This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Unsurprisingly, it was another muted week in primary following last week’s brutal sell-off that shows no signs of abating. Banks sit tight on droves of financings underwritten in rosier times, nervous to launch into a market where buy side capital is very much in charge. According to 9fin data, nearly a third of EHY debt is trading sub-90, so selling risk in primary is a tough ask when paper can be picked up on the cheap in secondary.

The sellside got the week off to the worst possible start, with syndication on Europcar’s sustainability-linked €150m mirror note stalling having launched last Thursday. Proceeds were earmarked to expand the fleet in anticipation of busy summer months, but growing risk-off sentiment proved too much for the French car rental company, who pulled the deal Monday afternoon.

That brings total pulled deals to six for 2022, with BNP Paribas (Europcar and Immobiliare Grande Distribuzione),Citi (Prax), Credit Suisse (Anacap), Barclays (Covis Pharma, shifted to loans with a steep OID) and UBS (ION Analytics) the left leads falling foul of testing market conditions.

I’m bringing High Yield back

With HY primary tentatively coming back in recent weeks, any deals looking to break the recent deadlock are going to have to do so under heightened scrutiny from the analyst community. That may or may not have benefitted Spanish football league LaLiga’s offering of €500m SSNs due 2029 and €350m SSFRNs due 2029, which had its fair share of complex structuring considerations and novel legal clauses. Our Legals QuickTake is a good place to start for those still unsure on certain elements. Non-call periods on the fixed and floating tranches are three years and one year, respectively.

The deal launched last Thursday, affording investors the weekend to wrap their head around the many idiosyncrasies. It had been pre marketed to certain large accounts before launching into general syndication, and it had been in the works for several months before that, with LaLiga’s executive committee recommending the CVC plan last August.

The sponsor will use an SPV that holds an 8.2% economic interest in what is essentially the revenue generated from broadcasting the league’s fixtures, less a few relatively small costs, to service the debt. The €2bn investment is being contributed through a “silent participation”, meaning CVC has very little direct control on how this money will be spent.

As discussed in our Financials QuickTake, a (if not, the) key risk is the value of these broadcasting contracts decreasing. This is mitigated by the league having tied up domestic broadcasting contracts, which account for around 60% of total TV revenue, for the next five years. After this, though, visibility gets fairly cloudy.

