This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

We’ve seen all sorts this week. Markets crashed hard early on, as central banks attempt to square the circle – taming rampant price levels while avoiding the dangers of a hard landing. A 75 bps hike from the Fed (pre-leaked by the WSJ) was followed by a less definitive 25 bps move from the BoE, although the MPC hinted at a more hawkish slant in the future, remaining ready “if necessary [to] act forcefully” in response to inflationary pressures.

Peripheral Fragmentation

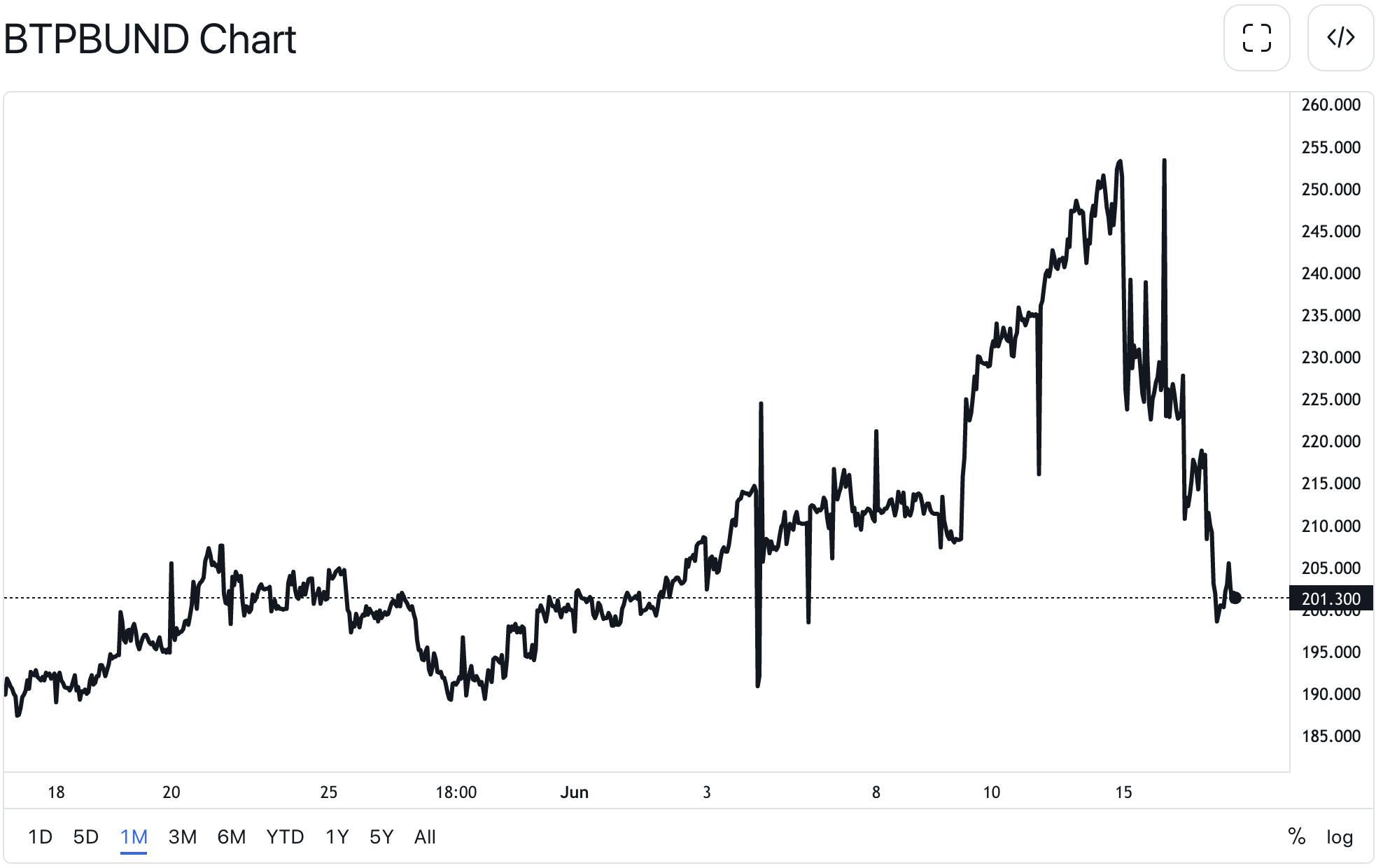

After the market rout, an ECB Governing Council meeting was held on Thursday to discuss widening peripheral govvie spreads. The spread between 10yr Italian BTPs and German Bunds peaked at 250bps ahead of the meeting, but currently sits at 200bps.

Source: tradingview

Stating its intention to apply “flexibility in reinvesting redemptions coming due in the PEPP portfolio”, the council has also mandated the acceleration of a new “anti-fragmentation instrument”, to be submitted for consideration. The move has helped push down peripheral sovereign yields – with the Italian and Greek 10Ys now at ~3.62% & ~3.99%, after peaking at 4.18% and 4.70% midweek.

German 10Y yields rose from 1.50% on Monday to peak at 1.89% and are 1.71% at time of writing, the middle of this week’s range, but are substantially higher than the 0.90% seen a month ago.

