This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Rate rises set the scene this week. The FOMC led the way, posting its third consecutive 75 bps hike, and unanimously bringing the Fed funds target range to 3-3.25%. With the dot plot guiding a similar move in November, and 50 bps in December, the median projection is now up to 4.4% by year end. Norway (50 bps), Sweden (100 bps), and Switzerland (75 bps) also announced increases, and on Thursday the BoE hiked 50 bps for the second time. While the UK bank rate is now 2.25%, a third of MPC members were keen for more, voting an outsized 75 bps.

On Friday, UK Chancellor Kwasi Kwarteng announced the much anticipated mini budget. The basic rate will be cut to 19p in the pound, the higher rate 45% abolished altogether, and the reversal of April’s National Insurance rise was confirmed. Planned duty rises on alcohol have been cancelled, stamp duty cut immediately, and banker bonus caps are out.

GBP traded off, hitting new lows of $1.10 to the dollar, and the 10 and 2 year gilt yields jumped to 3.8% (+65 bps this week) and 3.9% (+79 bps) respectively, as weighty new debt sales are anticipated to fund government plans. Importantly, however, Kwarteng did affirm BoE independence as “sacrosanct”, an area highlighted when UK Prime minister Liz Truss previously suggested a review of its mandate.

US equities proved volatile after the Fed announcement, with the S&P down, then up, then finally down again around -2.1% on Wednesday. Meanwhile both the FTSE 100 and EUROSTOXX 600 were especially punished this week, down -4.0% and -4.7%.

Back in credit, it was rollover week for the iTraxx Crossover, which opened 44 bps wider on the new series. Galp Energia, Lagardere and TVO were out, while Autostrade Italia, EP Infrastructure and INEOS Quattro made it into S38. Relatively soft, the index moved out over the week, closing at 619 bps on Thursday, and reportedly up to 637 by Friday lunchtime.

As expected, new primary supply arrived with the bond portion of Inetum’s (B2/B) buyout financing by Bain Capital. Offering €300-400m SSNs, alongside a €300-400m TLB (since upsized to €450m) and a €333-533m TLA, the LBO will also be funded with €68m cash on balance sheet and €568m of equity. The sponsor agreed the acquisition in January 2022 for a cash consideration of €1.631bn (6.6x December 2021 PF Adjusted EBITDA of €246m).

Settling at the lower end of the range, price talk for the €300m SSNs arrived on Friday morning at 10.25% to 10.50%, with a coupon in the high 7s.

Various doc changes arrived with the price talk, removing the 100% available restricted payments capacity and reducing certain basket sizes. You can read our Legals and ESG QuickTakes for full details on the deal.

Elsewhere, TeamSystem announced the pricing of a private placement on Thursday. Offering €185m Senior Secured FRNs due 2028, the notes priced at a very reasonable E+625 for par. Proceeds from the notes will finance bolt-on acquisitions, and debt outstanding under the group’s €180m RCF (€14m drawn on 30th June).

High Yield Secondary

Given the tightening monetary outlook, average prices slipped -0.74 pts across Secondary (14% +0.62 pts | 83% -1.00 pts). By Sector, Real Estate (-0.42 pts), Industrials (-0.52 pts) and Energy (-0.60 pts) saw the slightest falls, with IT (-0.85 pts), Consumer Staples (-0.90 pts) and Healthcare (-1.05 pts) faring worse. Declines were fairly even across instrument currency, with GBP leading the way (-0.84 pts), followed by USD (-0.80 pts) and EUR (-0.72 pts).

Among single names, US chemicals group Chemours slumped across its capital structure (-2.7 pts on average) as it announced reduced full year guidance on Wednesday. Adjusted EBITDA is now expected to be between $1.4bn to $1.45bn, around 7% lower than previously guided. More broadly, recent earnings estimate revisions now suggest two thirds of the S&P 500 revising downward.

Back in Europe, and downgraded a notch to Ba2, Moody’s notes German electronics retailer Ceconomy is under an increasingly challenging economic environment, with evidence that high inflation is affecting consumer spending while also increasing operational costs. The agency expects this will lead to material negative FCF generation in 2022. On Thursday evening it was announced Group CFO Florian Wieser will leave the company on 31 December.