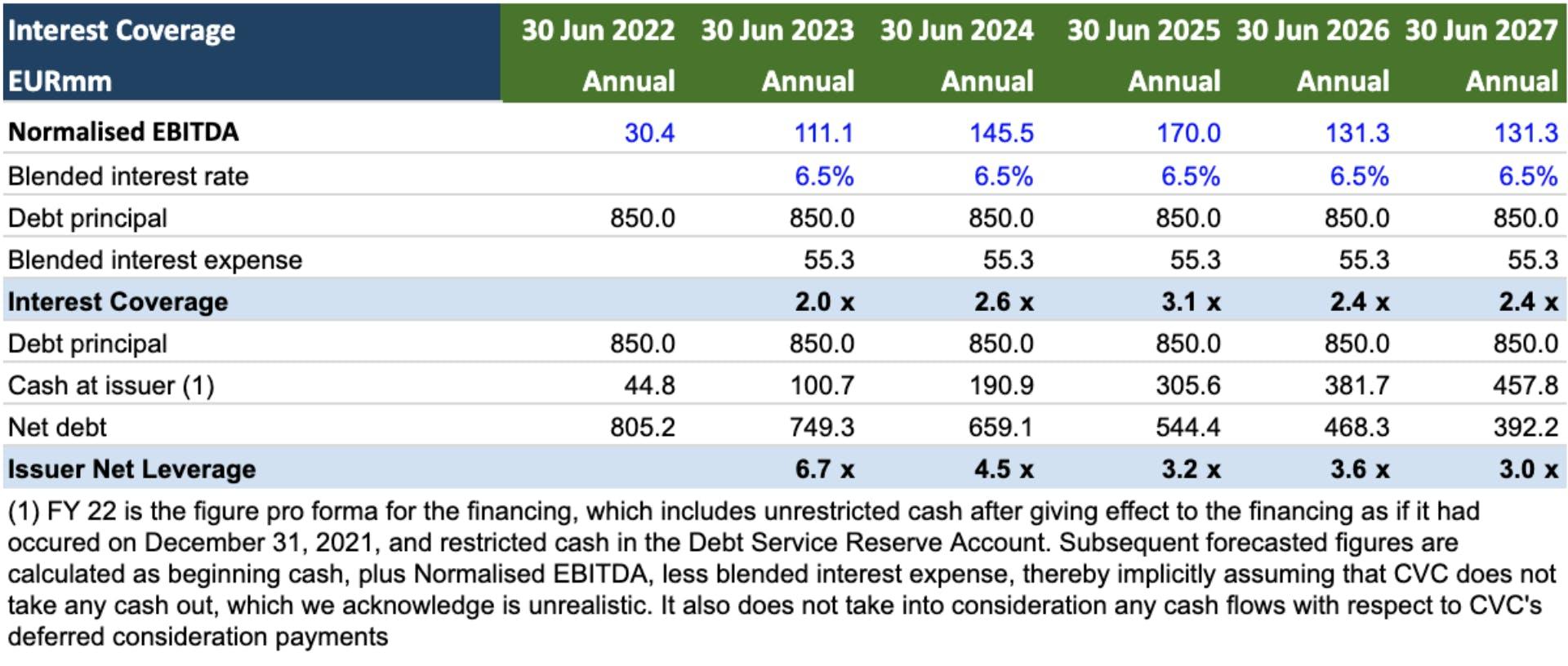

We modelled successful deleveraging from 6.7x to 3x by 2027, assuming (unrealistically) that CVC does not take money out of the Loarre SPV, and based on a 6.5% blended interest cost — illustrating that there should be a decent path to refinancing within the lifetime of the bonds, which is further supported by the lockbox structure.

However, hesitancy stems from Barcelona and Real Madrid, by far the leagues two biggest clubs and therefore biggest driver of broadcasting revenue value, jumping ship - the two alone are allocated ~20% of LaLiga’s TV revenue, and have thus far opted not to participate in the “Impulso” plan the bonds are backing. They tried and failed to leave the league last year, but a global outcry from passionate football fans (and pundits) put those plans to bed relatively quickly.

Termination of the SPSA (silent participation) or the shareholders agreement would trigger a requirement that the issuer apply proceeds received from LaLiga towards redeeming the bonds (up to the amounts received). However, departure of certain non-participating clubs would not directly trigger the termination of the SPSA or shareholders agreement. The issuer can renegotiate the economic terms of and/or terminate the payment of SP funds if there is a fundamental change to the league format (e.g. Barca and Real do not compete, unless relegated/for administrative reasons), but it's not clear how the renegotiations would look or what happens if they’re not successful.

Other questions are around CVC’s exit strategy, with this investment far from a typical LBO play. The extensive asset sale carve-outs suggest that co-investors could join or non-core assets could be spun out, perhaps to other PE or to sovereign wealth money, whose presence continues to grow in the sporting world. On the other hand, the investment could be something more long-term, with the potential to keep the SPV levered up and extract value via dividends.

Pricing came at lunchtime on Friday, with the SSNs landing slightly wide of IPTs of 7%, closing at 6.5% with a 96.61 OID to yield 7.125% to maturity. The floaters fared slightly better, helped by CLO demand, pricing on IPTs of E+500 and a 97 OID.