Risk-off for lower rated debt

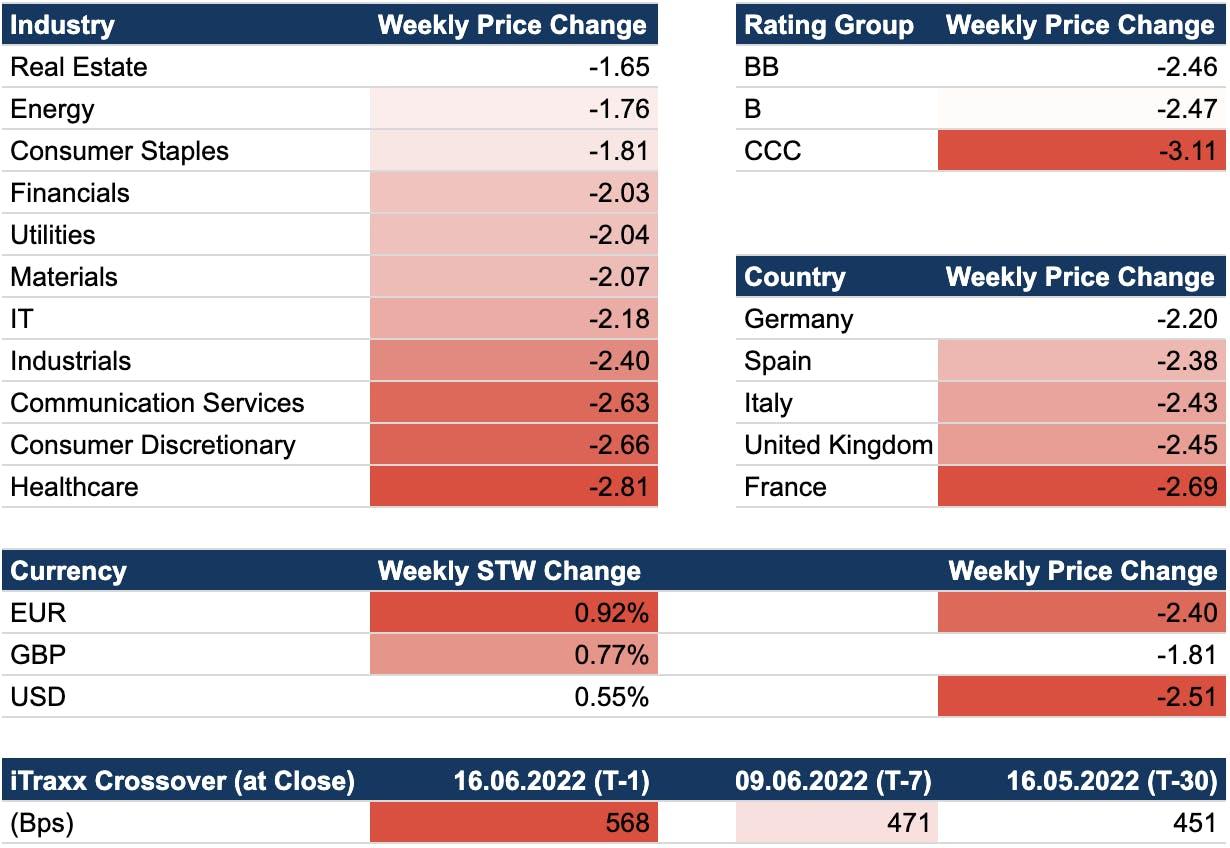

Price action across Secondary was equally painful across both single (-2.47 pts) and double B (-2.46 pts) names, and as with sovereigns, especially hard at the riskier end of the spectrum —triple C names marked average losses of -3.11 pts.

This captures sentiment also seen in US HY primary, where markets moved dramatically during the bookbuild for Clearlake Capital’s buyout of Intertape Polymer Group. The $400m SUNs (Caa2/CCC+) priced at 10%, with an 82 OID, yielding 14.4% – offering a generous spread over the $1,500m TLB, which priced at S+475 and 92. Back in Europe meanwhile, spreads on triple C debt widened 90 bps this week alone.

So, not a week for triple C issuers — as Nordic cruise operator Hurtigruten was forced to postpone its €25m tap of the existing 11% €50m Green SUNs (currently yielding 11.9%).

In a far slicker industry, and slightly higher up the ratings scale, it was better news for Swedish Preem. As conflict in Europe tightens fuel supplies, the group has benefited from strong crack margins, diesel in particular. Preem continues to invest in biofuel capacity, where profitability is supported by a tax exemption for liquid biofuels in Sweden, and similar incentive schemes are being introduced in Germany and other European markets.

Debuting Green Notes, the countries largest fuel refining and marketing company priced €340m 12% Senior Notes due 2027 (B3/B+) with a hefty 96 OID. Together with cash on balance sheet, proceeds from the notes will repay a $540m Term Loan.

A signatory of “Fossil Free Sweden” the group aims to become the world’s first climate-neutral refiner, and net-zero by 2035 across Scopes 1, 2 and 3. Methods to achieve this include the transformation of refineries to run on renewable feedstock, use of biogas and renewable energy, and use of carbon capture and storage.

