This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

LevFin Wrap — From Maxima to minima, 888 holds for holiday

Ben Hoskin

+Kat Hidalgo

•9 min read

And we’re back. Another slow week in primary, against a painful risk-off backdrop, squashed any hopes that supply might return in earnest. Maxima, a BB+ MTN issuer,took all week just to send out price talk before downsizing, and 888 Holdings pushed its debt syndication to next week.

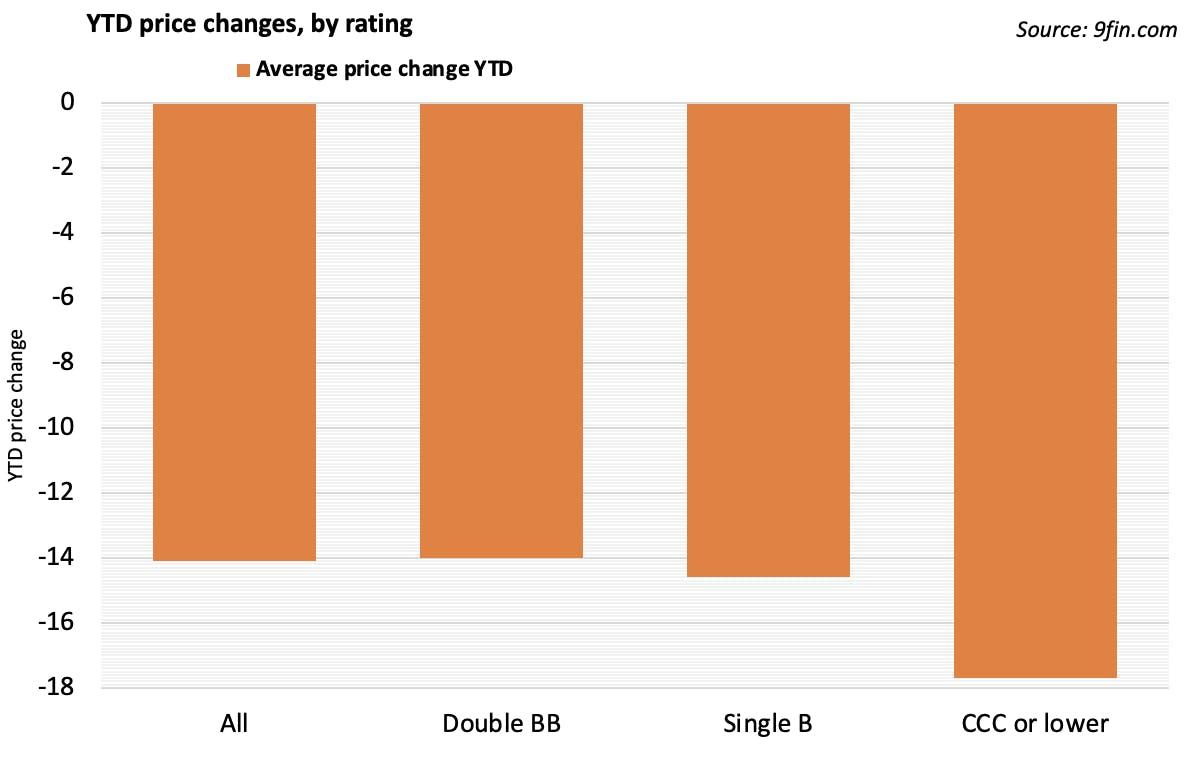

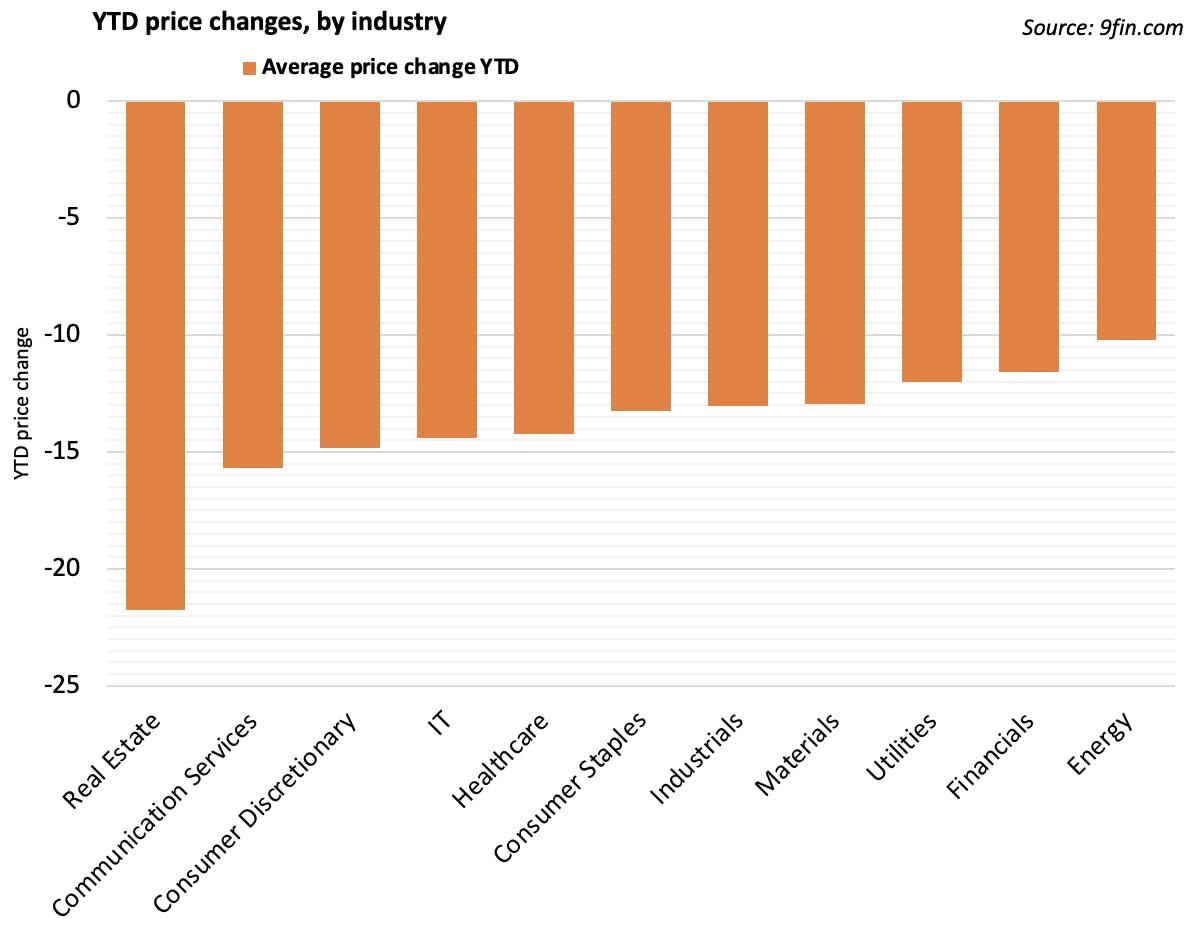

There’s been plenty of talk about how poor H1 has been for various asset classes. Here’s the jam in European high yield: crossover has blown out 338 bps, investors have yanked ~$9bn out of European HY funds, and instruments tracked by 9fin are down 14 points on average.

Real Estate, dragged down by Adler and friends, is the worst performer — it’s fallen nearly 22 points this year. And despite Brent crude rallying almost 50% in the first six months, even Energy (which is outperforming the rest of the market) is down double-digits thanks to bond convexity.

High Yield primary

It’s hard enough selling risk right now, so reports of new gambling restrictions incoming in the UK were the last thing Gibraltar-based gaming group 888 Holdings needed as it brought ~£1bn of debt to market.