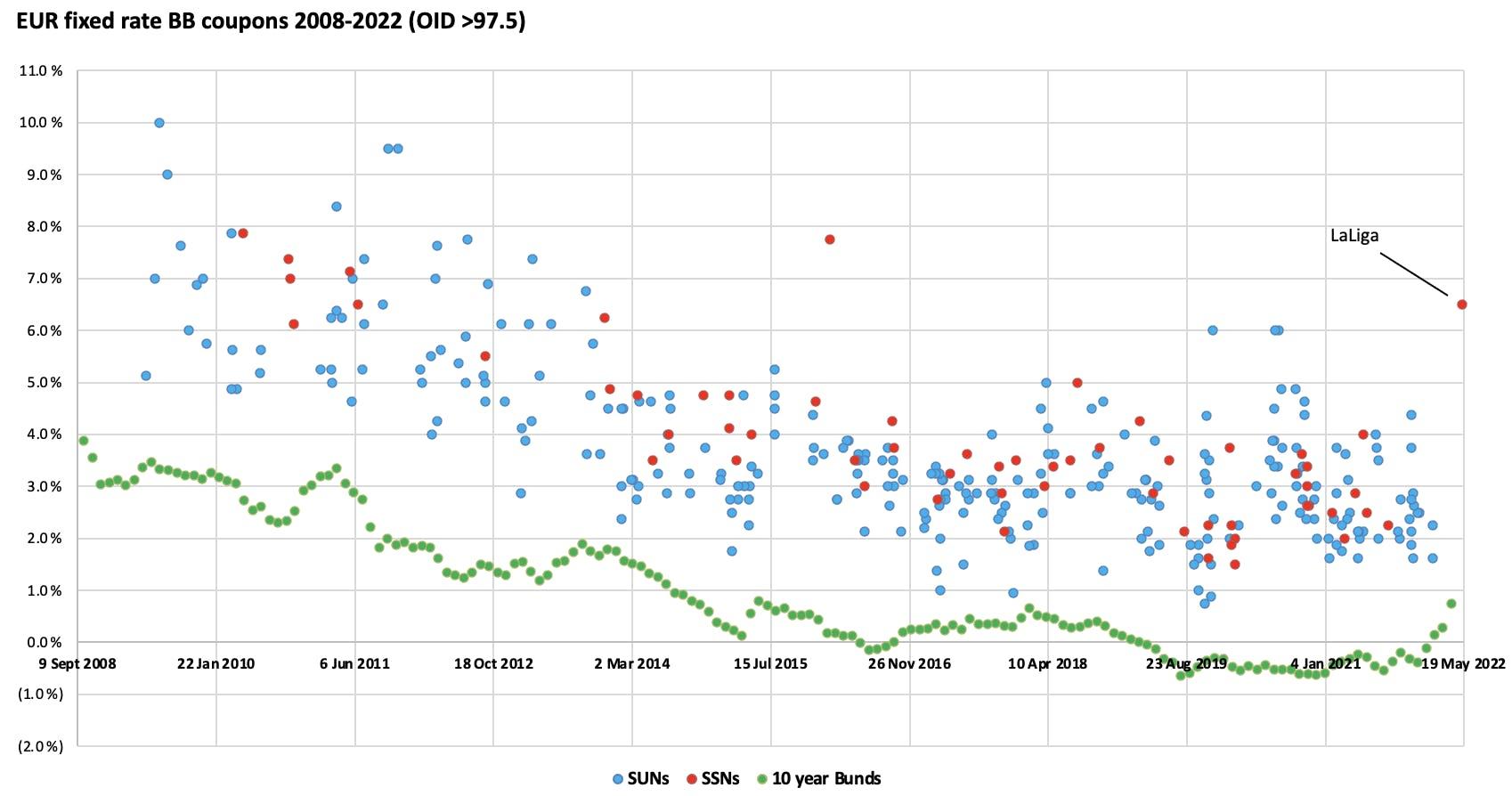

Those willing to stomach the structure are set to be rewarded. Removing Moby’s debut €300m SSNs back in 2015 that paid 7.75% (since restructured), you have to go back to November 2013 to find another senior secured BB paying north of 6%.

