This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

LevFin Wrap - Greenback has a purchasing power party as Powell fires in the Hole

9fin team

•8 min read

Another week of crickets in EHY primary with supply unlikely to return in earnest anytime soon. There was plenty on the macro front though: central bankers around the world descending on Jackson Hole, never-ending dollar strength, and a load of more pain in Europe’s energy situation.

All eyes were on Jay Powell who has just finished speaking in Wyoming. Following less-than-prescient comments at last year's symposium when he famously held the line on inflation's transitory nature, this year he erred on the side of caution and steered clear of saying anything too conclusive in a speech than took less than ten minutes. The main message was a hawkish commitment to the primary mandate of controlling price stability, whilst acknowledging the pain of higher interest rates.

Anyway, having initially discounted his hawkish stance on inflation that led to a monster rally across many assets in July, Fed funds futures have become more aligned with the central bank’s dot plot going into the meeting - although there is certainly still expectations of easier financial conditions in 2023. This may change over the afternoon as investors digest Powell’s brief remarks.

ECB representation won’t come until tomorrow in the form of Isabel Schnabel’s participation in a panel discussion (President Lagarde will be absent from the meeting again), but the July meeting’s minutes were released yesterday with some interesting takeaways. Most notably, some members had preference for a 25 bps hike, versus the previous hike of 50 bps, due to the weakening economic picture - this despite growing concerns among members that higher inflation is becoming entrenched.

And more gloomy headlines in the UK, with the energy regulator raising the price cap another 80% in October, meaning the cost of heating homes will be nearly three times higher this Winter compared to the prior year, and is only expected to get worse. The cap only applies to households, with no corresponding protection for UK industry. On Monday, Citi said UK inflation could hit 18% next year, with markets betting UK rates will hit 4% by May.

The hawkish chorus of Fed officials and worsening economic backdrop in Europe has pushed the dollar to fresh highs, ploughing through parity with Euro and 1.18 on cable.

Source: Trading view

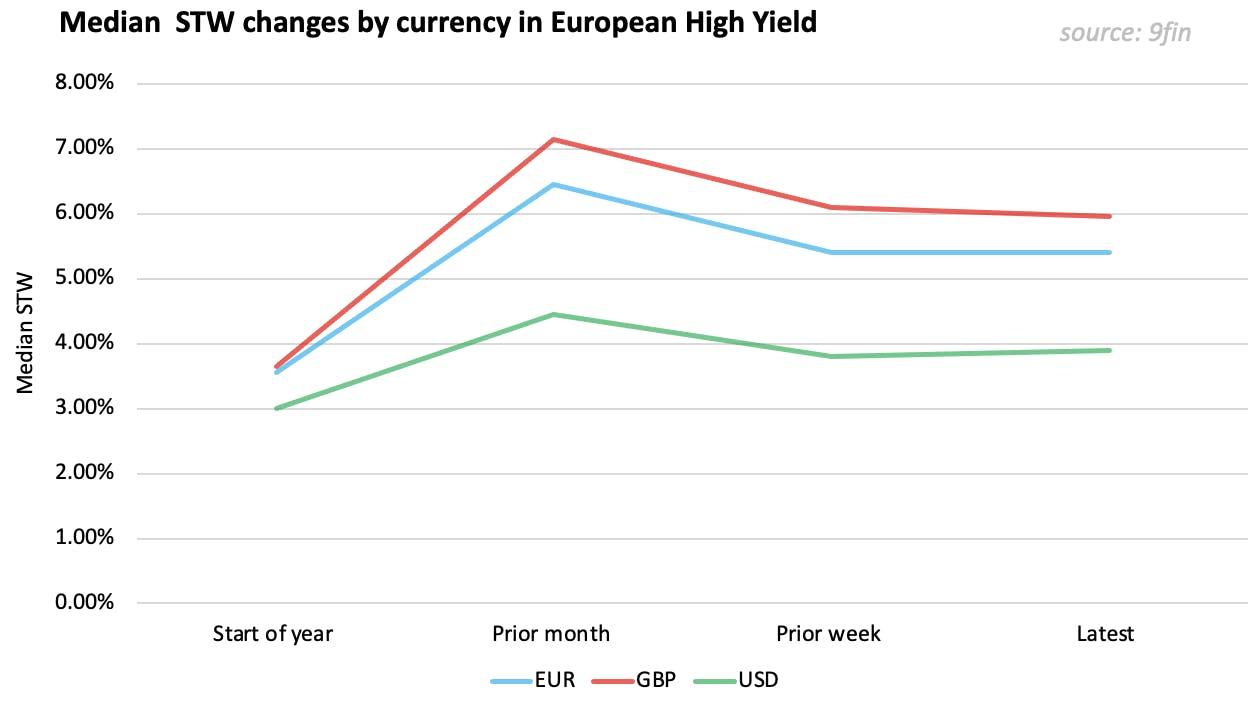

What’s the impact in High Yield? Well, one interesting trend we’ve seen YTD is growing spread differentials between USD- against GBP- and EUR-denominated debt - although there are likely to be other dynamics in play here.

