This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

LevFin Wrap - BB King as Covid Blues delay pricing

Huw Simpson

+Michal Skypala

High Yield Primary

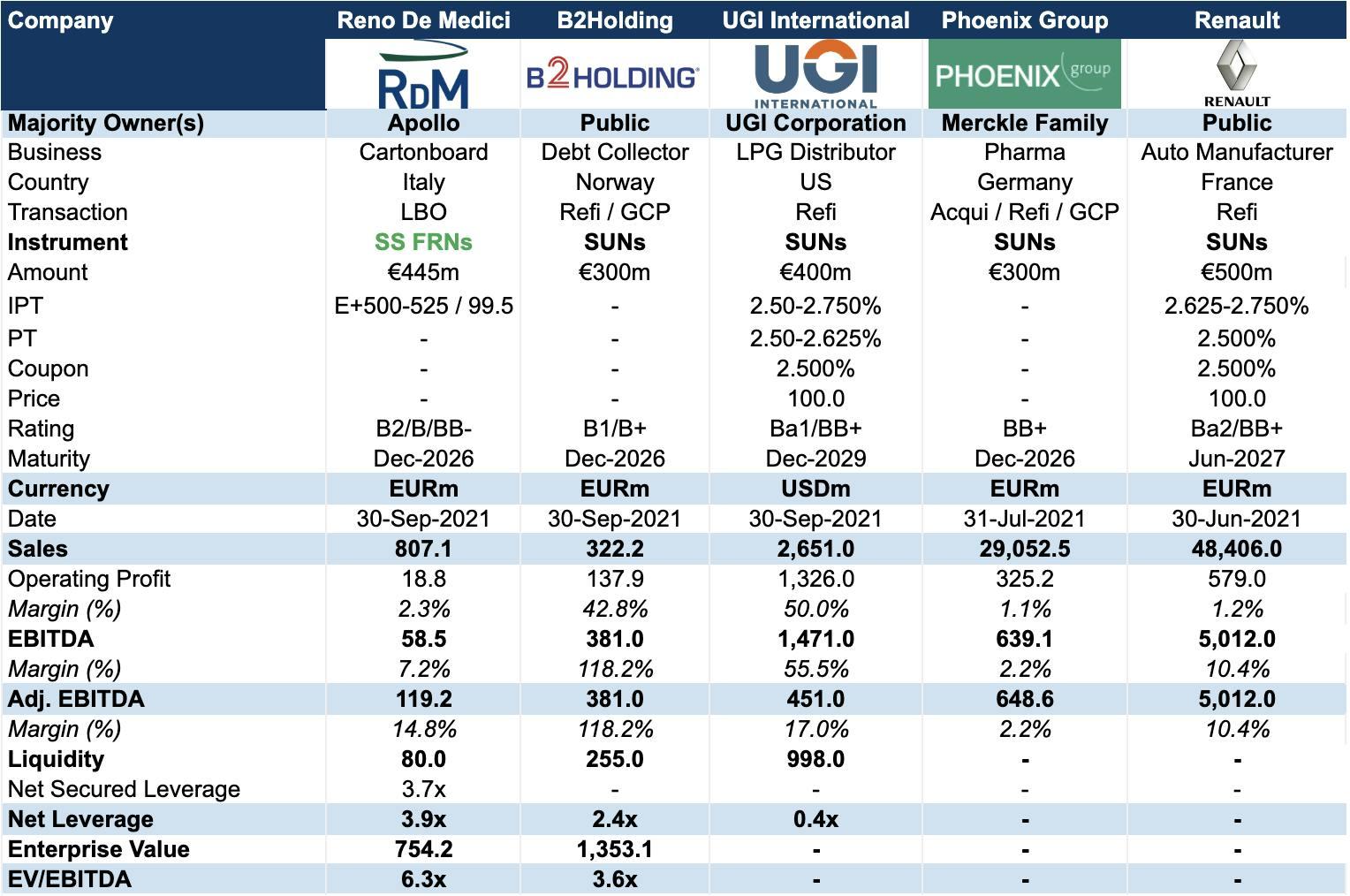

As we approach the end of November primary activity remains buoyant, but still absent several of the pending blockbuster M&A deals. Instead this week’s focus was weighted toward double BB names, and a lone LBO from returning sponsor Apollo. However, fears of a new Covid-19 variant and lockdown measures flipped sentiment on Friday, leading to some sell-offs in Secondary, and a push back on the timeline for Reno De Medici’s pricing.