Even when acknowledging the complexities of what is securing the LaLiga issue, only three BB SUNs have paid 6% since 2014. (Note the chart below only includes deals rated BB by both S&P and Moody’s; we have removed 40 instruments that were BB with Fitch but single B with S&P/Moody’s. It just looks at coupon at pricing, disregarding OID. To compensate for the shortcoming, we have removed five outliers that priced at below 97.5, and LaLiga’s datapoint doesn’t include the 96.6 OID).

However, with no close comparable and the uniqueness of the deal likely to be contributing to a healthy premium, this could well be another outlier and not something fund managers can start getting accustomed to. Nevertheless, a complex financing of this sort able to get over the line hopefully encourages some more issuers to test the waters in coming weeks.

Leveraged Loans Primary

It’s also another quiet week in leveraged loans, as analysts continue to pick through the slim pickings available. One buysider complained of “negligible primary” and “very weak markets.”

Our lone issuer is Optigroup, with a €515m TLB (B2/B/B+) and a €60m delayed draw TLB to be allocated on a pro rata basis.

The Swedish business, backed by little-known sponsor FSN Capital, finds itself in the middle of the raw materials inflation debate. Around two thirds of the business is dedicated to the supply of packaging materials and paper to businesses in Scandinavia.

In such a difficult market, physical bookrunners Jefferies and JP Morgan are leaving nothing to chance, currently offering E+525 bps and a 94-95 OID. One buysider agreed that this was incredibly generous for the rating, and suspected that OID might reach 96 in final pricing.

Nevertheless, there are serious concerns around the business, including geographic concentration and minimal potential organic growth. In addition, any kind of improvement to margins would have to come from price increases, suggests the buy side, which could be difficult to swallow in the current environment. Above all other issues however, is the little-known sponsor, according to the buy side.

So continues the drip, drip of issuance, and as lenders maintain their cool, according to market sources, the sell side has accepted that now is as good a time as any to get long-awaited underwrites launched.

As such there is a spate of deals in pre-marketing, including Morrison’s, though to some extent, the banks have likely been “pre-marketing” this problematic deal since late 2021. But in this environment, all banks have found themselves in a difficult spot. Due to the unstable market, where volatility has become commonplace for investors, pre-commits are considered too fragile to trust and could be considered an unreliable gauge of where the credit could price just weeks in the future, suggest sell side sources. Perhaps this is partly why Britain’s fifth largest supermarket chain has taken so long to launch.

The sellsider antidote for a confused and bruised market? Diversification of the investor base.

Bankers will continue to tap as many pools of capital, diversifying across euros and dollars, looking at loans where bonds are the norm and tapping private debt more than ever before.

Indeed, some issuers have already fallen prey to the certainty of execution on offer from direct lending, despite the higher cost of capital, which can typically reach up to 9%, according to market sources.

One such borrower is Corden Pharma, the contract development and manufacturing supplier recently acquired by Astorg. The business, which was rumoured to be valued at up to $2.6bn according to Bloomberg, has opted for a unitranche deal, according to market sources.

It’s hard to imagine an asset as large as Corden opting for direct lending, when this time last year, the likes of Advanz Pharma, despite its chequered history, managed to price a €305m TLB at E+500 bps, alongside a series of bonds. Sources say this is because of a potential over reliance on revenue from components made for the Moderna Vaccine, which the market expects to decline in the coming years.

Private debt eating into the syndicated debt space is a well-covered topic, and one that the 9fin team has covered out of the US recently, but it's likely the importance of direct lenders will continue to grow, especially as these difficult conditions continue. Otherwise, banks continue to underwrite deals, though not to the ravenous standards they were holding up in 2021.

High Yield Secondary

The iTraxx Crossover continued its ascent but at a slower pace than last week, closing on Thursday at 460 bps (+7 bps on the week). Fund outflows continued, with European HY corporate bond funds losing another 0.86% of AUM on the week, down 12.35% YTD.