Coming ahead of new regulation from the UK government, the deal is a tough ask given current market conditions, despite some lenders’ familiarity with the name and the industry.

The financing is split between euro SSNs (fixed and floating rate) of an undetermined amount and a $500m TLB tranche, rounded out with a £358m delayed-draw TLA and a £401m-equivalent euro TLA. All instruments are rated B1 (see our preview of the deal here).

We’ve talked before of the “Fitch Premium”, which offered around a notch uplift versus Moody’s and S&P during 2021. But for 888, the four-notch differential between Fitch’s BB+ and S&P’s B (Moody’s gave a B1) at the instrument level was particularly eye-popping.

A one-week syndication was always ambitious, although the deal was extensively premarketed. Official guidance on the bonds is yet to be circulated, though two sources expect a total yield of 10% on the FRNs and slightly higher on the fixed rate SSNs.

This morning, leads announced that syndication would be wrapped up “mid-next week”. They blamed the delay on posting the US TLB agreement, as well as the upcoming Independence Day holiday in the US.

That gives investors more time to assess heightened regulatory risk. The Timesreported on Wednesday that the UK government is set to unveil new gambling restrictions in the country, which makes up around two thirds of 2021 pro forma revenue for the combined 888 group.

Rules are likely to include maximum stakes in online casinos and affordability checks for customers with substantial losses. The Gambling Commission (Britain’s gambling regulator) is potentially going above and beyond these rules by ramping up their own affordability checks.

If you’ve been under a rock for the past week (or perhaps just enjoying some sun) you can get up to speed with the deal and the new regulations through our detailed coverage here.

Finally, Baltic retailer Maxima Grupe mandated banks for a €300m SUN on Monday to refinance €300m SUNs due 2023. Guidance for the new issue was seen today at 6.5-6.750%, double the current coupon of 3.25%.

The size was reduced from €300m to €240m, and the sellside announced that “an international development institution” had board approval to take down up to 30 per cent of the issue.

In sickness and in health

Apollo and Reliance Industries’ jumbo LBO of UK pharmacy chain Boots has fallen foul of vigorous rate hikes, with seller Walgreens and the two buyers unable to agree a price after the rise in financing costs.

As reported by LPC, some banks weren’t even interested in taking on the risk at all, pointing to the miserable failure of CD&R’s buyout of UK supermarket chain Morrisons, which wiped out bankers’ fees.

Elsewhere, TPG Capital announced its acquisition of Italian drugmaker DOC Generici on Thursday, with a muted reaction in the bonds despite the change of control. The €470m SSFRNs due 2026 rose less than a point to ~97.25, even though the schedule stipulates a par takeout.

We don’t know the EV yet, but it isn’t likely to be similar to some of the other tough LBOs of late: applying the 12x EBITDA multiple from when ICG and Merieux acquired the business in 2019 gets you to ~€1.3bn.

With the margin on the FRNs at 3.875%, the tepid reaction in the bonds may just be the relative unattractiveness of putting your cash here, with most of high yield secondary on sale. Still, if you believe the deal gets done (it’s expected to close in October) why not lock in that return?

Leveraged Loans primary

As we discussed earlier, Gibraltar-headquartered gambling company 888 Holdings tried its chances on a £1.017bn package this week to finance its acquisition of William Hill.

The borrower is compensating for market volatility with a steep OID, with price talk of SOFR+CSA+525 bps and an OID of 92-93 on the dollar TLB.

Still, there is a strong prospect of pricing going wider next week. Books for the dollar term loan portion were 2/3 full as of Thursday morning, with commitments due that same day (see 9fin’s update here).

Investors are already cautious on the sector, and the added complication of an upcoming UK regulatory decision that will impact 888 doesn’t help matters (for more coverage, see our ESG QT here and our Financials QT here).

Gaming1 is also out this week, though with a much smaller deal.