Fresh supply arrived for investors in the European packaging sector, as Reno De Medici launched its LBO financing for Apollo’s buy-out. Together with a €294m equity contribution and €9m of existing cash, the newly offered €445m sustainability-linked Senior Secured FRNs due 2026 (B2/B/BB-) will fund the transaction – giving a 6.3x EV/EBITDA multiple. Apollo has been active with buy-out financing for Kem One and Graanul Invest this year, and earlier this month another of their portfolio names, Lottomatica, was in market with €400m SS PIK Toggle Notes to fund a €375m dividend.

Headquartered in Italy, the group produces and distributes recycled cartonboard for the packaging industry. EBITDA margins have been squeezed by inflation and higher energy costs, down to just 5.3% in the nine-months to September (13.9% in the prior period). Over this period, raw materials have risen from 69% to 80% of revenues, pushing the group to raise prices five separate times in 2021.

Despite this, management presented Adjusted Pro Forma EBITDA of €119.2m, which includes €10m of anticipated cost savings, and €43.5m to normalize the impact of raw materials. This failed to impress one buysider, who described the add-back as “one of the most outrageous things I’ve ever heard… it’s absolutely bonkers to ask us to imagine this away, especially when costs are still increasing”.

On Tuesday IPTs were sent out at E+500-525 bps with a 99.5 OID, before leads today updated that due to current market conditions, pricing was expected to take place early next week. For more information our Credit, Legals and ESG QuickTakes are available in full. If you are not a client but would like to see the ESG QuickTake, please comp;ete your details here.

