This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

LevFin Wrap - Old Bailey looks to put inflation behind bars

Huw Simpson

+Laura Thompson

•9 min read

High Yield Primary

Another week, another rate rise, another record set. Thursday’s 50 bps hike by the BoE was widely anticipated, although new forecasts of 13+% inflation by the fourth quarter of 2022 probably weren’t. It’s the largest Monetary Policy Committee hike since 1995, the largest ever since the Bank of England’s independence in 1997, and comes alongside projections of a five-quarter long recession for the UK.

As previously announced the MPC will also embark on Quantitative tightening, with the planned sale of gilts to follow shortly after the September policy meeting. Total stock under the Asset Purchase Facility (APF) stands at a beefy £863bn (or almost 40% of UK GDP!). Gilt sales are expected to be around £10bn a quarter for the next twelve months, which together with maturing gilts will reduce total stock by ~£80bn over the same period.

Frontrunner for next Conservative Leader, Liz Truss is reported to be considering a “review of the BoE’s [independence] mandate” according to Attorney General and supporter Suella Braverman. It’s a worrying – if not that surprising – development for the low-tax, high-growth candidate. Truss even believes a recession can be avoided entirely.

Meanwhile, the battle between growth and inflation continues. Poor economic data in recent months has driven expectations of a softer reaction from central banks. This is given as one reason for the recent “bear rally” among equities – with both the S&P 500 (+8.4%) and tech-heavy NASDAQ (+13%) up significantly this month. This optimism has been shared in Europe too, with the STOXX Europe 600 up +9.3% over the same period. And in credit, the iTraxx Crossover closed on Thursday at 519 bps, over 100 bps inside its mid-July peak, while the BTP-Bund spread holds steady at ~205 bps, inside recent peaks of 243 bps.

Alongside the BoE’s gloomy forecasts, several Fed speakers have stepped in to re-iterate that tackling inflation remains the priority – rate cuts are unlikely in 2023. A hot US jobs report on Friday showed NFP rose +528k in July (250k expected), and an unemployment rate down to 3.5%, suggesting the US economy may not be so close to a recession.

Earnings Picture

Elsewhere, European corporate earnings have shown some signs of resilience to inflation pressures. Pricing power for many firms has allowed the passing through of increasing costs, and for earnings reported since June, average EBITDA margins have actually increased 1.6% pts year on year.

