This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

LevFin Wrap - Investors picky as pipeline offers promise

Huw Simpson

+Michal Skypala

•12 min read

High Yield Primary

A ‘week is a long time in politics’ Harold Wilson famously said, and doubtless even he would appreciate just how quickly sentiment can shift in today’s European capital markets. There’s a slight pause in issuance this week as both issuers and investors take stock on what’s been a (briefly) manic spree. Just two new real names to report, with Aggreko and Polynt offering fresh supply in a choppy market, while Iliad extended its bookbuilding into this week.

My Generation

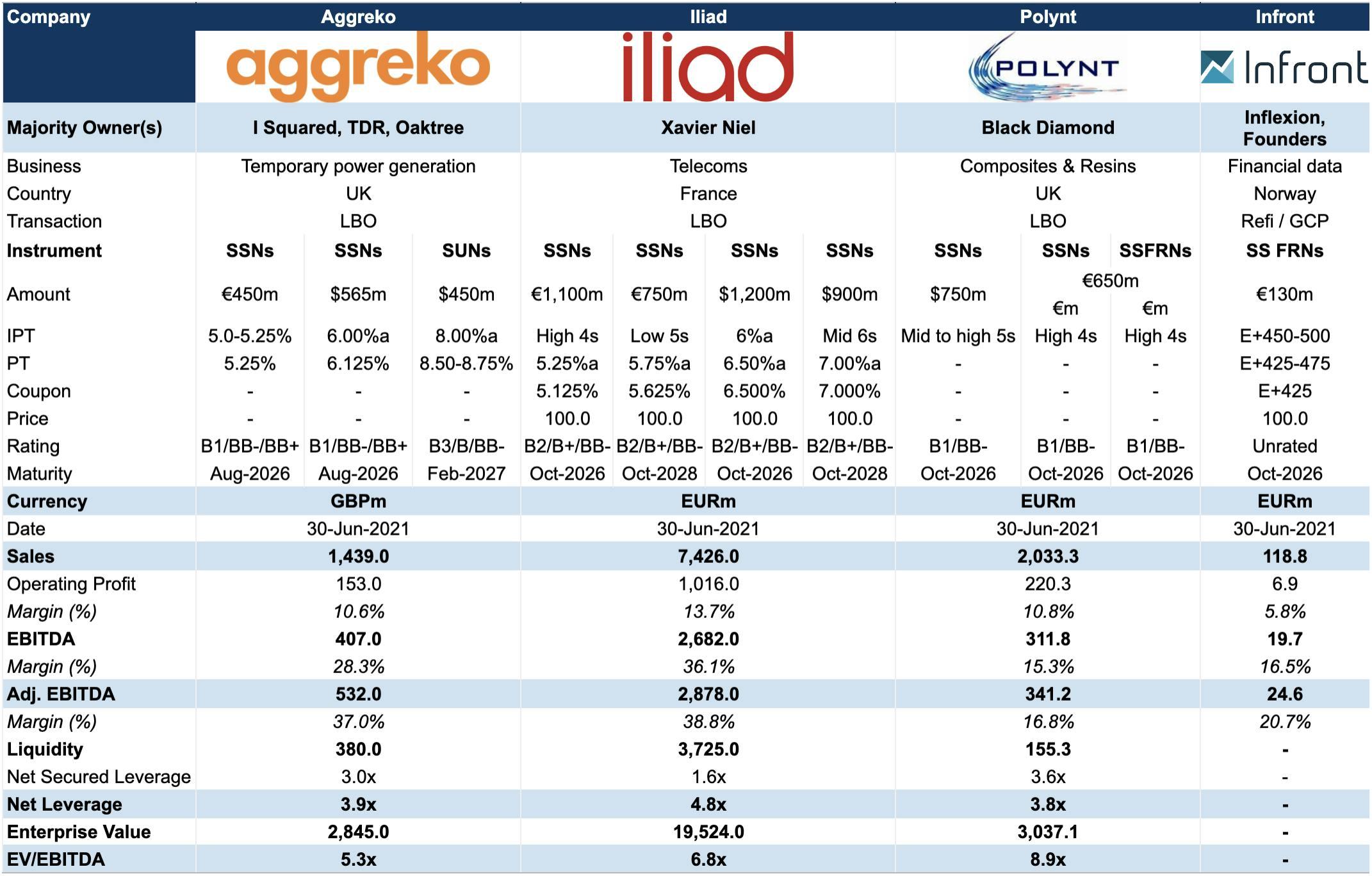

Portable power generation group Aggreko is funding its acquisition by I Squared and TDR with £700m (equiv.) of Senior Secured Notes due 2026, a £1,000m (equiv.) TLB - each split across dollars and euros - and $485m in Senior Notes due 2027.

Alongside a £70m RCF draw and £90m of cash on balance sheet, the two sponsors are injecting £699m in equity, with Oaktree providing an additional £93m via the TopCo in proceeds from preferred equity. Together this places an EV of around £2,845m on the company, an EV/EBITDA of 5.3x, and a slender equity cheque of ~28%.

While legals were fairly moderate compared to recent sponsor transactions, we might question some of Aggreko’s ESG credentials. The company's own definition of a “net zero target” doesn’t align with the widely accepted definition of the term, as it excludes scope 3 emissions (those emissions generated in the use of it’s products). In 2020 Aggreko moved end use emissions out of scope 2, and into scope 3 - so as a result, scope 3 emissions now make up 99% of total emissions. This is unambitious and lags its leading competitor, Cummins.

