This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

LevFin Wrap - HY goes hell for leather, Cirsa-cus is back in Town

Huw Simpson

+Laura Thompson

+ 1 more

•13 min read

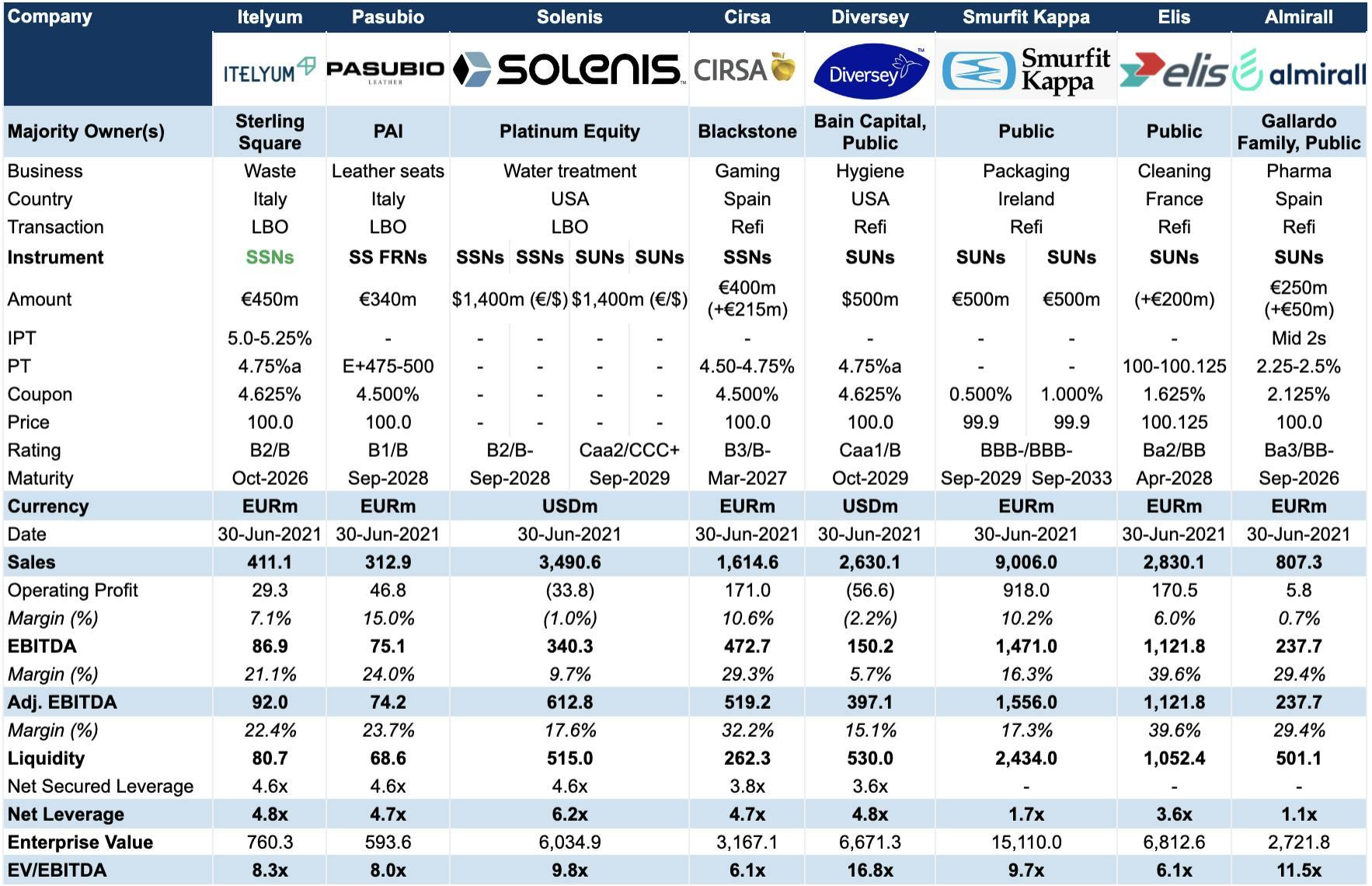

As expected, issuance returned in force this week, bringing a heady mix of refi’s, LBO activity and crossover names. Swollen books, tightening prices and new issuances trading up on the break all suggest plenty of appetite remains for the chunky pipeline ahead.

High Yield Primary

First up was Pasubio, a leather supplier for the automotive industry focusing on the niche premium and luxury market. Offering €340m in Senior Secured FRNs, the group announced the 7NC1 notes on Monday, which alongside a €275m equity contribution will fund the purchase by sponsor PAI (8.0x EV/EBITDA multiple).