Instruments tracked by 9fin were down slightly on the week by an average of -0.16 pts. Investors seeked cover in the defensive Utilities (+0.26 pts) and Consumer Staples (+0.21 pts), with Consumer Discretionary (-0.35 pts) and Financials (-0.41 pts) both underperforming.

Greek construction company Ellaktor was one of the big movers on the week. Last Friday (6 May), RB Ellaktor Holding B.V. announced a tender offer for all common registered shares with voting rights in Ellaktor S.A. RB Ellaktor is a subsidiary of Reggeborgh Invest B.V., who already own 30.522% of Ellaktor’s shares and voting rights, with the tender offer applying to the remaining 69.5%. To complicate matters, on 6 May Motor Oil also acquired a 29.87% stake in Ellaktor S.A., later confirming it will not tender its shares in the public offer.

The most obvious implication of the tender offer is a Change of Control trigger on the bonds - as 9fin’s Christine Tognoli discussed in her analysis of the transaction, if Reggeborgh’s tender offer is successful and it acquires the outstanding shares in Ellaktor (other than approximately 30% held by Motor Oil), or at least increases its shareholding in Ellaktor to above 50%, a Change of Control would be triggered. The Notes rose ~8 pts to 97.875 on the announcement, shy of the 101 Ellaktor would be obliged to pay should their shareholding rise above 50%.

The key reason for where the bonds sit appears to hinge on the sale of Ellaktor’s RES arm, for which an agreement is in place, with the unit making up over a third of group EBITDA. The sale would involve the RES arm transferred into a new company, which has its own implications on Asset Sales and Restricted Payments covenants - specifically, potentially requiring Ellaktor to reinvest the proceeds or pay down its debt.

Leveraged Loans Secondary

Markets continued on their downward trend this week, across all sectors, once again highlighting the opportunities available to PMs.

Our biggest faller is ATM producer Diebold Nixdorf, and this won’t come as a surprise to anyone on this week’s earnings call for the business. Revenue has fallen 12% for Q1 22 compared to prior year, with just $9.4m of adjusted EBITDA down from $100.3m. The US-headquartered business has also announced a big downward revision of revenues, EBITDA and free cash flow for 2022.

Its $384m TLB paying L+275 bps has dropped almost ten points this week, while the €350m TLB paying E+300 bps has dropped 8.3 pts. Both TLBs now trade in the low 80s and mature in November 2023.

Supply chain disruptions globally have impacted Diebold’s efforts in converting order backlog into revenue. Rising input costs have also put a strain on margins, forcing management to take a more proactive approach at discussing repricing with customers, or suggesting the pre-payment of orders.

A business restructuring plan has been launched, to restore profitability to prior levels, with estimated cash cost of $75m over the course of 2023/24. The company has also enlisted Evercore and Sullivan & Cromwell to advise on options to deal with its upcoming maturity wall. See our fall report on the earnings call here.

Following closely behind is Wittur, with a €530m and €55m TLB, each paying E+450 bps and E+ 400 bps, respectively. Both tranches have dropped around 5.5 points this week, following concerns around the manufacturing business’ exposure to the Chinese market, according to two buysiders. While the tranches are now indicated in the mid-80’s, lenders aren’t calling this a distressed situation just yet, despite high leverage and weak, falling EBITDA.

Our biggest upward mover by a healthy margin, was Comdata with a four point increase for its €355m TLB paying E+500 bps. The TLB, which is now indicated at 69, matures in May 2024. In April, the customer experience business announced it was to be acquired by Spanish ICG-backed competitor Konecta to form a company with around €2bn in sales and €300m in EBITDA. One ratings agency has been positive on the merger: S&P put the CCC+ rated business on credit watch positive on 26 April.

On Reconnaissance

On the ESG side, 9fin has noticed that more and more investors are raising the possibility of a change in attitudes towards defence spending. Some lenders are suggesting that weaponry most ESG-focused investors would have baulked at last year, is now being considered as “defensive” given the current situation. This is a stark turnaround from as recently as Q4 of 2021, when defence issuers feared “becoming pariahs of the investment world,” due to accelerating ESG trends, according to the Financial Times.