As touched on in last week's Friday Workout, although absolute yields are similar, spreads have diverged significantly between currencies. With the median spread-to-worst at the start of the year for dollar-denominated debt 55 and 65 bps narrower than EUR and GBP respectively, that gap has since widened to 150 and 205, respectively.

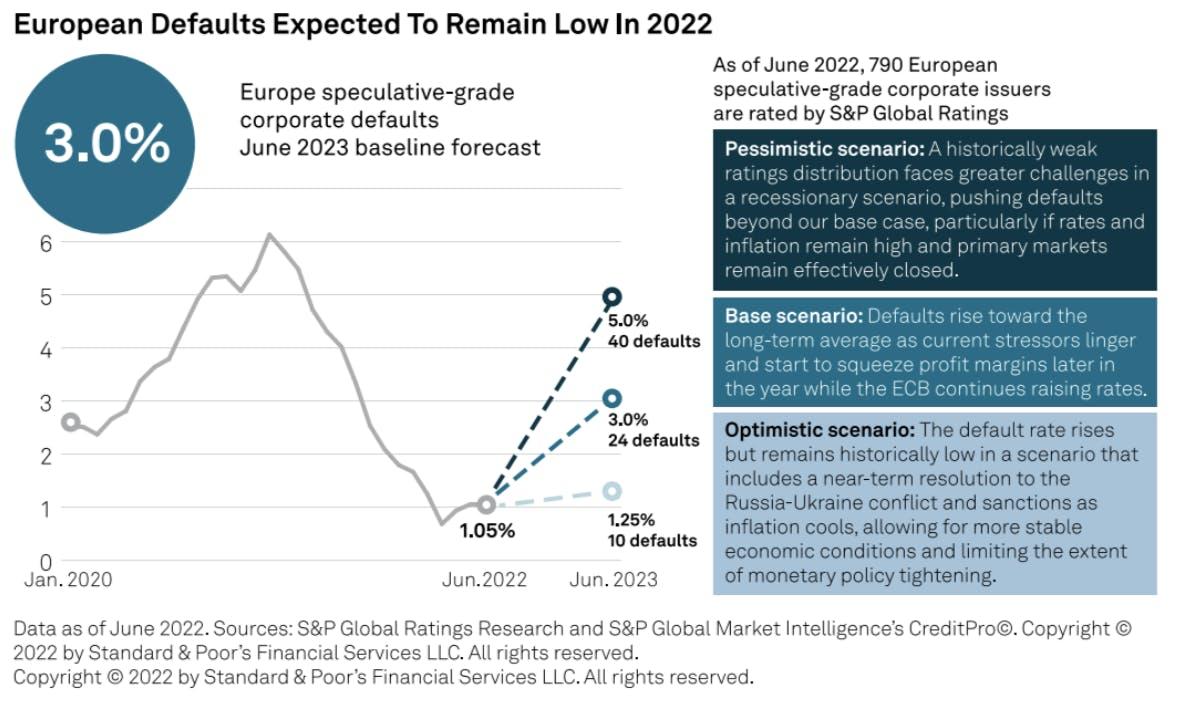

As with the UK, much of the economic weakness in Europe is thanks to the energy picture. European natural gas futures climbed another 32% on the week to Thursday’s close. The worsening situation has led S&P to dial up default expectations, which still look reasonable in their baseline scenario. European speculative-grade corporate defaults are now forecast to reach 3% by June 2023, from 1.05% prior year.

Cracks are showing in the dreams for September loans plenty following the traditional (and non-traditional) August lull for the leveraged loan market.

Despite buysiders relaying expectations of a busy autumn, one major bank said it only had one or two loans set to launch in September, estimating that around 20 of the 30 deals already underwritten were set to go to the TLA, private credit or dollar markets. This could leave as few as 15 deals between loans and bonds to launch in the syndicated market in September.

As 9fin’s Owen Sanderson points out, this leaves the CLO shops wanting to come to market (around 15) in a chicken-and-egg situation as they continue to hope for a healthy supply of loans to draw them out to print. This, in turn, keeps the syndicated loan market looking less than appetising for companies looking to raise funds.

The question of how long the private credit markets can step up to take re-directed loan deals is also rearing its head again.

One sellside source told 9fin that some direct lending funds are already fully deployed and are struggling to raise new money, leading to them cutting back on deals and becoming more picky in which deals they choose to play and modifying the terms they can offer.

“I expect direct lending funds to be more selective as they can access increasingly larger parts of the market,” an advisor said this week. “In terms of the upcoming pipeline, I will definitely expect direct lenders to take down more sponsor driven LBOs, particularly in areas they feel comfortable with like Healthcare and TMT.”

"We’re fully ramped for the year on LBO funds and [are] trying to raise new funds at the moment,” one private debt lender said. “But at the same time we have funds for M&A and IPO opportunities from four years ago you’ve not fully realised yet, which makes things more complicated.”