The Belgium gaming business will likely suffer from 888’s presence in the market, as sources say the small number of buysiders looking at the space will be prioritising that deal over this far smaller issue.

To boot, Gaming1 has zero cash on the balance sheet and significant single-jurisdiction risk, with more than 60% of its revenue derived from Belgium.

“Given the amount of regulation to worry about in the industry, the possibility that changes could come in a single jurisdiction and wipe out significant revenue is just too great,” said a buysider.

Of course, the business also faces the same ESG considerations as 888. Several buysiders said it’s difficult to allocate capital to the gambling sector right now, given the amount of ESG scrutiny they are facing from institutional investors.

This week’s gaming issuance provided a break from the healthcare theme we’ve seen in primary recently.

Following Inovie’s sluggish syndication, which priced wide of talk at 94 (down from 96-97) on 22 June, Affidea tried its luck and has now priced.

Despite improved leverage and market positioning, as well as less exposure to the Covid unwind, Affidea still priced at the same OID level as Inovie. Then again, these days it’s difficult to tell whether pricing is wider for credit reasons, or just because of the general market backdrop.

Affidea’s €600m TLB was to support its acquisition by Groupe Bruxelles Lambert’s for €1.8bn. The B2-rated loan pays a coupon of E+500 bps and was issued at 94, after flexing to 93.5 through syndication (original price talk was 95-96).

A stable name with all the trappings of a well-positioned healthcare business in Europe, Affidea’s deal sported just one margin step-down, conservative sponsorship and a strong equity cushion.

Nevertheless, the buyside struggled with macroeconomic pressures such as labour cost inflation and questioned the credit’s relative value versus what’s currently on offer in secondary (see our loan preview here).

Keep holding on

More primary supply is coming, but this is less a sign of bullishness and more likely because banks need to get underwritten debt off their balance sheets before secondary loan pricing drifts even wider.

“For a long time it was about holding on to see if the market would rebound,” said a market source. “But now it’s a question of, if you’re holding on for much longer, are you shooting yourself in the foot?”

When asked if they felt that recent issuance indicated primary markets could be heating up, another source said no: “I don’t think so — Affidea has come out because if anything’s going to get done in this market that would be it.”

Buysiders continue to bemoan pricing volatility. With so little stability, it’s hard to commit to primary offerings.

Nevertheless, 9fin understands there are deals in pre-marketing, including Theramex, another healthcare borrower. The women’s health business struck a deal to be acquired by PAI Partners and Carlyle in May for around $1.4bn, according to Bloomberg.

High Yield secondary

The iTraxx Crossover closed Thursday at 580 bps, another big move wider after starting the week at 536 bps.

On average, instruments tracked by 9fin were 1.28 pts lower. Real Estate (-2.1 pts) and Consumer Services (-1.55) were the biggest losers, with Financials (-0.76) and Healthcare (-0.83) holding up best in this week's sell-off.

In single names, Stonegatehas hired Eastdil and Sapient Corporate Finance to sell a portfolio of ~70 pubs with a combined value of up to £100m, having already disposed of ~£30m of sites since September.

Despite Stonegate’s strong liquidity and improving operational performance as Covid restrictions disappears, the prospect of a recession does not bode well for the UK pub sector.