Reception hasn’t been wholly positive to the somewhat cyclical B1/BB- credit. Pricing on the loans has already pushed out from E/L+425-450 (99-99.5) to revised talk of E/L+500-525 (98.5), and IPTs on the bonds are currently offering a chunky 5-5.25% and 6% across the secured euro and dollars, the unsecured sent out IPTs in the 8% area yesterday. A price update sent out this afternoon reaffirmed the wide end of IPTs, at 5.25%, 6.125% and 8.50-8.75% respectively. You can read our deal preview here, courtesy of 9fin’s Owen Sanderson.

Black Diamond doubles down

In an all secured offering, specialty chems group Polynt was out with €650m (equiv.) in Euro fixed and floating notes, alongside a $750m fixed tranche to fund Black Diamond’s acquisition of the remaining shares in the group. Previously 50% owned by Investindustrial, an €85m equity contribution and €345m of cash on balance sheet will also fund the cash consideration, as well as fees and repayment of existing debt at the target group.

With a focus on composite resins and coating technologies, Polynt’s end markets span from building and construction, to wind energy and the marine sector - supplying a protective layer to worksurfaces, turbine blades and boat hulls - among many applications.

Legals on the deal included EBITDA add-backs (permissible cost savings and synergies) capped at 25% and a 24-month time limit, Issuer election of whether or not to apply IFRS 16, and the welcome presence of a J. Crew blocker.

IPTs were sent out at Mid-to High 5s on the dollar tranche, and High 4s on the euros. Meetings end today (15th October), and pricing is expected next Tuesday (19th October).

Long song of Ilium

Extending the group’s bookbuild to Wednesday, Iliad became the second firm to concede a host of doc changes in as many weeks. Notable changes include a cap on EBITDA adjustments, the inclusion of a minimum 75% cash consideration on asset sales (this is present in all but the more aggressive deals), and dropping the so-called “super-grower” concept (high watermarking of basket sizes) - you can read our original Legal QuickTake here.

Tranche sizes shuffled toward the shorter tenor across both currencies, with the initial €1,000m and $1,000m 2026s boosted to €1,100m and $1,200m, while the 2028 trimmed from €900m and $1,000m to €750m and $900m.

