This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

LevFin Wrap — A quintet of high-yield bond issuance; Italmatch yield entices investors

David Orbay-Graves

+Laura Thompson

•7 min read

The 2023 secondary market rally is showing little sign of slowing, providing fertile ground for new issuance to come to market. The iTraxx Crossover index tightened a further 15.25bps on the week, and is marked at 413bps at time of writing.

Thursday’s closing print of 409.75 bps was the tightest close for the index since April last year.

Eyes are now likely fixed on a slate of central bank decisions scheduled for next week, with the US Fed, ECB and Bank of England all set to announce rates decisions next week.

With this supportive market backdrop, overall bond issuance in Europe is having a record-breaking January, according to Bloomberg, with more than €240bn in bonds sold this month so far – beating a previous record for January issuance in 2020.

Activity in the high-yield space specifically isn’t letting up – with deals from iQera, Italmatch, ZF Group, Kiloutou Group and Verisure all pricing this week. One levfin banker told 9fin that, as a conservative estimate, their shop expects €45bn in high-yield issuance this year, and €34bn in leveraged loans.

Bonds in particular are a “compelling product” right now, according to a second levfin banker, who noted that issuers’ leverage point has come down a lot from their cheap-money era highs. The real constraint for sponsors looking to issue now comes from the fixed charge cover ratio rather than EBITDA leverage, the banker continued.

The tone in the market is constructive, the first levfin banker agreed, with signs of “green shoots” after last year’s bloodbath. But while macro concerns are abating, private equity is expected to do fewer deals in 2023 and investors are becoming more selective. “The year will be driven by fundamentals and active management,” the banker said.

What large cap M&A activity there is will likely be H2’s business, said the second banker. Seller expectations have not reset to reflect the new dynamic, the banker said, adding that they’ve seen relatively few underwriting requests for LBO activity. Nonetheless sponsor-backed activity is expected to ramp up over H1, with some encouraging early indications already.

The first banker agreed – suggesting now is not the time for M&A. “Why are you selling a company today? Will those valuations be where they should be?”

This slowdown is further spurring A&E activity, as sponsors do not want to exit in the current environment, the banker said. And the absence of a buoyant IPO market further reduces the avenues to exit.

Ital-Match Made In Heaven

Bain Capital-owned Italmatch priced Thursday (26 January) its €300m 10% SSNs and €390m E+550bps SSFRNs, both due February 2028, at par and 94 OID, respectively. The issuance refinanced the company’s outstanding €650m E+475bps SSFRNs and RCF drawings, as well as to fund some cash on the balance sheet.

Perhaps indicating the extent to which the new issuance market is moving back in issuers’ favour, the deal managed to tighten considerably from early indications – albeit from a very generous starting point.

Whispers on the deal were circulated around the 11% area for the SSNs and E+575bps at 92 OID for the SSFRNs earlier this week, according to two buysiders. By the time initial price thoughts were released, that had already tightened to 10.5% area for the SSNs and E+550bps at 92-93 for the SSFRNs.

Despite tightening considerably, the first buysider said these levels offered ample upside. At 11%, the investor said they would have “taken it in spades”.

Potential comps flagged in 9fin’s Credit QuickTake include Arxada, CABB, Caldic, IGM Resins, Kronos Worldwide, Nobian, Polynt-Reichhold and Solenis – all of which trade at YTMs tighter than Italmatch’s new deal.

Indeed, the fact the new bonds looked “super cheap” raised some nervousness, especially at the whispers level, the first buysider said. The deal looked almost too good to be true, prompting a hunt for lurking downside risks.

The deal was marketed on 3.9x net leverage at €162m adjusted EBITDA, though a second buysider suggested that leverage in the 5x area is more realistic given the company’s adjustments. The cyclicality of the business was flagged as one particular concern, though the company has only seen two downturns in revenue in 2009 and 2020.

Another potential issue is guarantor coverage which, at 61% of Q3 2022 LTM revenue and 78% of total assets, looks relatively low, the first buysider said.