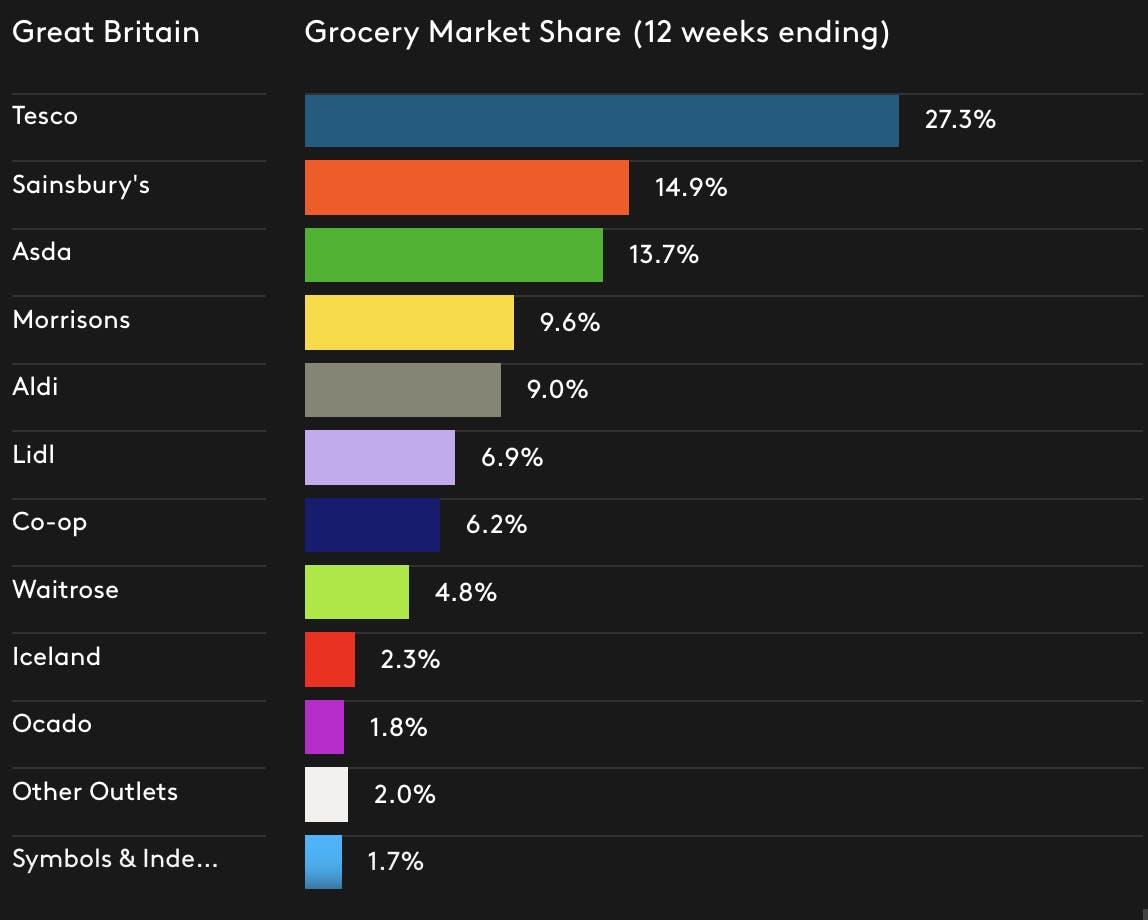

Morrisons also delivered underwhelming results, with sales off 6.4% in the latest quarter. The cost-of-living squeeze and deteriorating consumer confidence is creating “a very fragile and difficult environment”, according to the company’s CEO.

According to Kantar research, Morrisons’ market share has steadily dropped from 12% in 2013 to 9.6% today, with discount retailer Aldi on the brink of disrupting the “Big 4” supermarkets.

Note: 12 weeks ending 12.06.2022 (Source: Kantar)