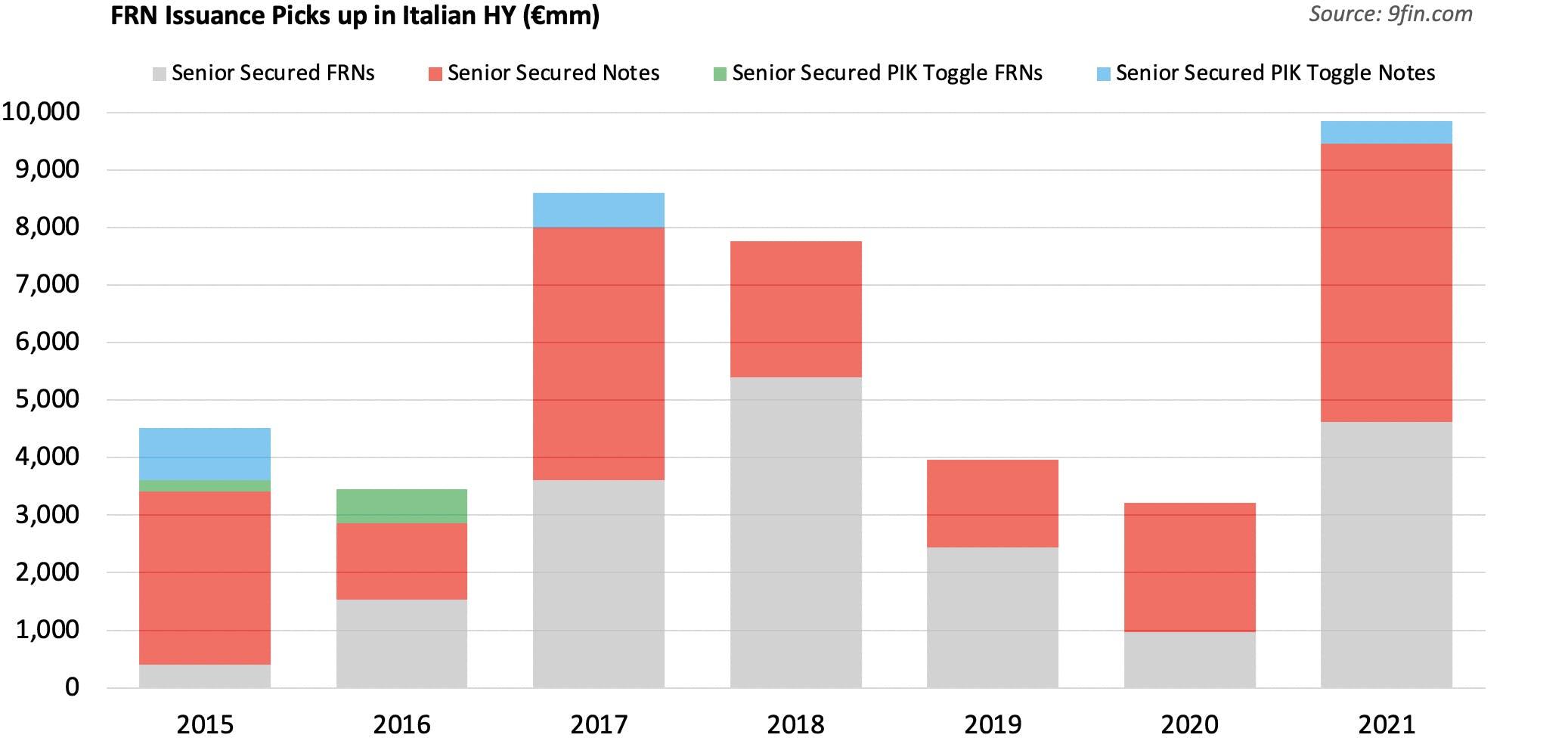

Regulation in Italy has historically pushed – and pulled – lenders into the bond market, with FRNs the closest instrument to a leveraged loan. Senior Secured FRN issuance year-to-date is now more than €4.5bn, improving on FY 2019 and FY 2020, and including Secured and PIK tranches, overall volumes from Italian issuers are now almost at €10bn.

BB King

Earlier this month, LPG marketer and distributor UGI International posted “solid Fiscal 2021” results, and followed up on Monday with a €400m Senior Notes offering due 2029 (Ba1/BB+/BB+). Proceeds will refinance the existing unsecured notes, and a small $45m wedge for general corporate purposes – or a distribution to the parent. Although parent UGI Corporation has no stated dividend policy, net of capital contributions the parent has paid dividends of $638m since 2016.

The LPG market in Europe is mature and declining, and as outlined in our ESG QuickTake UGI Corporation has set a scope 1 GHG emission target of a 55% reduction by 2025 versus 2020, and a net zero target for 2050. The 2050 commitment is a “positive first step”, but without an apparent net zero roadmap, and non-science based targets UGI is not currently aligned to the Paris Agreement. If you are not a client and would like to see the UGI ESG QuickTake, please complete your details here.

Pricing at par for 2.50%, the notes have since traded down, and were last seen at 98.7.

Elsewhere, Nordic debt purchase and collection group B2Holding mandated DNB, Nordea and Pareto for €300m Senior Notes due 2026 (B1/B+). The notes will repay a €50m bridge facility provided by DNB and Nordea (due May 2022), with the remainder for general corporate purposes, including a term-out of its €301m drawn RCF.

Leveraged Loans Primary

Loan primary is entering the last month of the year with the pipeline fairly empty, unless a supermarket sweep occurs before Christmas. Even with less to play, buysiders are not hungry for holiday paper after a record breaking volume year.

“It is almost December, so no push to deploy more money. We have to be selective, there will be funds flow next year. Generally if I’ve hit my annual target, I don’t feel the need to take extra risk,” said one buysider.

As expected in a tumbleweed primary, opportunistic add-ons had no issues in tapping the market for extra paper.