Additionally, the significant number of patents the company has (40) could see the business badly affected if these were threatened, the buysider continued. However, as highlighted in 9fin’s Legal QuickTake, the deal includes a “J. Crew blocker” provision, preventing intellectual property being transferred to unrestricted subsidiaries (or the redesignation of an entity holding this IP as unrestricted).

Saudi Arabia’s Dussur took a 20% stake last year and injected €100m into the business. As well as recapitalising the company, the involvement of the Saudi state-owned enterprise may bring a boost if it opens the door for Italmatch to do additional business in the country, according to the buysider.

Joint global coordinators and physical bookrunners on the deal were BNP Paribas and Goldman Sachs (B&D). Joint global coordinator and joint bookrunner was Citigroup. Joint bookrunners were Credit Agricole and UniCredit.

9fin published Credit, Legals and ESG QuickTakes on the deal earlier this week. If you are not a client but would like to request samples of these reports, please complete your details here.

Cranking out the bonds

The week saw a variety of other issuers tapping the market.

German automotive parts manufacturer ZF Group priced €650m 5.75% green SUNs, due August 2026, at 99.66 for a yield of 5.875% on Thursday (26 January). Proceeds will finance eligible green projects. The issuance tightened from initial price thoughts in the 6.375% yield area. Bookrunners on the deal were BNP Paribas, Commerzbank, Deutsche Bank and Santander.

French equipment rental company Kiloutou Group priced €200m E+550bps SSFRNs, due July 2027, at 96 OID on Tuesday (24 January). Proceeds will refinance a €150m senior secured bridge loan that financed the acquisition of Denmark’s GSV. The issuance was upsized from €150m and tightened from IPTs of E+550bps at 95 OID. Joint global coordinators and physical bookrunners were Credit Agricole (B&D) and Natixis. Joint bookrunners were BNP Paribas and Societe Generale.

9fin published Credit, Legals and ESG QuickTakes on the deal.

Sweden-based Verisurepriced €450m 7.125% SSNs, due February 2028, at par on Thursday (26 January). Proceeds of the deal will be used to repay the alarm maker’s RCF drawings. The deal was upsized from launch size of €350m, and tightened from IPTs in the 7.5% area. Goldman Sachs was sole physical bookrunner. BofA, JPMorgan, Barclays, Credit Agricole, Credit Suisse, Deutsche Bank and Morgan Stanley were joint bookrunners.

9fin published Credit and Legals QuickTakes on the deal.

French debt servicer iQera priced €500m E+650bps SSFRNs, due February 2027, at par on Tuesday (24 January). The notes, issued both to new investors and as part of an exchange offer, refinance the company’s 4.25% 2024 SSNs, 6.5% 2024 SSNs and E+537.5bps 2024 SSFRNs, with any excess used for general corporate purposes. Sole physical bookrunner and joint bookrunner was JPMorgan. Joint bookrunners were BNP Paribas, KKR and Societe Generale. Co-manager was Natixis.

9fin published Credit and Legals QuickTakes on the deal.