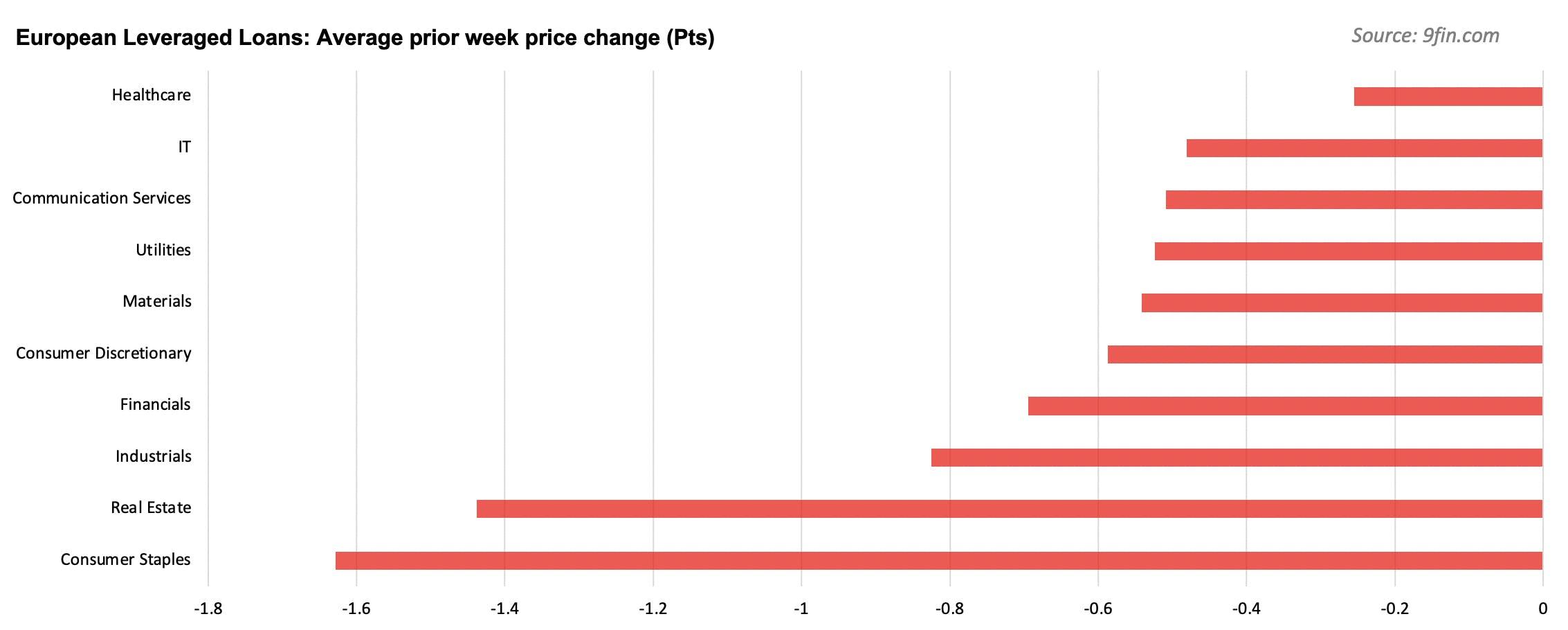

Leveraged Loans secondary

The loan market was down across the board, with both real estate and consumer staples falling more than a point.

Sectors more resilient to commodity inflation (such as Healthcare and IT) were more stable this week, as labour inflation takes longer to hit. Hourly wage inflation was 3.8% in the Euro Area during the first quarter, according to Eurostat, compared to 5% headline inflation.

Investors continue to enjoy the yields on offer in secondary. “There’s so much out there on the secondary market,” said a buysider. “Before, you had to pull teeth to get yield, and now it’s just there.”

The only hitch is long settlement times, which make it inefficient to trade in and out of loans quickly, the buysider added: “It take weeks to get your capital back from a loans trade. The market just doesn’t function like it does in America.”

The biggest upward mover this week was Multi-Color, the CD&R-backed labelling company, with a more than three-point increase on its €500m TLB. The tranche, which pays a coupon of E+500 bps, is now indicated at 93.25.

When the label manufacturer was acquired last October, buysiders were already concerned about raw materials inflation (the company’s primary materials are paper and ink) in addition to heavily adjusted EBITDA.