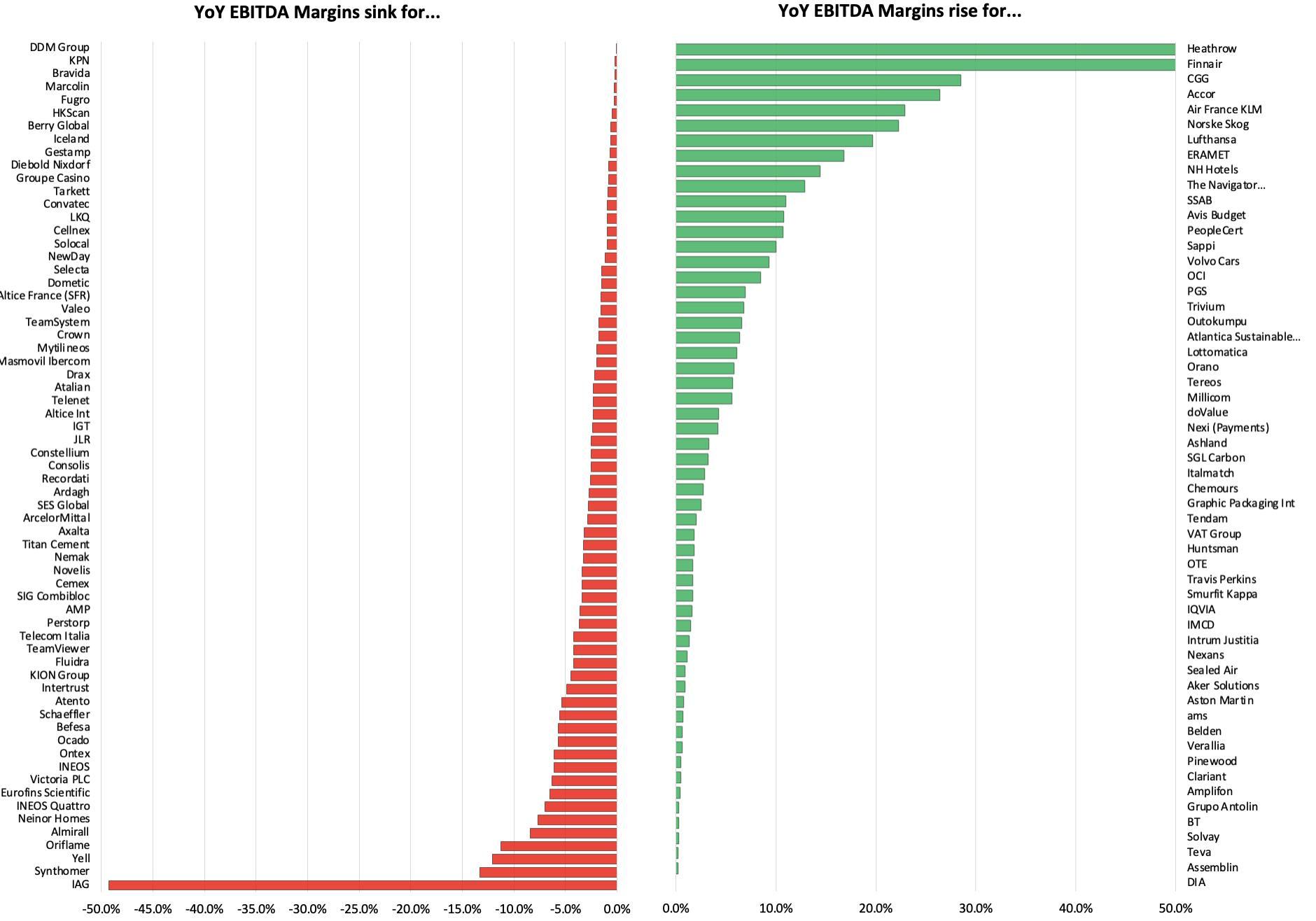

Across the 121 company sample, earnings reported since mid-July: average sales increased +36% YoY, EBITDA +114% YoY, and EBITDA margins by +1.57% pts. By median, Sales +18%, EBITDA +13%, EBITDA margins 0%. Axis trimmed to +/-50% points.

But this doesn’t tell the whole story, this comparison is slightly muddied by poor prior year results. For example, EBITDA margins are up across a number of transport names as pent-up demand fills increased capacity: e.g. Heathrow (+69%), Finnair (+61%), Air France KLM (+23%) and Lufthansa (+20%).

Another caveat is that we’re looking at reported, often adjusted, EBITDA metrics, which usually add-back permitted costs.

For other firms, such as those in paper and packaging, a global unbalance between demand and supply in pulp markets has been supportive of price increases, allowing price increases to offset the increase in energy and raw material costs: e.g. Norske Skog +20%, Navigator Co. +13% and Sappi +10%.