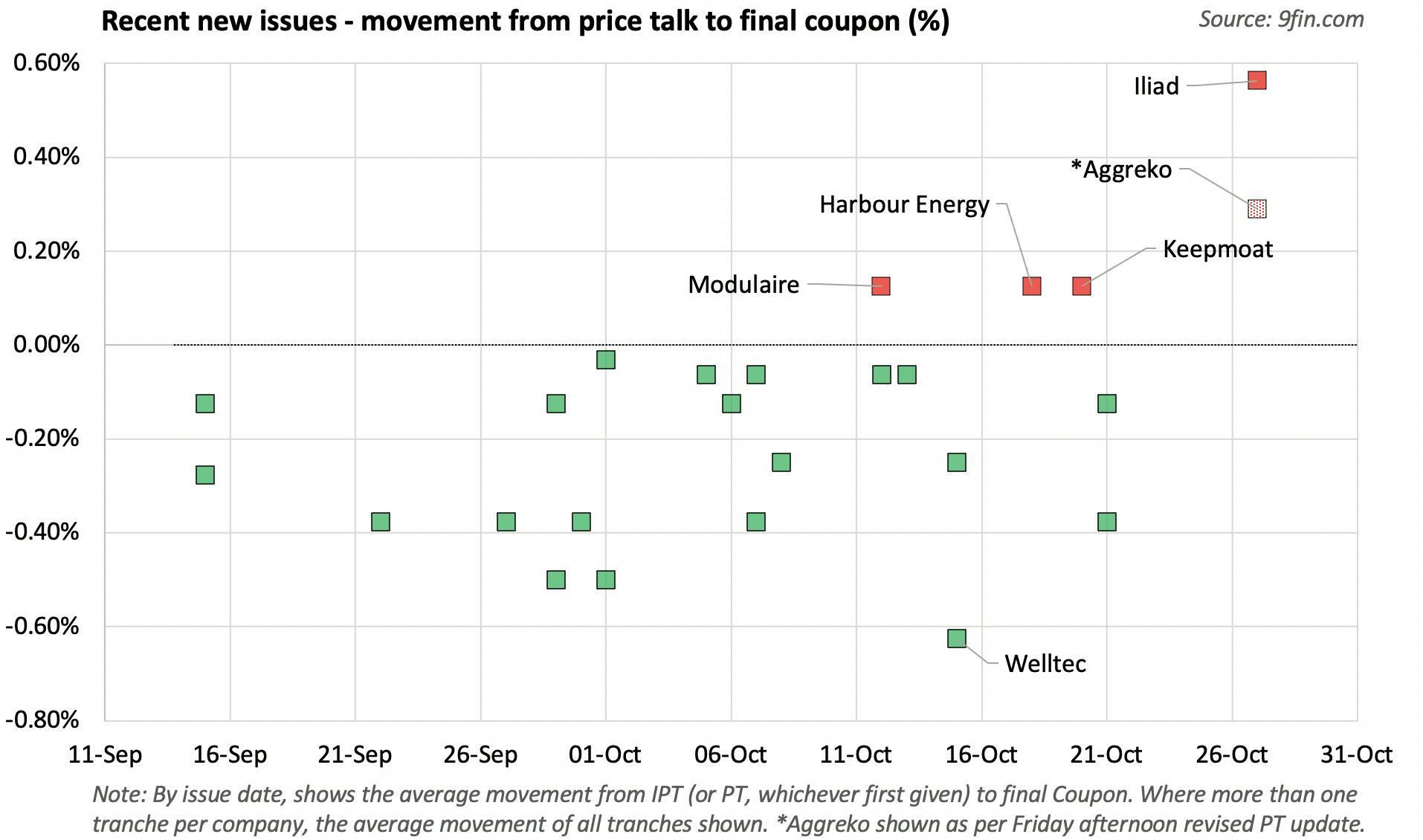

Pricing also widened dramatically with Price Thoughts sent out on Tuesday (12 October) showing around a 50 bps increase on IPTs across all four tranches. The Euro’s launched at the tight end of revised price talk, while the dollars held firm. Since issuance however, the notes have all traded strongly - the euro 2026 and 2028s have since lept to 103.1 and 103.7.

And elsewhere, Nordic financial market data and ‘information solutions’ group Infront printed €130m Senior Secured FRNs due 2026 (unrated). Final pricing emerged at E+425 bps (par), down from IPTs of E+450-500 bps. Proceeds will refinance existing group debt and for general corporate purposes - including repayment of the bridge loan and acquisitions. Sponsor Inflexion completed its acquisition back in June this year.

Ghoul or Glut? Fright or Flight?

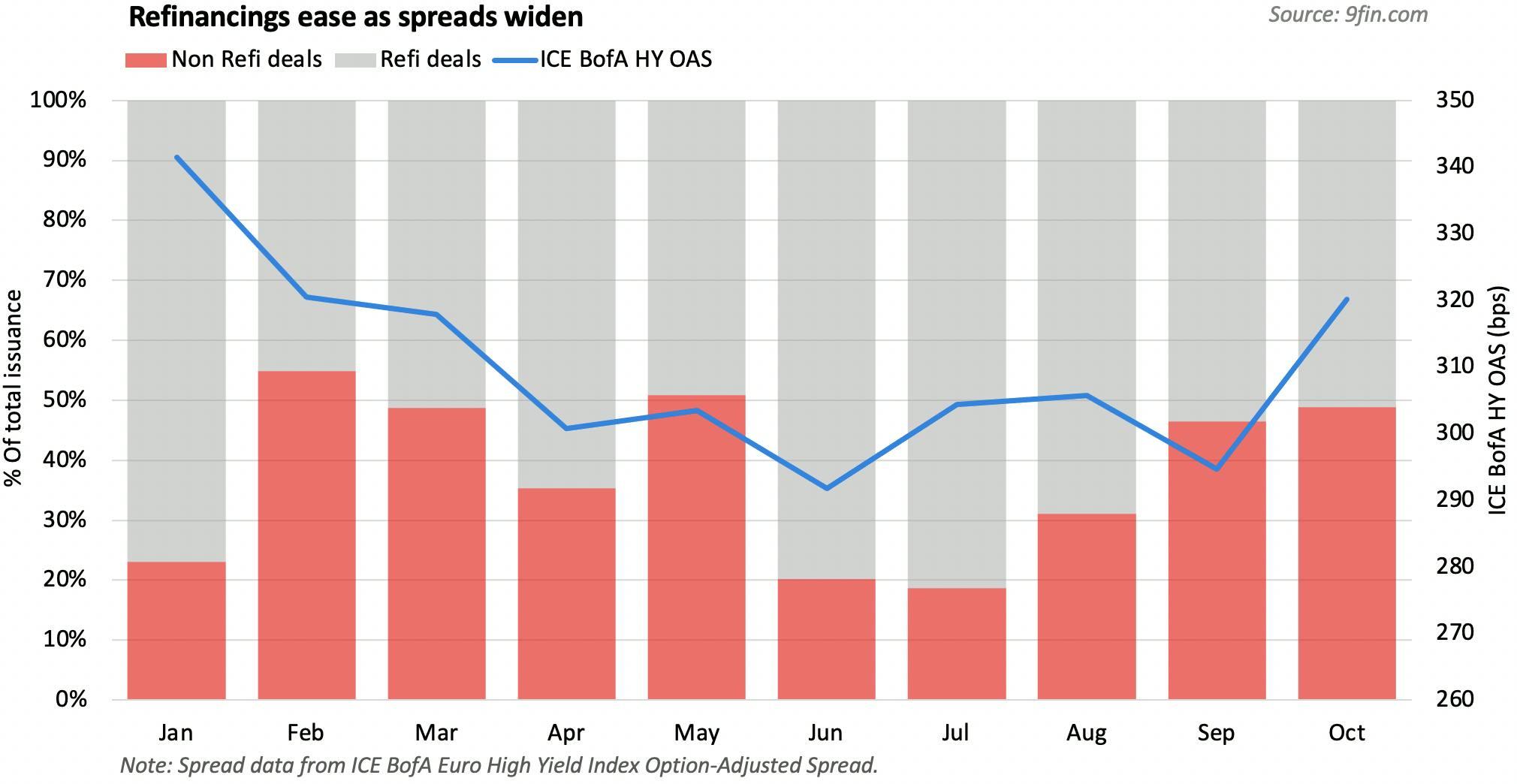

Back in mid-September, spreads in European High Yield tunneled to new post-Covid lows of ~285 bps. These have now retraced a little, with the ICE BofA HY OAS seen on Thursday at 325 bps. Meanwhile, credit funds have seen further outflows this week, with Global HY and US HY tracking -$226m and -$114m each. Euro HY funds have had the worst of it, with -$309m in outflows this week, bringing the total to -$696m in the last fortnight.

