This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Forget the Santa rally, European high-yield credit appears to be in the midst of a Hogmanay revivification, both in the secondary market and also with reopening trades in both bonds and leveraged loans.

At time of writing, the iTraxx Crossover stands at 407.5 bps, back to levels not seen since April last year. The index is about 20 bps tighter on the week and 66 bps tighter since the start of the year.

Much of the week’s tightening happened prior to the reassuring US CPI print on Thursday (6.5% YoY inflation in December 2022, down from 7.1% in November), with about 7 bps tightening since the economic data was released. US high-yield credit marginally outperformed European high-yield, with the CDX HY index tightening about 25 bps on the week to 424.75 bps.

The inflation data was accompanied by some relatively dovish comments from FOMC member Patrick Harker: “We will raise rates a few more times this year, though, to my mind, the days of us raising them 75 basis points at a time have surely passed […] hikes of 25 bps will be appropriate going forward.”

Research analysts at Barclays put much of the year-to-date rally in European high yield down to market technicals: ”In the absence of any macro surprises and with earnings season not yet underway, in our view this strength is really being underpinned by strong technicals.”

“We estimate that, in November and December, €13.5bn of cash came into the market via coupons, maturities, tenders and inflows, equivalent to 3.0% of the market notional. The market has also seen net rising stars over this period worth €1.7bn whilst gross supply has only totalled €5.5bn leaving a positive technical tailwind for the market.”

The analysts added that the most notable aspect of the current rally is the relative underperformance of triple-C credit.

We Have Takeoff

Unrated Air France-KLM priced its dual-tranche euro-denominated sustainability-linked bonds. It placed €500m 7.25% May 2026 SUNs at 99.7 and €500m 8.125% May 2028 SUNs at 99.55. The deal was 2.6x oversubscribed and tightened somewhat from initial price thoughts in the 7.75% and 8.5% area.

Proceeds will be used to partially repay French state-guaranteed loans provided to the airline during the Covid-19 pandemic. The deal was arranged by Deutsche Bank, HSBC, Natixis, Societe Generale and Credit Agricole.

As a reopening trade after a wretched 2022, the issuance proved just the ticket. “It was a great one to open the market with,” noted one market participant.

“It's a familiar name, a flag-carrier still riding post-pandemic demand and enough European travel to hold up in a cost-of-living crisis – you need a name like this to sooth market nervousness and get people comfortable,” they added.

The sustainability label KPIs will see the coupon step up by 75bps on the 2026 SUNs and 37.5bps on the 2028 SUNs if Air France KLM fails to hit a 10% reduction in Scope 1 and 3 jet fuel greenhouse gas emissions by December 2025 (from its 2019 base).

The SLB format came in for some criticism in the press last week, as Bloomberg highlighted that proceeds are not tied to specific sustainable projects – instead, they incentivise issuers to hit predefined sustainability targets or face a financial penalty. But, according to Bloomberg, these targets are often unambitious and the penalties for missing them inconsequential.

However, research produced by Swedish non-profit Anthropocene Fixed Income Institute (AFII) countered this: “SLBs are complementary to ‘use-of-proceeds’ products such as green bonds in mobilising capital for the climate transition, as they provide an opportunity to improve disclosure and climate performance at a broader, corporate level.”

Specifically in the case of Air France-KLM, AFII noted that by basing the KPIs to 2019 – prior to the pandemic drop-off in air travel – the airline has set itself a more challenging target.

The period between the sustainability test date and the notes’ maturity is not long, especially for the shorter-dated notes (the test date is in December 2025 means any coupon step-up would only impact the 7.25% May 2026 SUNs for a few months before redemption).

AFII acknowledges this, but – on balance – sees the issuance as a positive. “Using the AFII option pricing model, we estimate the value for the five-year bond SLB premium to be 7.5 bps. While significant for an investment grade issuer, this has a more muted impact on the funding spreads for Air France-KLM. Nevertheless, it is a positive step to make a public climate commitment, which will increase transparency in a challenging sector.”

Extended School Terms

As predicted, in the leveraged loan space, A&E is the name of the game — with plenty of deals both in pre-marketing and having already launched.

Nord Anglia Education, which operates international day and boarding schools, was first out the gates, as it seeks to extend up to c. €1.3bn worth of euro-denominated 1L debt and its $500m in dollar-denominated TLB debt, both maturing September 2024, until January 2028.

A global lender call is being held today (13 January) at 3pm UK time. Joint global coordinators and physical bookrunners are Deutsche Bank, HSBC and JPMorgan (though HSBC is passive on the dollars) Mandated lead arrangers on the deal are Citi, DBS Bank, Goldman Sachs, Morgan Stanley, Standard Chartered, BofA, E.SUN Bank. The private schools company was bought out in 2017 by Canada Pension Plan Investment Board and Baring Private Equity Asia.