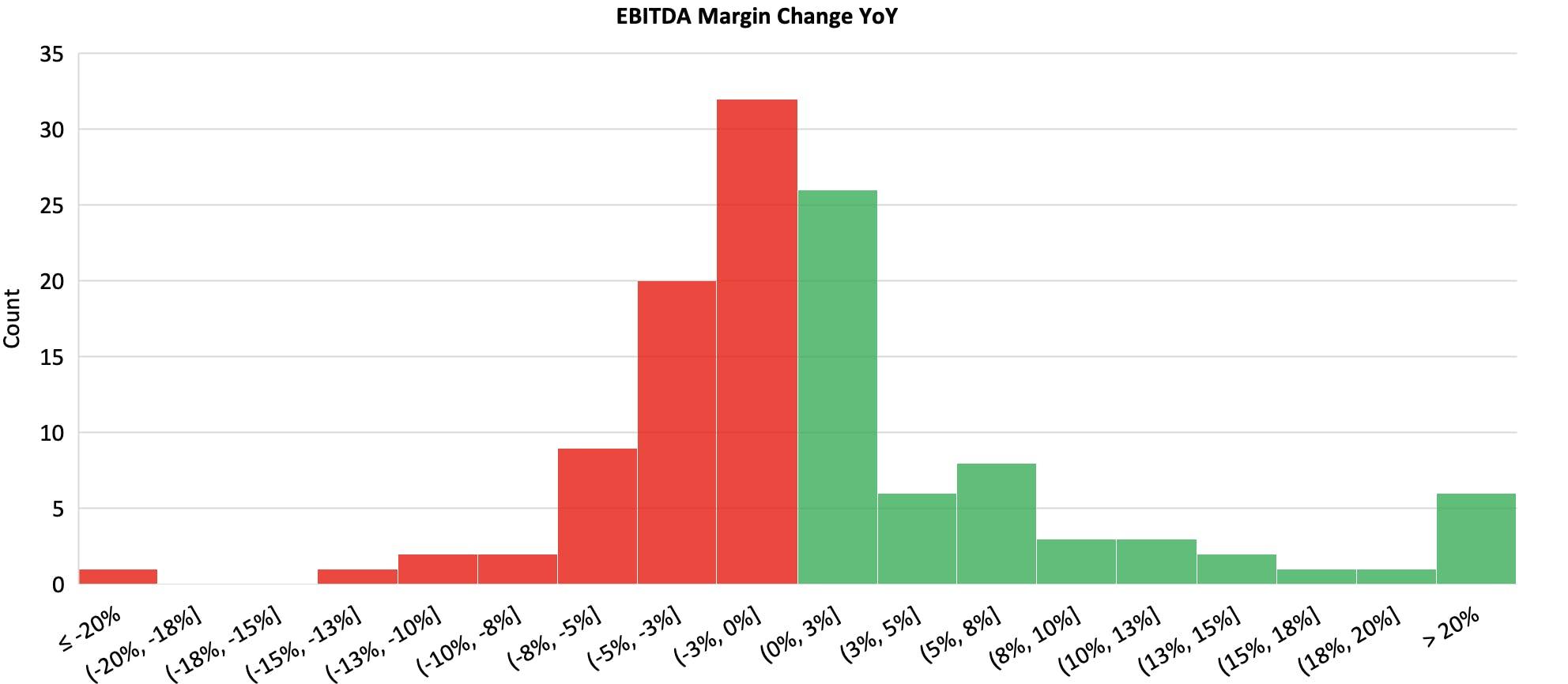

Looking closer, and ignoring the outliers, you can start to see margin pressure for many names. Across the sample of 121 names, 50 report EBITDA margin declines of up to 5 percentage-points, versus just 31 reporting up to 5 percentage-point gains.

YoY EBITDA margin change, in percentage points. E.g. a +5% point change would equal a change from a 10% to a 15% EBITDA margin

High Yield Secondary

In Secondary, prices gained an average of +0.62 pts this week (71% +1.1 pts | 26% -0.67 pts). By sector, Financials (+0.86 pts), Industrials (+0.84 pts) and even Energy (+0.83 pts) made the greatest gains, while the more defensive Real Estate (+0.21 pts) and Consumer Staple (-0.03 pts) fared worse.

Data from BofA and EPRA Global show limited fund flows as we enter the first week of August. Global HY funds registered a -$16m outflow, US HY a +$34m inflow, and Euro HY a slightly larger -$151m outflow.

Among single-name moves, Aston MartinSSNs have slipped -4.3 pts on the week, last seen at 101.8. All tranches of the supercar makers debt jumped in mid-July following news of an equity raise, of which roughly half is expected to go towards debt repayment – although as reported Chairman Lawrence Stroll wasn’t exactly clear on which tranches would be refinanced, only that it should save £30-40m of annual interest costs.