A few reasons have been cited, from a new supply glut, which has taken the edge of investor hunger, to poor recent performance on certain names, and of course wider macro-inflationary fears. Together, these have pushed some new issuers back on pricing during the bookbuild, with Iliad and Modulaire both forced to widen pricing over initial thoughts, and make significant doc changes.

Interestingly, this goes further, as either due to the well marketed M&A pipeline, bankers preference to de-risk, or simply wider spreads eating into any cost savings, most opportunistic re-financiers have kept away from the market.

However, it’s not over yet - conditions toward the end of the week appear to be improving once again, with the iTraxx Crossover tightening back to 256 bps today, after reaching above 270 on Tuesday - it’s highest level since March.

Leveraged Loans Primary

Beggars turned to choosers as loan investors have the biggest selection to pick from in primary since the market reopened in September. Buysiders finally feel like the belle of the ball deciding swiftly which suitor is even worth the effort of due diligence in a crowded market.

“We are not stretched to play anything with high risk and that is felt in the market. Everyone knows by now that they had a good year so we are not eager to deploy cash. I would not be surprised if some deals start to widen,” said one CLO analyst.

And we are not slowing down as it seems banks are trying to get deals off their balance sheets in a benign environment before the half-term holiday hits the UK at the end of this month.

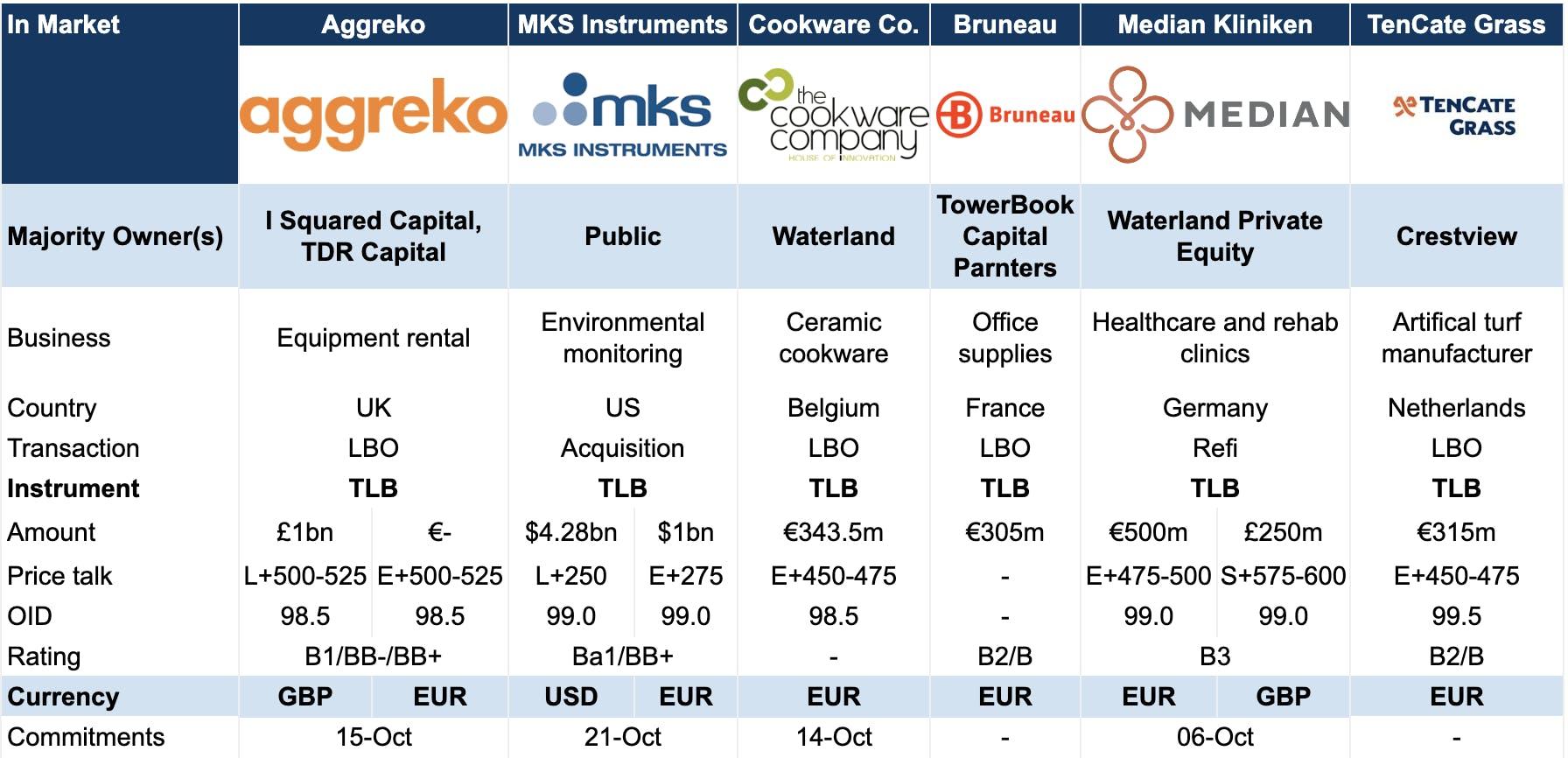

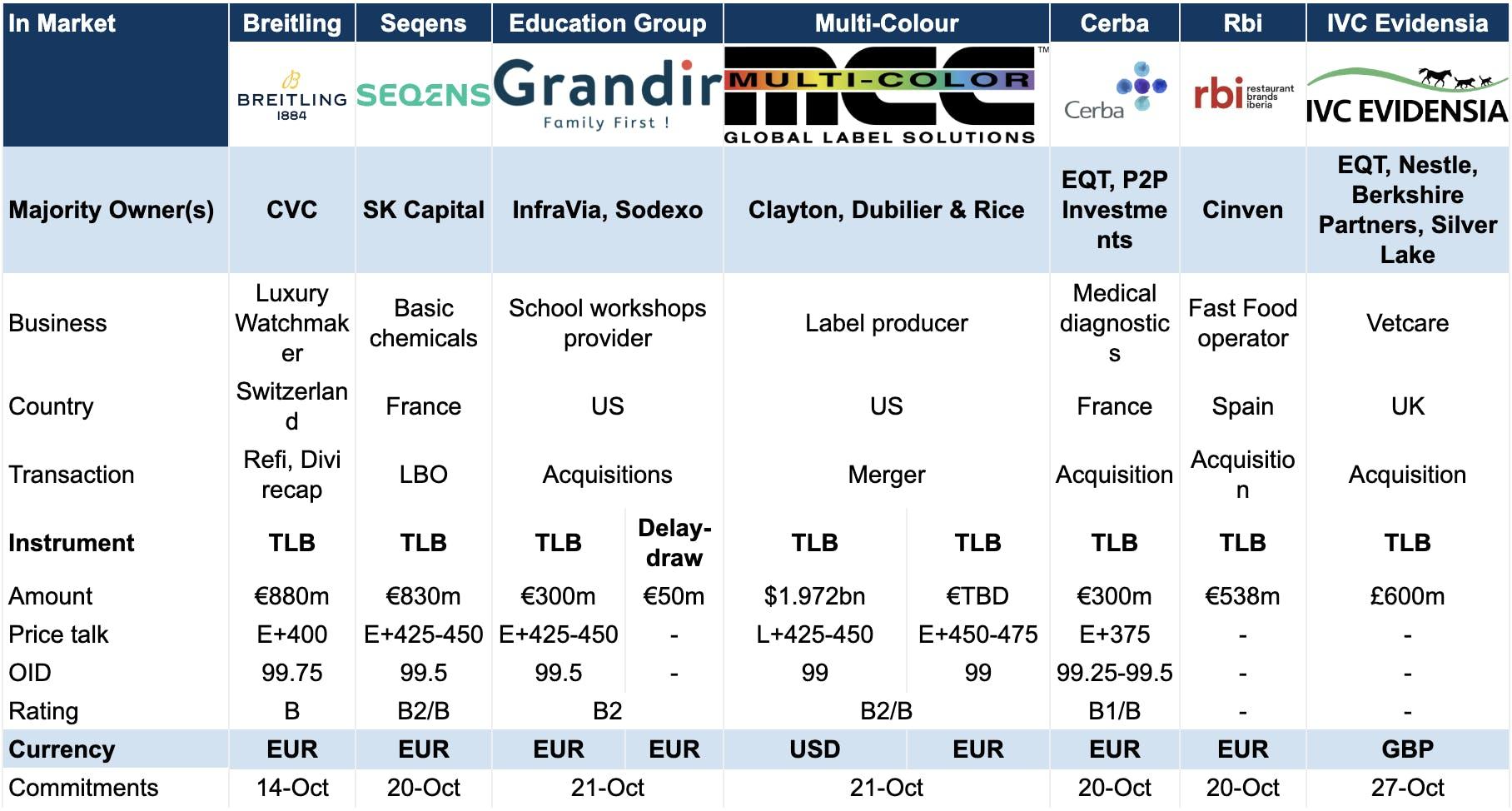

Four new deals launched this week. Most of the names are LevFin usual suspects, with French media diagnostic firm Cerba offering a €300m TLB with price talk at E+375 and 99.25-99.5 OID, US label producer Multi-colour plans to price $1,972m of paper split between $ and € tranches talked at L+425-450 bps and E+450-475 bps, both with 99 OID, while UK veterinary group IVC is bringing sterling paper with £600m TLB. Three new joiners are complemented by Spanish LBO as Burger King Iberia is looking to place €538m TLB.

Early signs of fatigue

The Primary Bonanza has 12 active syndications with still two of them - Aggreko, Breitling - still due to price today (15 October). Unsurprisingly with this slew of deals on buysider’s desks signs of indigestion are starting to show.