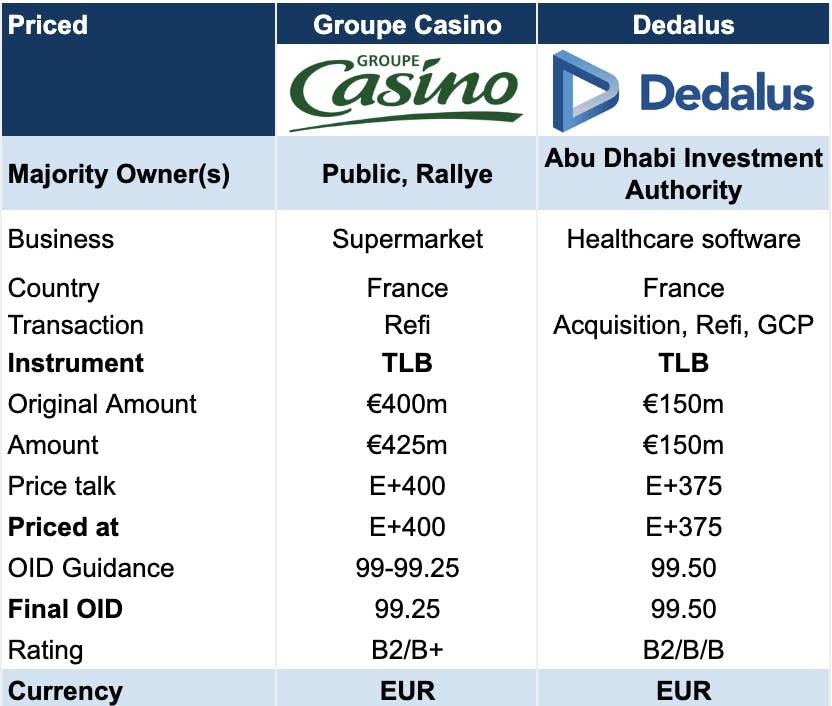

French supermarket chain Groupe Casino upsized to €425m from an initial €400m to the add-on of its existing €1bn TLB. The covenant-lite fungible loan will mature on 31 August 2025 and priced at 400bp over Euribor, the same as the existing facility, with a 0% floor and an OID of 99.25 (guidance of 99-99.25), according to LPC. The financing will go towards a tender offer for its 2023 and 2024 bonds.

Dedalus, previously touted as a “straight-forward story,” also easily priced its second add-on of the year at E+375 bps and 99.5, which was in line with initial talk. Even despite a data leak earlier in the year, the B2-rated Italian software provider for health care had no trouble placing €150m of additional paper. Clients can see our June 2021 preview here.

Primary turns Gallic

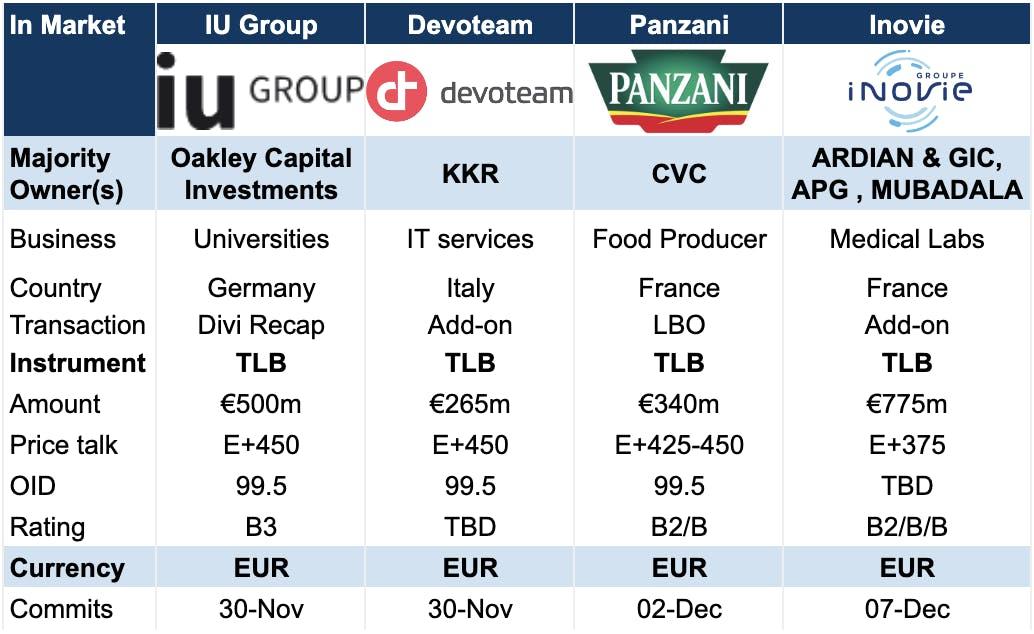

This week brought two new launches from the country of the Gallic rooster. French medical testing laboratory group Inovie is back with a €775m Term loan B add-on guided at E+375 bps aligned with margin and tenor with the existing facility maturing in March 2028.

Owned by Ardian, GIC APG and Mubadala it plans to repay its RCF, fund acquisitions and repay quasi-equity instruments plus transaction costs. The deal has two step down ratchets cutting margins by 25bps if senior net leverage goes under 5.1x and again if below 4.6x.