Sources told 9finearlier in the week that the maturity extension for Nord Anglia is expected to be relatively straightforward, with outstanding loans trading in the mid- to high-90s. “It is a super solid business. It won’t struggle to get done,” said one buysider presounded on the name. Price talk was released this afternoon, with the euro tranche guided at E+ 475-500 bps at a 97 OID, while the dollar tranche is guided at S+ 475-500 bps at a 97 OID.

As reported, another A&E expected in the pipeline is SafetyKleen, whose maturity extension is also expected to be uncomplicated. The UK-based industrial cleaning chemicals company attempted to push through an A&E in December, but got timed out. However, the deal is already garnering positive feedback in premarketing, with one buysider telling 9fin they would “jump all over” the offering.

“It’s been a solid name for us and honestly, there’s so little supply that we’re willing to be lenient at the moment,” said the buysider. SafetyKleen raised a €455m TLB when it was bought by Apax in 2017, upsizing the facility later that year with a €40m add-on. According to its latest financials, it had £495m-equivalent in euro-denominated TLB at the end of 2021.

More levloan supply coming from Inetum, as the French IT company launched a €100-150m 1L TLB add-on to partially refinance its outstanding €533m TLA (as this column noted, TLA takeouts became something of a theme in December as LevFin markets recovered at the back end of the year and banks sought to offload exposure).

The add-on will mature in October 2028 and is guided to pay Euribor+ 500 bps (0% floor) at 91 OID. Physical bookrunners are BNP Paribas and Credit Suisse, joined by Credit Agricole, Goldman Sachs, Macquarie, Societe Generale, UniCredit, BBVA and RBI as bookrunners.

Meanwhile, the long-anticipated syndication of the €2.9bn in buyout debt backing Advent’s acquisition of the carved out DSM Engineering Materials (part of Royal DSM’s engineering materials business) and its merger with LANXESS’ materials business may finally be around the corner. The deal could be pre-marketed as early as mid-February, one banker told 9fin, though market conditions will be crucial. The deal will likely feature euro- and dollar-denominated TLBs.

UBS, BNP Paribas and Barclays are lead bookrunners. A €675m PIK piece was already privately placed with direct lenders.

Aggressive Downgrades

Alongside tracking individual deals, the reporting team has picked up on a number of interesting themes in leveraged finance this week.

9fin’s Michal Sypala this week highlighted investor discontent with S&P Global Ratings’ “agressive” approach to downgrading credits to triple-C. Downgrades to this level can put pressure on CLO managers to sell their exposure: when a CLO hits 7.5% of its exposure to CCC-rated credit, anything above this level has to be marked-to-market, rather than par, potentially hurting the CLO vehicles’ credit metrics and potentially diverting interest payments to equity.

While recognising that ratings agencies are forward looking, buysiders polled suggested S&P has been overly aggressive toward companies that do not face immediate liquidity issues. Among the credits cited were Dutch software company Unit4, UK software company Misys and French industrial manufacturer Novafives. Buysiders noted that sometimes the rating downgrades appear to lag behind reality, and are based on stale numbers.

However, given that ratings aren’t solely based on company financials, but also through sector-wide and macroeconomic assumptions, the overall worsening of the economy - with recessions both in the UK and Europe having been widely predicted for some time now - may also be putting pressure on ratings.

Alternative Methods Of Offloading Exposure

Meanwhile, 9fin’s Owen Sanderson picked-up on banks’ use of the credit insurance market to de-risk hung LBO exposure. This market is already well established for banks seeking capital relief on their core loan exposures, and represents a well-known way to improve the capital treatment on RCFs.

In return for ceding a portion of the margin, lenders can achieve a degree of RWA relief, one banker said. “It’s another way to recycle or reduce risk, and a fairly active market, though less common for discounted facilities or those which are intended to come to the primary market.”

Credit insurance can be a cost-effective way to take risk out of the banking system because it sits on the liability side of an insurer’s balance sheet, where the capital treatment for corporate exposures is different from the asset side. Insurers typically invest most of their asset portfolios in rates and high grade credit.

The credit insurance can be structured as either an insurance policy or a financial guarantee. Unlike the bond insurers or ‘monolines’, this would not be a wrapper that moves with the loan exposure, but a policy or guarantee with the underwriting bank as counterparty.

“We’re aware of some insurers with good appetite to insure BSL (broadly syndicated loan) type risk — they’d likely be interested in LBO positions,” the banker said. However, market participants cautioned that insurers typically prefer to face established underwriting banks dealing with core risk, and with experience in handling defaults and workouts, rather than lower tier institutions which may struggle to secure repayment in a distressed scenario.