Forementioned UK industrial firm Aggreko felt the investors fatigue as it flexed price talk on the loans 75bps upward to get the deal through, as cyclicality risk and exposure to energy prices might have overcome the modest leverage and good cashflow management.

Question marks still remain about the future of Median Kliniken’s syndication that was postponed due to a planned TV documentary about the Priory Group and it does not seem to be the only deal that needs more digestion time. This week brought another delay, as the LBO debut by Belgian retailer The Cookware Company plans to price and allocate early next week even though the commitments deadline passed this Thursday.

In our preview investors expressed that The Cookware Company’s great lockdown performance even though complimented by a juicy margin could be all too-good-to-sustain, especially in a saturated and cyclical market with fairly low barriers to entry. “It’s asymmetrical, I probably want more than an E+450 bps margin to play there,” said one CLO analyst. “It was a tough one to turn down because it pays quite well,” a sentiment echoed by a second buyside analyst.

KP(bye?)

Even in a saturated primary there were still winners of the race if a strong credit supports the deal.

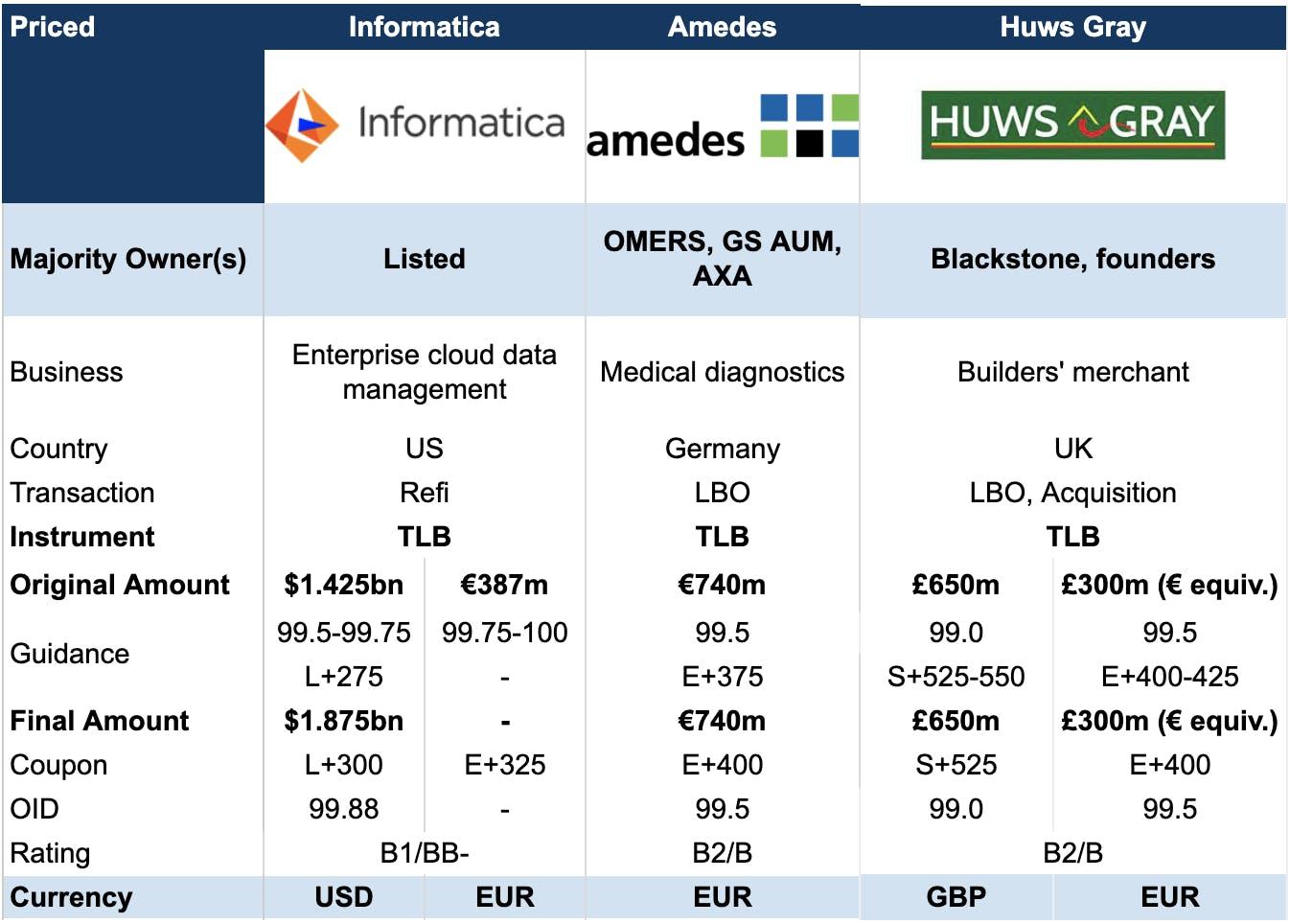

German diagnostics firm Amedes has priced its €740m 2028 TLB (B2/B) at E+375 bps and 99.5, cutting 25bps from initial talk. The deal was a blowout after a strong response from the buyside, with books twice oversubscribed, according to one market source, adding: “It’s the largest book on a loan deal we’ve seen since Titan.” The Netherlands-based tin food can manufacturer came to market with a €1.175bn E+375 bps 2028 TLB in July this year.