Another French ticket is Devoteam. The IT consulting and security business brings a €265m fungible add-on to its E+450 bps term loan due December 2026, with an OID talked at 99.5. Commitments are due by Tuesday (30 November). Proceeds will support a tender offer for Devoteam’s remaining listed shares. KKR and founding shareholders Godefroy and Stanislas de Bentzmann took control of Devoteam last year in a deal backed by a €370 million loan.

Bursary difficult to give

Early next week IU Group will be closing a new €500m Term Loan B due 2028 to refi €310m of existing debt and pay a €175m shareholder distribution. The education business generates decent cash flow and is fuelled by years of massive growth in student intake, but not all investors see it as a valedictorian of the current loan cohort, according to our 9fin preview. If you would like to request a copy, please complete your details here.

The largest German private university business is Oakley Capital’s star portfolio performer, but EBITDA numbers are in attendance dressed in add-backs that leaves leverage toppy after analyst’s sharpen their pencils for substantial haircuts.

The sponsor is dipping into the inkwell for yet another hefty dividend having received its full bursary investment back. Combined with a friendly portability feature for next two years some suggest Oakley Capital’s exit could be in the making adding future uncertainty for some, especially if things go south afterwards.

Price talk is set at E+450 bps and 99.5 OID with 0% floor. Commitments are due on Tuesday (30 November) at 4pm UK time.

Panzani will also test appetites, with the iconic French pasta maker serving up a €340m LBO cooked by CVC, taking the company private. The seven-year Term loan B is guided between E+425 bps and 450 bps with a 99.5 OID. The facility is rated B2/B and commitments are due by Thursday (2 December).

Investors are unsure about the credit, mostly citing unclear growth prospects given a leading position in a saturated domestic market. A bump from lockdown pantry-stocking covers up declining sales and market share. The deal also has an unpalatable recipe of small size and high leverage. More to follow in 9fin’s preview early next week.