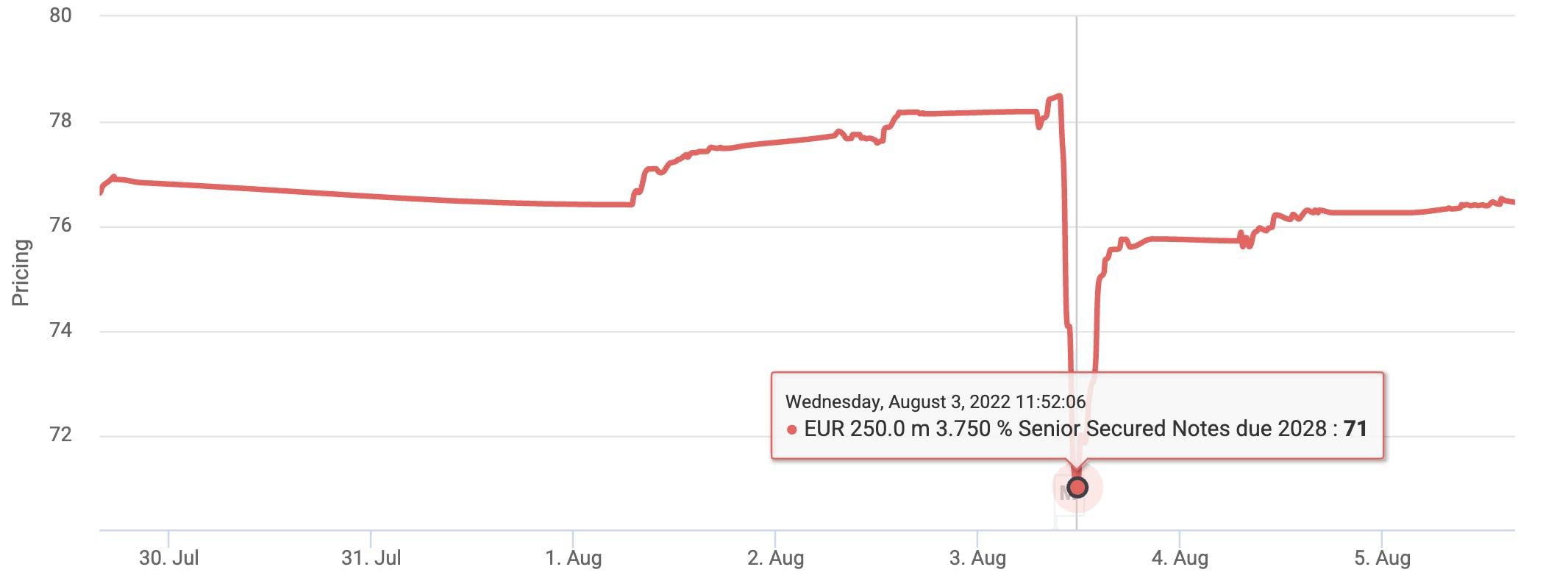

On Wednesday, Victoria PLC, producer of “innovative flooring products” came under a short-seller attack from Iceberg Research. The 2026 and 2028 SSNs promptly dropped -7-8 pts, before recovering around half the losses. Robert Smith at the FT reports.

Victoria PLC, SSNs due 2028

In more positive moves, Diebold Nixdorf, the US-based ATM manufacturer and service provider recorded a “strong relief rally” according to 9fin’s Ben Hoskin, after Q2 earnings on Tuesday. Full year revenue guidance was reduced for the second quarter running, but EBITDA guidance remains unchanged with management confident on cost savings to offset the topline hit. The 2025 SSNs are up +6 pts on the week.

And good news for holders of BestSecret’s recent €315m (+€35m) SS FRNs due 2027. Pricing at an OID of 85 a fortnight ago, the notes gained another +3.8 pts this week, last seen today at 94.6.

Leveraged Loans Primary

More downtime this week as the market, already subdued, finally settles into the August lull. Unlike in years past, August will be less of a welcome respite and more of a continued silence for many in the market, though hopes are high for a turnaround come autumn.