Elsewhere, Luxembourg-based Metalcorp Group tapped its 8.50% SSNs due 2026 (B) for a further €50m – offering a c.3% discount to the market price (86.2-mid as of Monday) in a private placement to provide additional working capital and for near-term ‘strategic initiatives’.

And then, just as we thought the market was firmly shut to risk-on LBOs, today we had the surprise announcement of a new deal from Manuchar. Led by Credit Suisse, the chemicals business is offering €350m Senior Secured Notes due 2027 (B3/B) to fund the buyout by Lone Star. Marketed on net leverage of 3.4x, EBITDA has been normalized from $179.9m to $105.0m, accounting for unusually favourable conditions related to supply-chain and Covid-19 disruptions.

An investor call is planned for 9am Monday UKT.

High Yield Secondary

Instruments were down an average -2.33 pts this week, with only 4% of our coverage managing a positive gain. The moves were fairly beta-driven, with more defensive sectors like Real Estate (-1.65 pts) and Energy (-1.76 pts) tracking the smallest losses. Similarly, the iTraxx closed at an impressive 568 bps yesterday, more than 100 bps wider than at the same date in mid-May. Fund flows were equally bleak, with Global (-$849m), US (-$628m) and Euro (-$371m) domiciled credit funds all tracking significant outflows, according to BofA Global Research.

Across currencies, Dollar-denominated debt in EHY markets performed worst, relative to GBP-denominated, although on a spread-to-worst basis, Euro-denominated debt saw the greatest widening, up ~92 bps on the week.

In addition to the general downturn, a host of names suffered large declines in excess of immediate re-rating by central banks, including Dana Incorporated (2027s -8.4 pts), TIM (2036 -7.6 pts), INEOS Quattro (2026 -7.5 pts), ION Group (2028s -7.4 pts), and Sarens (2027 -7.0 pts).

And outside the Adler Group complex, a few names managed gains this week. Although some of the worst performers of recent times — Orpea (+3.2 pts) Graanul Invest (+2.9 pts), Paprec (+1.8 pts) and Frigoglass (+0.5 pts) — perhaps collecting demand from bargain-hunters.

Leveraged Loans Primary

A tale of two cities — it was conference week for various pockets of our market — but speakers and attendees at Barcelona’s Global ABS and Berlin’s SuperReturn have been telling opposite ends of the same story.

In both the question of a recession loomed large, with rate movement noise, as always, in the background. But while Barcelona described the dearth of leveraged loan supply in Europe constraining the CLO space, lenders in Berlin sang the praises of private debt in stepping up to meet the financing requirements of leveraged credits left behind (clients can see here and here we have made the latter article free to read here) as the pricing point between the two converges.

“It’s been a trend for the last few years, but over the past few months, the majority of business we’re seeing is companies that have turned away from syndication or failed to get it done,” the private lender said on the sidelines. Speakers described the “bigger and bigger” problems leveraged finance credits were turning to the private market to deal with, with structures including unitranche and club deals ballooning.

Nonetheless, some attendees doubted the ability of the private debt market to absorb the new wave of demand coming its way. Historically operating on small, subordinated deals, private debt providers are now being tested by the larger hung deals that flopped in the syndicated market. Eyes are currently on the Boots buyout deal, which private lenders expect to go their way, and will be a test of their market’s capacity.

Illustrating the market’s current weakness, US-based enterprise software firm Kofax axed a €300m euro tranche on its financing this week despite private credit taking a significant share of the dollar financing in pre-marketing. Supporting a buyout by Clearlake Capital Group and TA Associates Management, the company ultimately chose to pump up the USD portion to $1.346bn from US$1.025bn after a tepid European reception.

A familiar name, Kofax was the first big buyout since Refresco to offer fresh paper in euros and was a hopeful sign in breaking the European primary drought. However, a number of potential investors were put off by old legacy software whose pending contract transformation from perpetual licenses to maintenance SaaS contracts will temporarily squeeze margins and revenue. Aggressive documentation that allowed the new sponsors to pump up leverage was another pain point. Clients can read a preview of the deal here.

Leveraged Loans Secondary

Some speakers at SuperReturn Berlin continued to see loans trading in the 80s as the biggest source of opportunity in the market, however secondary trading nonetheless remains illiquid.

“What I observed in the pandemic was that loans were marked at 80 but the actual bid was 89 and once trading resumed, prices suddenly bounced back to 95,” said one leveraged finance analyst on the sidelines.

Sectors again traded down unanimously, led by Real Estate (-1.6 pts) and Consumer Staples (-1.0 pts). Food names in particular have stayed sour, with Signature Foods dropping -9.6 points to 86 on its TLB this week.

Elsewhere, French pastry firm Cerelia extended the deadline on a proposed covenant waiver from Tuesday to Friday this week, with another extension likely, as some of its €495m-equivalent TLB lenders were unhappy with certain terms of the deal, chiefly sponsor Ardian’s equity contribution (which they’re hoping to come upfront) and the maturity of a proposed PGE loan (which is currently inside the TLB 2027 maturity). Clients can read more here.