Bankruptcy Court for the Southern District of Texas. Endo International joined it, having filed last week, seeking to settle thousands of lawsuits over opiod usage and following the well trodden path of its peers, Purdue Pharma and Malinckrodt which also used the US process.

Amigo Loans has just £105.9m left on its loan book as at end June, a 63.3% decrease YoY. It has £70m of restricted cash and £102.4m of unrestricted cash, which is more than enough to repay the rump of its February 2024 bonds with just £50m outstanding. There was little further information on the planned capital raise and a return to lending (both by 26 February 2023). The FCA holds the keys to its future, as it has to approve its new lending model and quantify the amount of fines to be paid under two outstanding investigations into past lending.

What we are reading this week

Our favourite HY meme borrower AMC is still trying to convince the bros that it is different to Vue and Cineworld. After maxing out on their ability to tap their stock - which despite recent falls is clearly overvalued - they came up with a strangely monikered APE Units instead. We assume it is a nod and a wink to the Bored Ape NFT crowd (yes AMC has even tapped this well too).

The APE units are the issuance of a preferred stock unit for each share (eventually convertible into to common shares) to get around the stock selling restrictions. Despite ranking ahead in the event of an insolvency, the APEs are trading at a 27% discount to the common stock.

But as Matt Levine said you might want to think twice about trying to close the discount:

“Good luck with that one! I will not comment on it as a thesis except to say that AMC’s retail shareholders seems to be endlessly angry about short sellers, so if you want to short AMC stock as part of an arbitrage strategy, they will probably be endlessly angry at you.”

Petition as usual was prepared to poke fun at the meme-sters. They pointed the way to Donut Shorts and their extensive synopsis of Redbox Entertainment, which isan incredible tale.

Redbox was owned by the mighty Apollo. It then merged with a SPAC set up via Seaport. HPS later provided a private debt facility - with penny warrants to 20% of the company.

But it didn’t go well, it agreed a merger at a substantial discount to prior value with a stakeholder cram down which Petition commented:

“It is hard to overstate how rare it is to see Apollo in this position. Apollo has refined the ritual abuse of creditors to an art form, and yet here it gave up its board seats, lost its veto over any M&A transaction and, most remarkably, had its RCF crammed down into common equity with a prospective 85% loss. This set of facts is highly suggestive that Apollo viewed the Redbox equity as effectively worthless. As important, Apollo was looking to put distance between itself and Redbox and let it crash and burn on someone else’s watch.”

A remarkable story, already, but hold on there was an Act 3 - it became a meme stock - of course it did. Even though the voting was pretty much locked up to the agreed merger, the stock soared. They retail investors believed posts that an injunction to block the merger was coming a day after the vote - you have probably guessed what happened next - it never did.

I was reminded this week, of one of my favourite articles of all time - and potentially one of the reasons why I was attracted from the sell side - to a sell scribe. It is Felix Salmon’s piece on the Gaussian Copula, probably one of the major contributors to the GFC. The elegant piece of maths was first published in 2000, but it never worked, as co-association between securities is not measurable using correlation.