High Yield Secondary

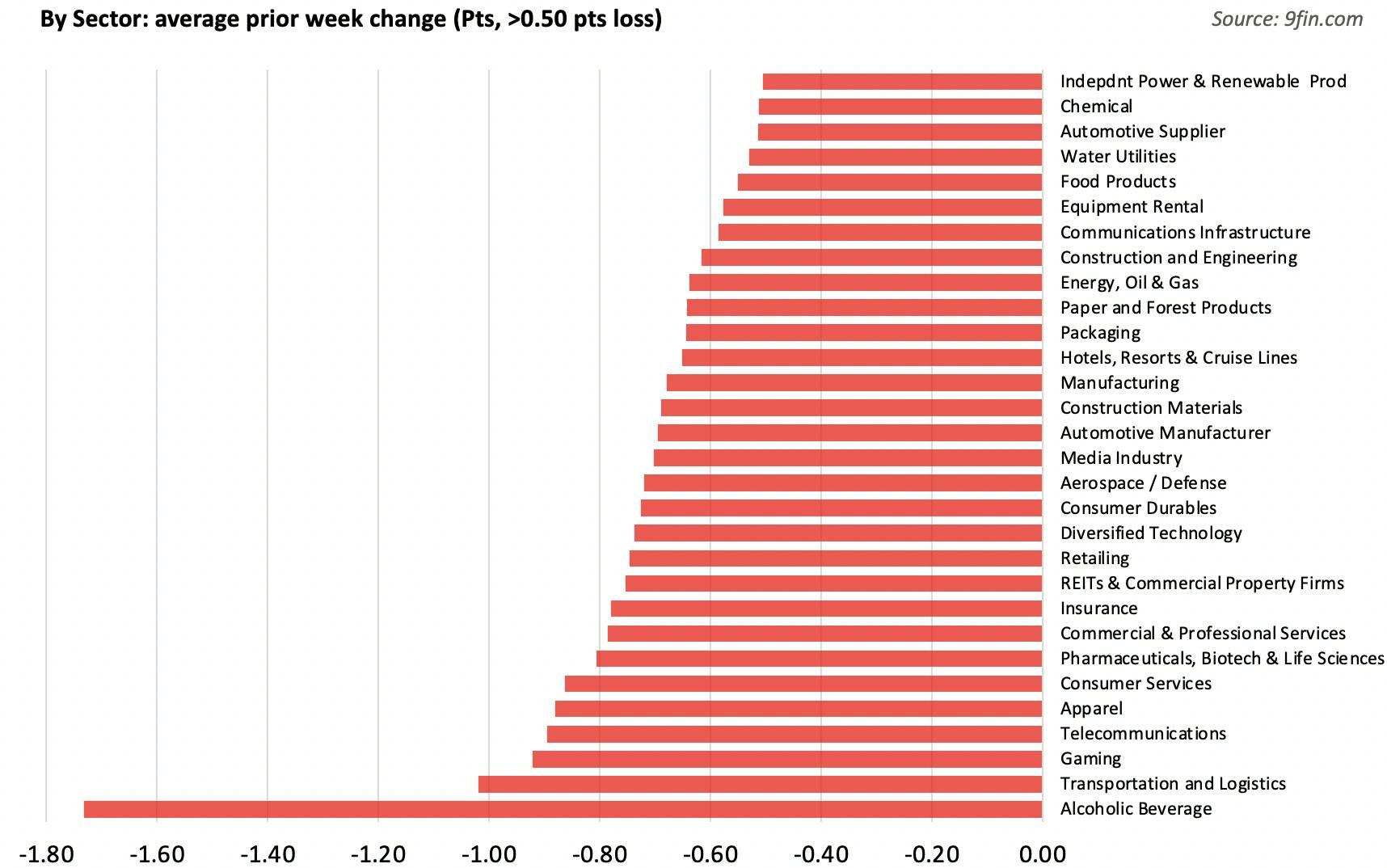

Markets softened considerably this week, trading down -0.69 pts on average, and over 90% of instruments registering a fall. New Covid-19 variants spooked stock markets, and we traced a daily average fall on Friday of -0.32 pts as this flowed into High Yield.

The iTraxx European Crossover widened significantly, to 281 bps from 246 bps last Friday. There were however inflows across all European domiciled HY credit funds, with Global HY +$239m, US HY +72m, and Euro HY +$475m.

At an industry level, Communication Services (-0.87 pts), Industrials (-0.79 pts), and Consumer Discretionary (-0.71 pts) marked the greatest losses, while Financials (-0.43 pts) and Utilities (-0.46 pts) proved more resilient.

Single names traded down heavily across the transportation and logistic sector; Carnival (-2.8 pts average), TUI Cruises (-3.6 pts), Lufthansa (-2.2 pts), IAG (-2.4 pts) and Air France KLM (-2.3 pts) fared worst. Other affected names include Stonegate Pubs2025s which were down almost -2.5 pts to around 101.4, and fellow boozer Punch Taverns2026s which slipped -1.3 pts to dip below par for the first time since it’s issuance in June this year.

Finally, we look at two situations grabbing most attention this week:

Unsigned, Unsealed – as we covered in our pre-earnings coverage, automotive trim manufacturer Standard Profil has been hit by the uncomfortable duo of rising costs and reduced demand. Adding to this are liquidity concerns and the current absence of an RCF. The 2026 notes have struggled since late September, and are now down more than -4 pts on the week. You can read our post-earnings coverage here.