“There’s a decent amount of stuff being pre-marketed, Healthcare and Services names, so we’re hopeful that supply will be healthier come September now that we’ve had some CLOs print in recent weeks,” said one buysider.

This is the crucial difference between the coming September and previous dashed hopes of a market return post-Easter, two buysiders say. Recent prints including those from Alcentra, CSAM and Bain have been competing over similar credits in ramp up, but will soon provide much-needed demand for companies hoping to come to market after months of CLO drought.

“We also need some primary supply at the moment to get people moving stuff out of their portfolios and starting some market liquidity up again,” a third lender added. “Everyone is sitting on what they have and execution is still sluggish, so hopefully this will jump start things.”

It remains to be seen how the market will receive these upcoming names and what the ongoing role of private credit will be in getting deals across the line. “I’m expecting that any larger syndicated deal will need to be cut in a way that takes some pressure off the CLO shops — TLAs, second liens, ways to slice and dice to get leverage to appropriate levels,” said the first buysider.

The only pockets of activity this week include French telecom equipment distributor ETC Group (B2/B), who added a last-minute €475m tranche and downsized the dollars on its $989.8m-equivalent TLB backing an LBO by Cinven. The euros came in high at E+625 bps and 92 OID, with two step-downs at 4.75x and 4.25x net leverage on the first lien.

Some US buysiders looking at the deal had previously admitted they struggled to see a reason to take on an unknown European name, which could have driven ETC to slim its dollars from €972.4m-equivalent to €525.9m-equivalent. Read more here.

Finally, Belgium-based Gaming1 wrapped up a €306m TLB at E+525 bps and 91 OID (from 95 guidance) today. As reported, the deal struggled to find a home with lenders and was mulling the private debt markets. The name primarily suffered from its controversial sector, with investors reluctant to sell out of other, more familiar Gaming names (888, Flutter) to make room for this one.

“We’ve been wanting to sell out of some of our existing gaming stock for a while anyway and struggling to do so, so selling out of another name to make room for this one just isn’t realistic,” said one analyst looking at the deal. “You have to be selective about what you put forward in this sector because there is perennial regulatory risk alongside the ESG angle.” Read a full preview of the original deal here.

Leveraged Loans Secondary

Loans rallied in Secondary this week, up between +0.7 pts (Consumer Staples) and +1.7 pts (Real Estate) across sectors tracked by 9fin. Buysiders are buoyant on these slight signs of recovery, hoping it helps to clear the cobwebs of risk-off attitudes, as a fourth buysider reported.

Some of the largest movers include food processes equipment manufacturer Duravant, Ireland-based Jazz Pharmaceuticals and Spanish theme park operator Parques Reunidos. These names rose +5.8, +4.3 and +3.7 pts respectively this week — Jazz on positive Q2 results.

At the other end, long-beleaguered Arvos Group fell -5.5 pts to 67 on its €130m 2023 TLB after releasing 2021/2022 results this week. Revenues came in at €260m, with EBITDA up 25% YoY and adjusted EBITDA margin at 19%.

Others in decline included French fine foods company Labeyrie, which has continued to miss

budget in recent months in the face of rising input costs, as reported, down -3.4 pts on its €455m 2026 TLB, now just clinging onto the 70s at 70.8-mid.