High Yield Secondary

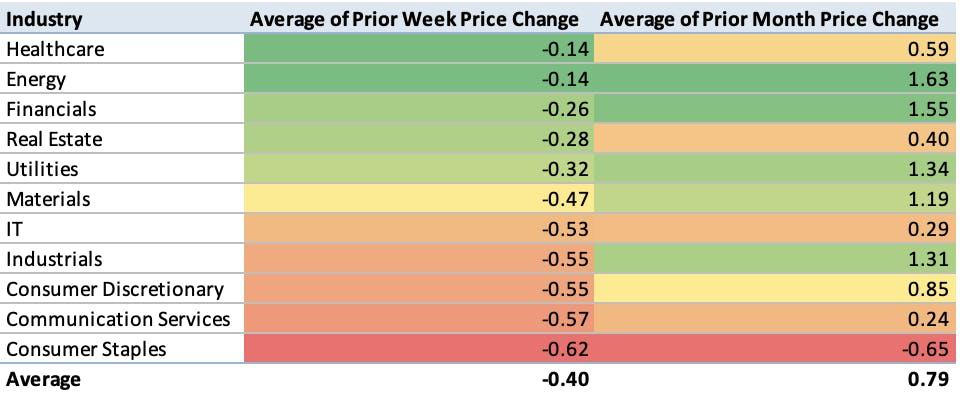

The iTraxx Crossover traced the gloomy macro sentiment and moved 38 bps wider on the week to close on Thursday at 530. This was in sync with instruments tracked by 9fin which were lower by an average of -0.4 pts on the week, with all sectors in the red. That wasn’t enough to offset a decent August performance otherwise, albeit on thin liquidity, where we saw an average gain of 0.79 pts.

As shown above, Consumer Staples was the one exception to a good August, unsurprising given the cost of living crisis engulfing Europe, with a particular tilt towards UK names in the sector. Asda, Co-op, Iceland, Ocado and Tesco all struggled in August as forecasts for the Kingdom went from bad to worse to apocalyptic.

Asda reported Q2 earnings this week, with very modest sales growth of 4.5% offset by a 25% decline in EBITDA. Lower volumes from consumers managing tighter budgets as well as price impacts necessary to remain competitive were the main drivers in the margin deterioration.

Source: Asda Q2 presentation

Elsewhere in single names, Douglassubordinated PIK notes rose ~3 pts after releasing Q2 results that didn’t deliver any nasty surprises. Management was also upbeat about current trading with sequential margin improvement for the German beauty retailer, although this was slightly offset by the growing influence of its lower margin e-commerce segment. For 9fin’s earnings review, see here.

B2Holding bonds received a ~5 pt boost this morning after closing a funding facility with Pimco. As discussed in this week’s Excess Spread, the deal is a reperforming loan securitisation backed by secured assets, in effect monetising B2Holding’s back book.

Tullow’s $1,800m SSNs due 2026 dropped ~3 pts as the tie-up with Capricorn faces resistance from Capricorn shareholders. Compounding issues is S&P revising Tullow to negative outlook on account of Ghana - where Tullow derives a significant portion of its production and revenues - being downgraded to triple-hook status. According to the rating agency, this means “there is potential that the Ghanaian state will implement tighter capital or foreign-exchange controls in the future”.

Leveraged Loans Secondary

Secondary markets were soft this week, reversing a multi-week rally that many in the space had hoped signalled a supportive environment for a September flood. Communication Services fell the furthest of sectors tracked by 9fin at -0.4 points, with Industrials and Consumer Stables the most resilient at -0.1 points each.

In this week’s interview with 9fin, Fair Oaks Capital’s Tyler Wallace explained August’s rally through the spate of priced CLOs in July that came with relatively low-ramped warehouses (around less than 25%). “The rating agencies usually require a minimum percentage of purchased assets at closing (e.g. 75%) so effectively the post-pricing CLO becomes a forced buyer,” Wallace told 9fin. “If several low-ramped CLOs price at the same time (like what we noted in the second half of July) – you may get a rapid increase in loan prices.” This dynamic, it appears, it abating.

Over on individual names, Philips Domestic Appliances (PDA) lost the most ground this week at -5.1 points on its €1.05bn TLB following its results at the end of last week. 9fin’s coverage of PDA’s earnings last Friday called the company out for a lack of visibility amidst a weakening consumer demand environment. Ultimately, leverage ticked up above 6x and the outlook for H2 22 appeared mostly negative with ongoing inflationary headwinds and an indication that pricing power is limited.

“PDA has been difficult. I still like the name, but I was disappointed by the results,” said one lender. “But really in many ways the results are self-inflicted because management is taking a long-term view of growth and that means short-term pain. It’s the same as Prosol, people have to think long-term, and recognise that a lot of the cap structure is still viable.” Read more on Prosol here.

Top movers were more muted. Spanish fishing company Iberconsa is up +2.5 points to 91.5 on its €300m 2024 TLB, with French margarine maker St Hubert +2 points to 72.8 on its €260m 2024 TLB.

French fine food firm Laberyrie’s €455m 2026 TLB enjoyed a minor reversal of +1.8 points to a still strained 72.2, with lenders remaining sour in their medium-term outlook: “Demand is going to be weak for some time,” said one buysider. “It’s not an easy positioning because the premium aspect of their products and a lot of its products are quite replaceable in a consumer’s diet. Salmon prices are soaring and that’s very easy to swap out for another protein for customers.”