Defence companies aren’t prolific in EHY, though Ultra Electronics does have some revenue from the defence industry. The company has actually had the converse reaction to this trend, with its loan pricing declining ever so slightly since 2021, but 9fin will continue to watch this space.

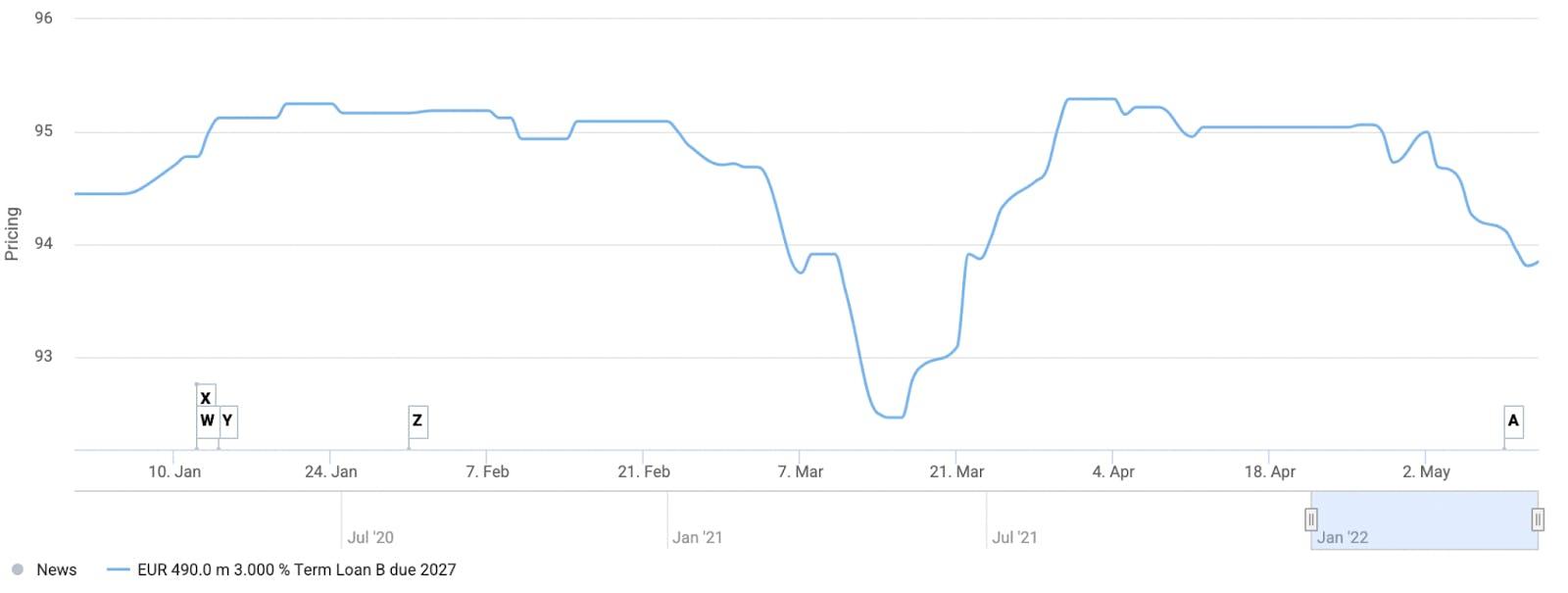

Aernnova, another HY name, manufactures parts for the likes of Airbus, Boeing, Bombardier and Embraer. The credit has also coasted through 2022 and its €490m TLB paying E+300 bps is now indicated at 93.8.

Other defence and aerospace businesses in the HY universe to watch out for as defence budgets begin to look more and more healthy include ITP Aero, Leonardo and Bombardier itself.