A tighter margin was a pain for some investors who still decided to play the deal but lowered their exposure. “That’s a bit tight for us on a credit that we weren’t terribly excited about, so we’re planning on reducing our offer,” said one buysider.

Even against an overfilled book investors stood their ground on the docs and their pushback axed the ESG ratchet which had two KPIs related to electric car use in Germany and reducing employee injuries. “It was an unusually small ESG ratchet to begin with - the kind of size you were seeing at the beginning of the year rather than now - and it’s strange to then see an ESG ratchet cut,” mused one buysider.

The ratchet was cut following questions around the appropriateness of KPIs, according to the market source, with a clean removal seen as the easier option over altering the KPIs given the relative slim size of the discount. Terms were also detoxed around the usual battlegrounds of margin ratchets and ticking fees that were toned down to market standards.

Divi watch

It would not be a week in the loan market without a dividend recap. This time Breitling has priced a reward for its sponsor CVC while still managing to tighten the €880m TLB to E+400 bps and 99.75 from E+400-425 bps and 99.5. A top tier sponsor, adequate deleveraging and strong rating helped the deal to push through a dividend, which has not been anything surprising in the history of the company. “We think B2 loans are offering adequate compensation at the moment, you’re seeing loans in this category paying in the 400bps-425bps area, sometimes up to 450bps,” said a portfolio manager at a credit investment firm looking into the deal.

US cloud data manager Informatica also sailed through syndication pricing $1.875bn TLB at L+275 with 99.88 OID, tightening from L+300 and 99.5-99.75 OID at launch. The €387m euro tranche was dropped in favour of the dollar issuance.

UK building materials supplier Huws Gray priced its £650m TLB (with £100m on delayed draw) on the tight end of talk at S+525 bps with a 99 OID and the £300m equivalent euro tranche at E+400 bps and 99.5 OID. Investors also received eleventh hour concessions on margin ratchet where the final terms reduced stepdowns and leverage, and shortened the ticking fee.

The company is a star performer in its sector but buysiders voiced concerns - worried it may be building on shaky ground due to macro considerations, including raw materials volatility and saturated demand for building materials sector issuance.

Primary stays motley and is yet to see if syndication remains unwrinkled for the deals left to price for upcoming week such as the French chemical firm Seqens, US school workshop provider The Education Group, French office supplier Bruneau and Dutch artificial turf manufacturer TenCate Grass.

High Yield Secondary

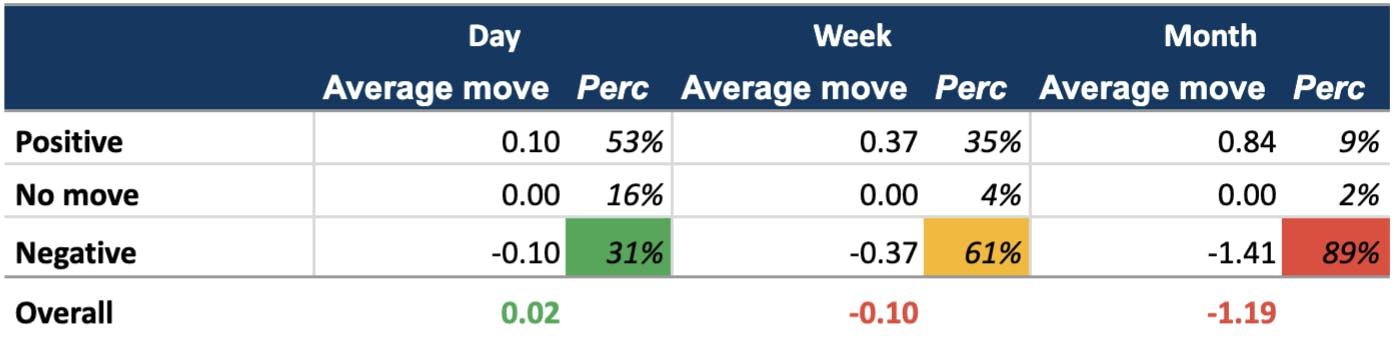

Across HY, instruments were down on the week an average of -0.10 pts (35% +0.37 pts | 61% -0.37 pts), but have rallied somewhat since mid-week. By industry, Real Estate was once again fared worst (-0.35 pts), although this is largely due to poor performance at Aggregate Holdings - while bonds at the AdlerGroup and Adler Real Estate level have recovered an average of ~3 pts. Consumer Staples (-0.25 pts) and Healthcare (-0.25 pts) also traded poorly, while Energy (+0.14 pts) and Communication Services (+0.02 pts) posted the only industry level gains.

Leveraged Loans Secondary

The secondary loan market has seen renewed activity in the fall after slew of deals in primary as portfolio managers make space for new offerings. “[Secondary] is in healthy condition, enough loans are trading away from the seller rather than going into other funds through cross trades,” said a CLO manager.

That was evidenced on a hefty BWIC arrival early in the week. Bids were due on Tuesday for a €215m-equivalent pool comprising close to 100 names, in a motley selection of some recent pricings, companies that are actively tapping the market at the moment, such as Breitling or Informatica, and tainted names like B&B Hotels, Hotelbeds or GTT Communications. According to 9fin holders data, the most likely seller was the CLO house Barings.