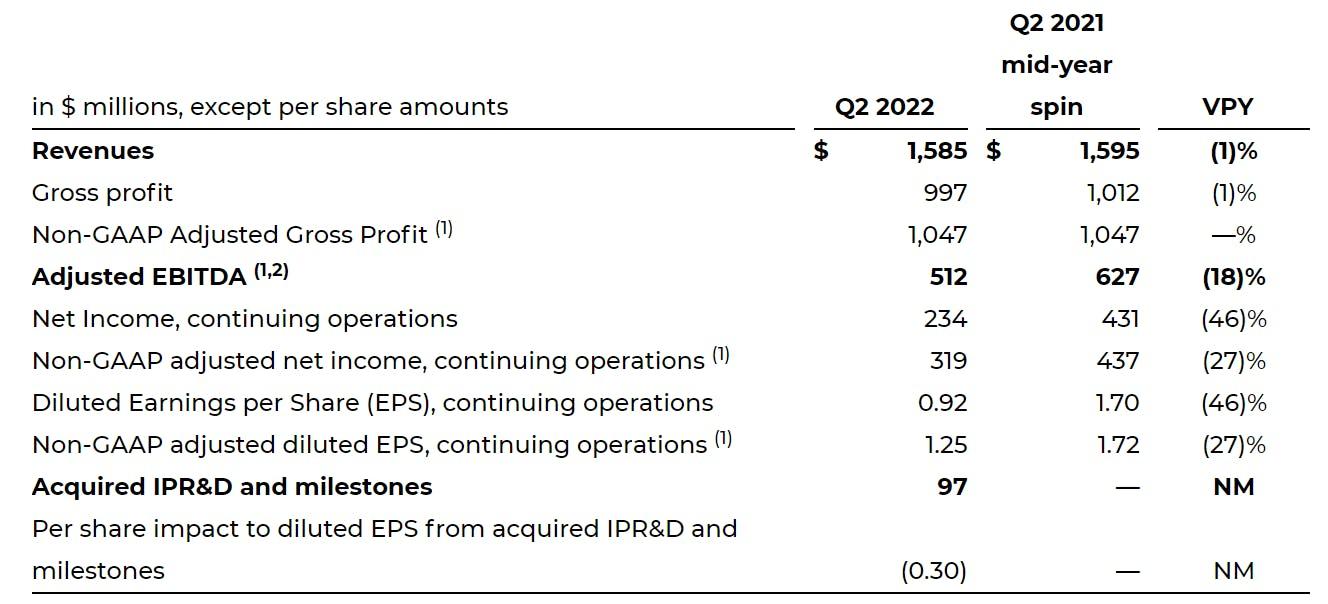

In this weeks earnings, over in the US, Organon reported a -18% drop in adjusted EBITDA from $627m to $512m on $97m of R&D spend, related to the biosimilar transaction with Shanghai Henlius Biotech. FX headwinds, with around 80% of Organon’s revenues coming from outside the US, also weighed on results.

“I’m reasonably alright with ascribing EBITDA loss to the reasons they gave given that margins were fairly robust,” said one lender. “The news around women’s reproductive rights in the US is going to be supportive of long term contraception, too, and the worst of loss of exclusivity impacts were last year.”

Gross margins held up at 62.9% versus 63.4% last year, while adjusted EBITDA margins fell from 39.3% to 32.2%. Organon’s golden goose, contraceptive implant Nexplanon, grew 8% ex-FX in Q2 on volume growth outside the US, but Nuvaring, hit by generic competition, declined 18% ex-FX in the second quarter of 2022 compared with the prior year period.

Leverage trended -0.1x of a turn lower to 3.5x, though management on the call said they remained open to transformative acquisitions once on the Merck spin out has been digested: “We’re not on the hunt for them but we are planning for their possibility.”

Organon Q2 2022 results

Elsewhere, French food companies remain lean. This week, 9fin revealed organic foods company Ecotone (Koninklijke Wessanen) had once again missed its budget in May 2022. EBITDA for the month skimmed its budget of €10.7m, coming in at €7m, while YTD EBITDA was also around €10m behind at €29.9m. Leverage came in at 6.2x on €505.7m total net debt, roughly flat on April’s 6.1x, and up from 5.1x at the start of 2022.

“Contrary to the likes of Biscuit International, raw materials are a bit more diversified for Ecotone and the margins are also higher, however this is still a tricky situation,” said the third buysider. The earnings misses have put pressure on margins, the buysider went on, but remains “far from being comparable to Biscuit International or Cerelia where there’s been a huge crash on margins.”

Lenders also question whether customers will stick with higher price point organic foods during a cost of living crisis, though they acknowledge organic and plant-based foods are an attractive focus long-term. Its €380m 2026 TLB is currently at 84.3 points. Read more here.