Movers and shakers

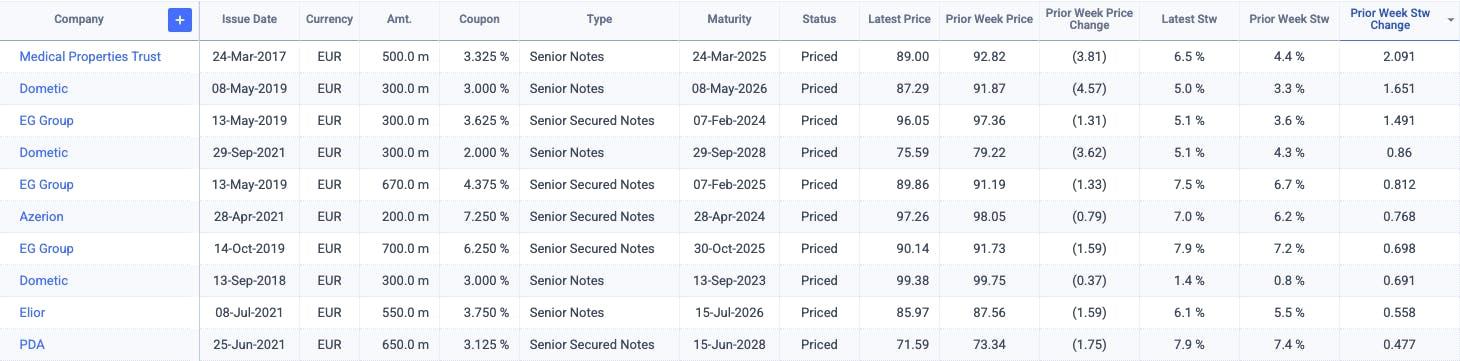

In the euro-denominated secondary market, the biggest loser this week was Medical Properties Trust, the US-based and UK-exposed medical REIT. Its €500m 3.325% 2025 SUNs dropped nearly four points to be quoted at 89-mid for a STW of 6.5%. The decline follows the delivery of a short-seller report from Viceroy Research on Thursday (26 January).

Meanwhile, UK-based petrol station company EG Group’s bonds underperformed, with its €300m 3.625% 2024 SSNs, €670m 4.375% 2025 SSNs and €700m 6.25% 2025 SSNs each losing around 1.3-1.6 points on the week, to be quoted at 96.1-mid, 91.2-mid and 90.1-mid respectively.

The drop follows on the back of press reports that the company could be merged with Asda. The market is concerned by the huge maturity walls that a combined entity would face and its ability to address them – though some lenders told 9fin earlier this week that they were doubtful the transaction would proceed.

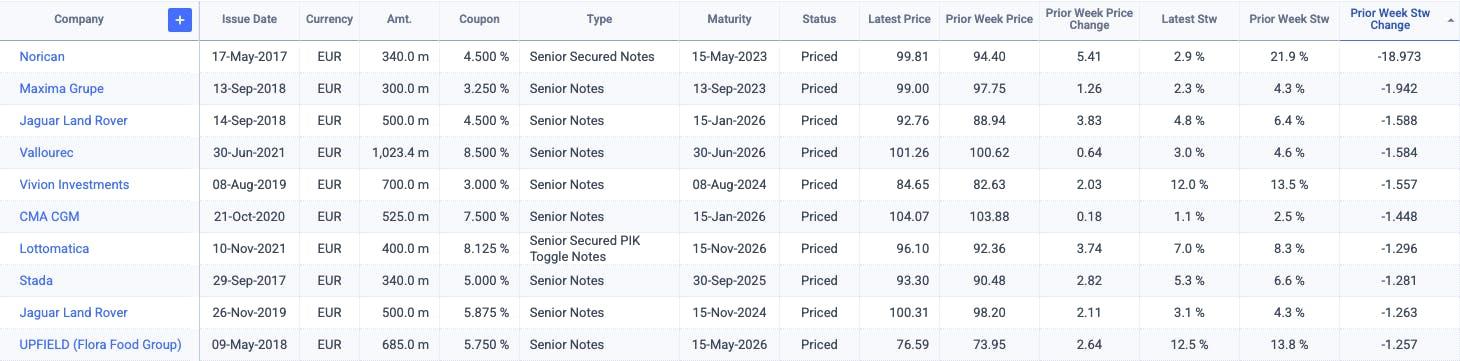

On the other hand, the week’s clearest outperformer was Danish metal parts maker Norican Global. The CCC+ rated company announced it had agreed a refinancing loan to take out its €340m 4.5% May 2023 SSNs, which were trading around 94.4-mid prior to the announcement. The SSNs popped on the news and are indicated close to par today.

Lastly, Vivion Investments’ bonds continue to grind higher, with its €700m 3% 2024 SUNs up two points on the week to be indicated at 84.7-mid. The notes sold off sharply after a short-seller report from Muddy Waters late last year, but have been clawing back losses as the market digests the company’s response and as it announced it had secured a £200m refinancing loan.

Excluding stressed credit (STW < 15%), the following euro-denominated fixed-rate bonds saw some of the biggest week-on-week moves in spread to worst (STW) terms, according to 9fin’s European price moves screener.