The largest ticket was €5.9m TLB from Finastra. The list included almost only TLB tranches. Exceptions were ordinary shares A from Tunstall, small portions of Ordinary B shares from AS Adventure, a €300k slug of senior secured 2021 notes from Galapagos and a €4.35m slice of Carlson Travel senior secured 2025 notes.

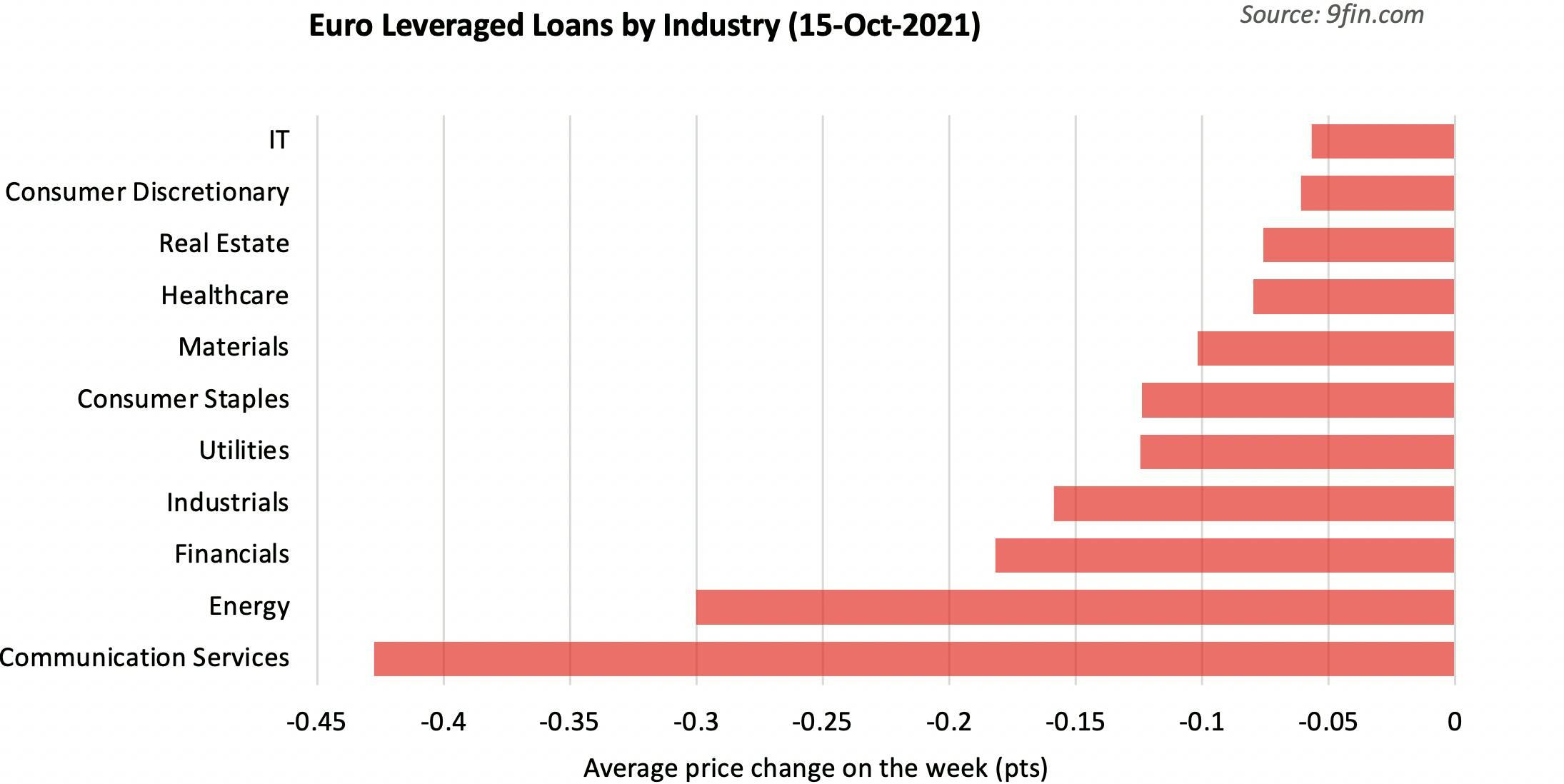

The wider market was fairly flat although mildly softened with all sectors slowly falling, with communication services and energy taking the biggest toll with 0.4 and 0.3-points respective decreases.

The strongest riser in a fairly uneventful week in the secondary trading was the Dutch lingerie retailer Hunkemoller which gained 2.4-pts (2.5%) to a 96.25 mid-quote.

French event organiser Comexposium was the biggest loan decliner this week, coming down 4.4 pts (5.3%) across all its three respective TLBs €114m, €483m and €355m to a 78.75 quote, after it announced last Friday that it has left the French safeguard process with the support of its shareholders.

Spanish wedding dress designer Pronovias has also seen its €215m TLB fall by 4.2-pts (5.8%) to 69.25.

We hope you enjoy this round up from across the leveraged finance markets. It was first published for subscribers and includes links to many features on our platform including company and bond information, pricing, loan previews, deal screening and source documents.

If you would like more information on any of the functionality available from the 9fin platform, please contact team@9fin.com