Movers and shakers

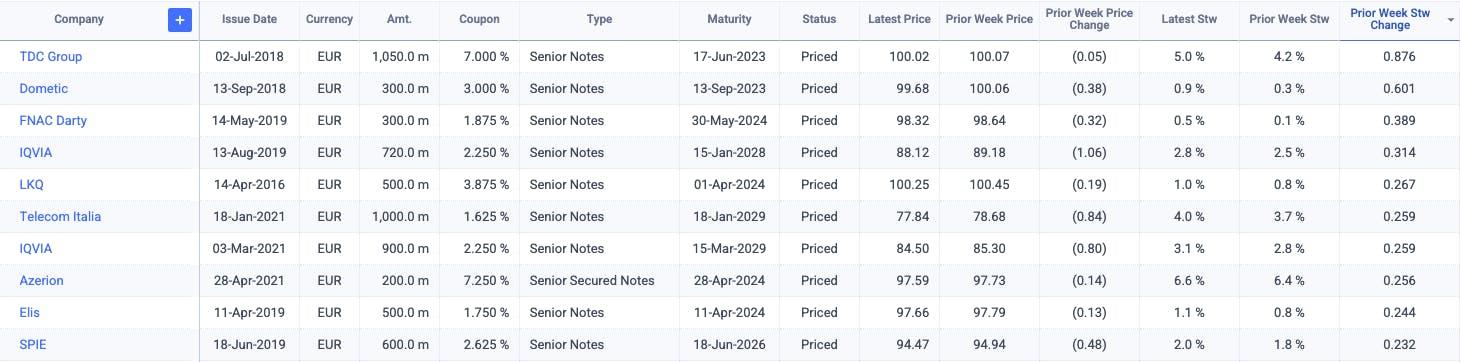

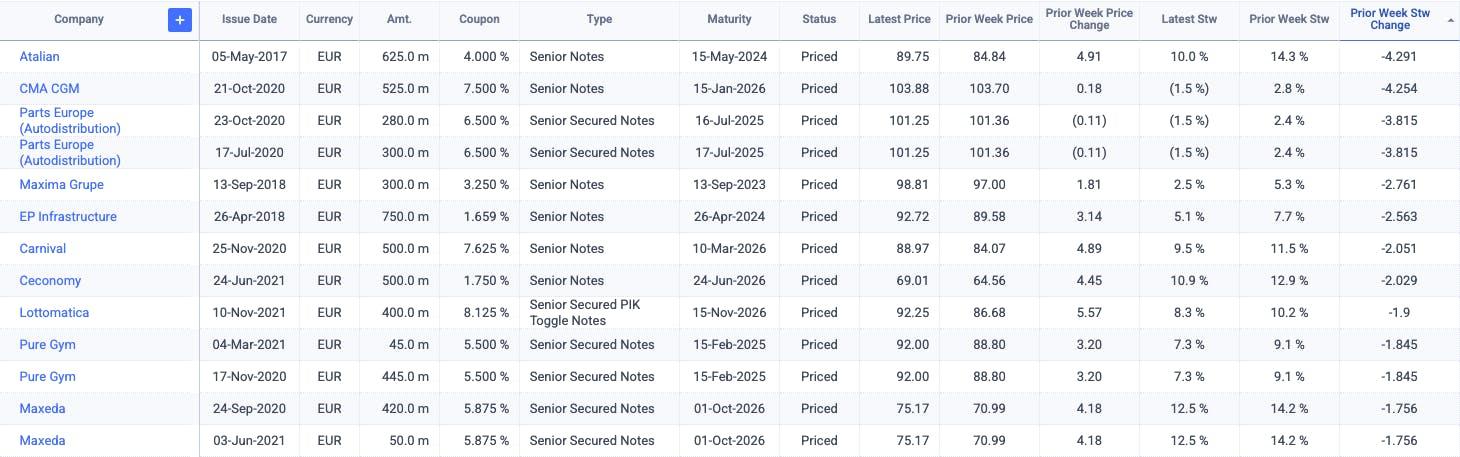

Spread wideners this week were muted, with TDC Group’s €1.05bn 7% 2023 SUNs the biggest mover, gaining 88bps for a STW of 5%. However the week saw some fairly sizeable repricings in the other direction, with Atalian’s €625m 4% 2024 SUNs tightening 4.3% for a STW of 10%.

Excluding stressed credit (STW < 15%), the following euro-denominated fixed-rate bonds saw some of the biggest week-on-week moves in spread to worst (STW) terms, according to 9fin’s European price moves screener.