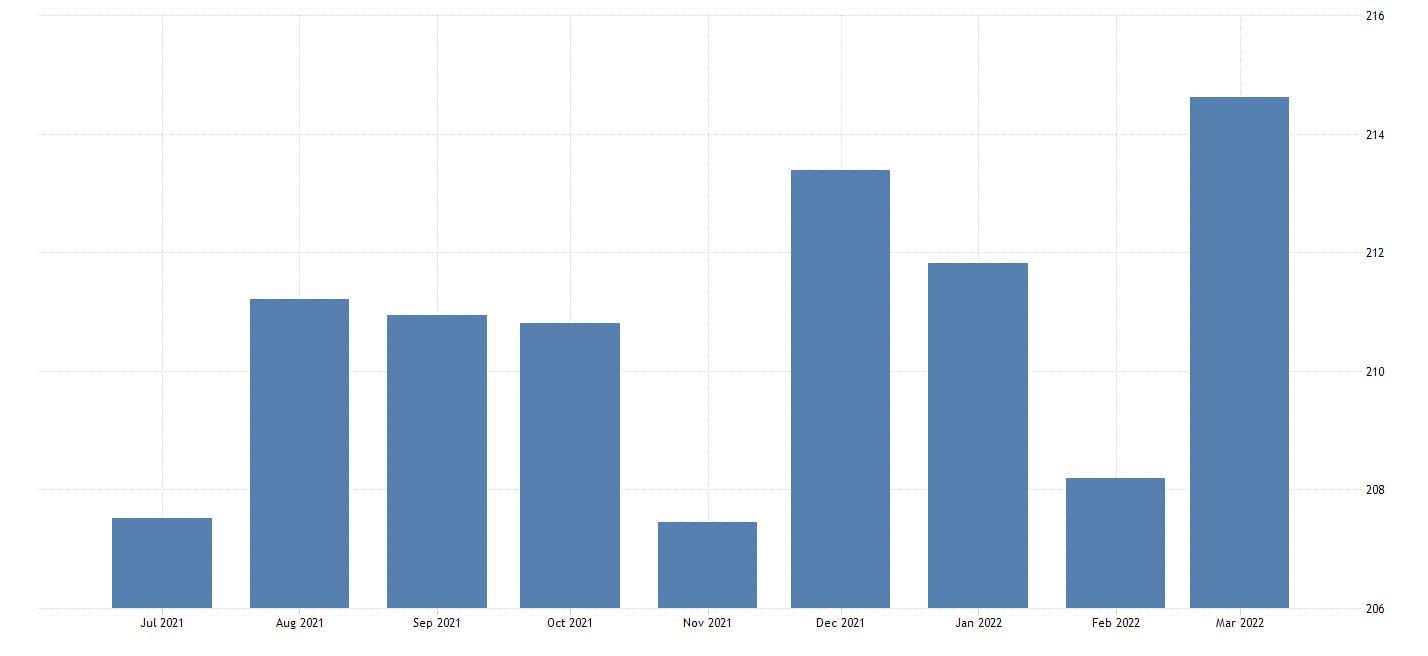

The value of raw materials in Multi-Color’s own inventory rose from $76.9m to $95.5m between December 2020 and June 2021. Data shows the price of wood pulp has only continued to increase this year.

United States - Producer Price Index by Commodity: Pulp, Paper, and Allied Products: Wood Pulp

(Source: Trading Economics)

The downward movers were much more dramatic this week. Food inflation continues to hit, with the biggest decliner being Flamingo Afriflora, a Dutch flowers and food producer. Its €280m TLB, which pays coupon of E+575 bps, is indicated at 90 after a 9.5-point drop this week.

Close behind is Valeo Foods, probably best known for producing Kettle Chips. The company’s £81m tranche, which pays a coupon of L+850 bps, suffered a 8.750-point dip this week and is now indicated at 82.5.

Three other tranches dropped more than five points this week, including (biggest movers first) Wella’s £550m TLB, Upfield’s PLN2.089bn tranche and Arvos’ €163m TLB.