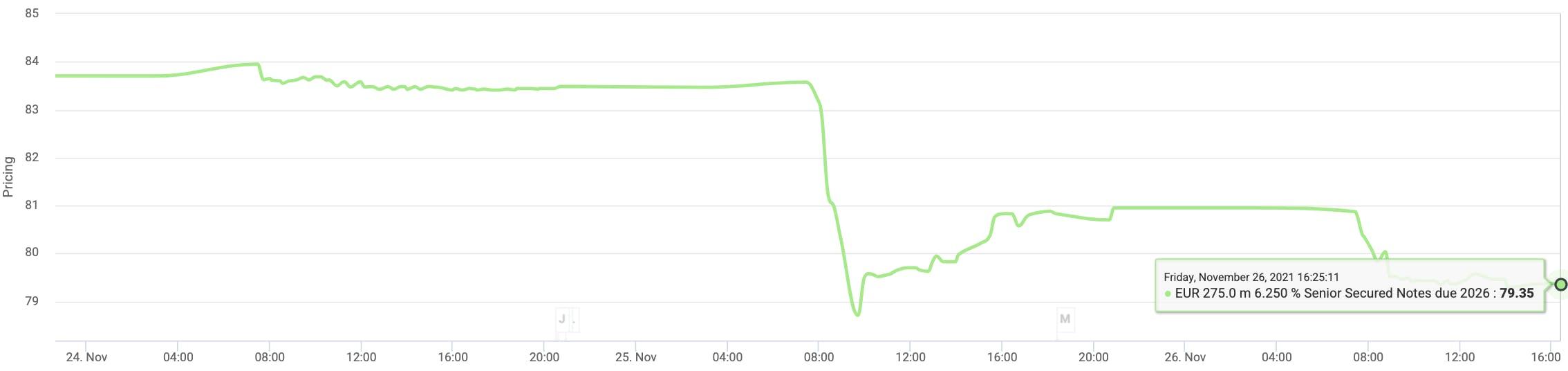

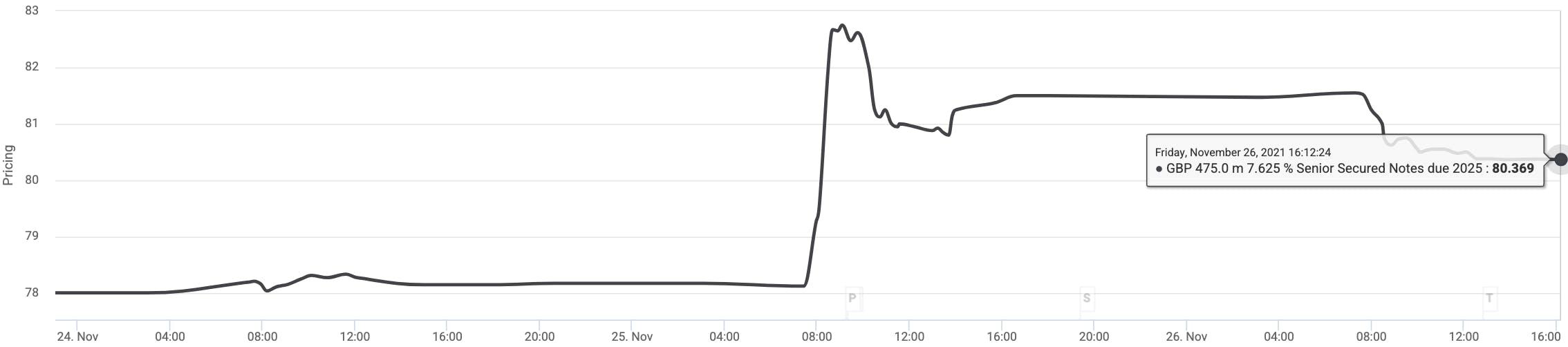

Plucked, but not stuffed – chicken producer Boparan announced predictably challenging conditions in its Q4 2021 results on Thursday. But in spite of these, news of a heavily discounted £50m mirror bond issuance, and a commitment to provide a £10m TLB will offer stop-gap liquidity. The 2025s recovered to the low 80s, before settling in at ~80.4 this afternoon.

Leveraged Loans Secondary

The secondary loan market had an eventful end to the week with jitters surrounding a new more virulent coronavirus variant appearing in Southern Africa. Even with US public holidays, the market was slightly down, mainly across lockdown exposed sectors.

“Yeah, everything is moving down today, we’re all keeping an eye on it. Looking again at our travel names, we've already been de-risking the portfolio a bit after Germany’s lockdown and other developments in Europe, said one CLO analyst. “Covid is almost background noise at this point.”

As expected, the biggest decliners were names with most to lose from prospects of fresh restrictions. Dutch retailer Hunkemoller led the bunch with its homebase already in lockdown with its loan falling two-points or 2.1% to 95.25 by 2pm London time on Friday (26 November). Swedish mattress producer Hilding Anders saw its loans slide 1.5 pts (1.7%) to 86.5, Belgian natural health company Inula fell a point to 99.5, followed by a decrease of 0.9 pts for Cineworld. Genesis Care continues its fall that started last week on the back of weak earnings and cash flow and elevated leverage as noted by S&P, down an additional 0.8 pts to 95.4.

LevFin Wrap is published weekly for subscribers and includes our forward pipeline. If you would like to see a sample of our forward pipeline please complete your details here.