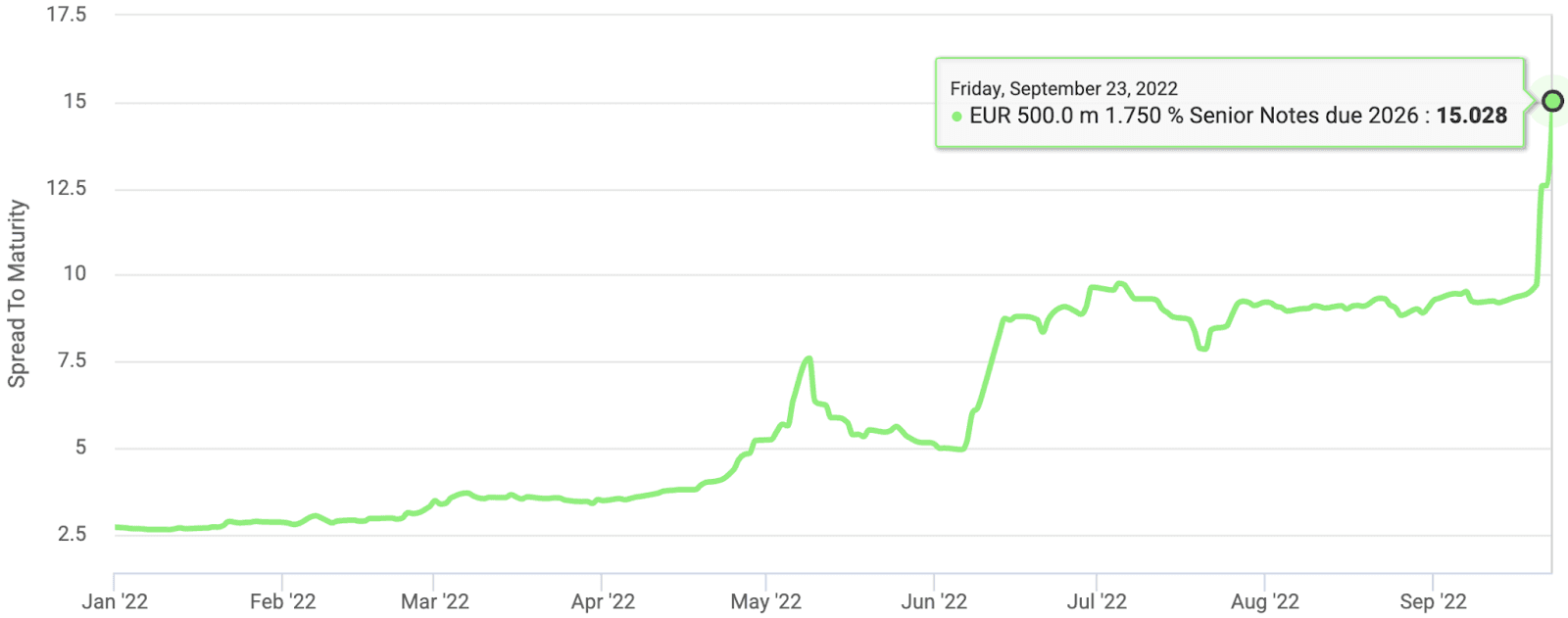

Prices on the low coupon €500m SUNs drop -13.6 pts on the week, and STM crosses 15%

As reported by Bloomberg on Wednesday, Singapore-based gateway services provider SATS Ltd. is in talks to acquire Cerberus-owned aviation cargo handler Worldwide Flight Services (WFS) for as much as $3bn. Both groups have confirmed discussions are ongoing, and WFS’s 2027 fixed notes jumped over +9 pts on the news. However, 9fin’s Olivia Mantock reports SATS could avoid triggering a change of control put (CoC), due to a lenient portability feature.

With a similar theme, Singapore’s sovereign wealth fund GIC announced on Thursday it will take a majority stake in Sani / Ikos Group (SIG). The acquisition will be the European hotel sector’s largest since Covid-19 — valuing SIG at €2.3bn — and is expected to close in Q4 2022. GIC states in a press release that, due to portability, the €300m SSNs due 2026 are expected to remain in place. Despite this, the notes popped over +6 pts on the week — read our CoC analysis here.

And finally, Italian gambling group Lottomatica, who priced its €350m SSNs last week with what looked like a healthy premium, has seen the notes perform well, last seen today at 101.2.

Leave something on the table

Leveraged Loans Primary

The spate of deals in primary brings with it a renewed tousle over where pricing needs to land in the market’s on-going risk-off sentiment.

“The market is still in price discovery and the worst case scenario is a quick rebound into where pricing was pre-crisis, but I don’t think that’s going to happen across the board anytime soon,” said one buysider. “There will be dispersion along credit quality that gets even wider, definitely, and that will only compound when we see Q3 results.”

Some on the sellside, however, see positive momentum in coming to a pricing consensus — “Discovery around OID tension has started to head in a more constructive way,” said one sellside source. “In summer, secondary was down so much that you’d get people saying — ‘Don’t call me if it hasn’t got an 8 in front of it. I’ve got no cash, I have to sell out of something to create liquidity, and I won’t sell at 90 to buy your deal at 92’.”

Now, all five deals currently in market come with an OID in the 90s. French IT services firm Inetum lags (90-91) and agro-chemicals company Rovensa leads (94-95), with the three remaining deals, KronosNet, House of HR and TenCate Grass, happily in a rough middle.

Rovensa’s €387m add-on trimmed pricing to 95.5 (+/-0.25) from 94-95 OID earlier today. Many looking at the deal were existing lenders, pleased with how the company has sprouted up through acquisitions over recent years. Newcomers, who had previously shied away from the sector itself on weather-based crop unpredictability, were also soothed by a plentiful equity cushion.

“I’m hoping this is a sign of strength for the market and this will encourage issuers that they can get a genuine CLO bid on deals,” a second buysider said today. Read more here.

Belgian-based staffing company and market familiar House of HR also launched its €1.02bn 2029 TLB at E+575 bps and 94 this week, accompanied by a relatively unusual syndicated €310m second lien. In recent years second lien has more commonly been pre-placed with direct lenders or private credit funds before the launch of a more broadly syndicated TLB tranche.

The size of the deal itself could prove difficult for the market to digest, but House of HR’s familiarity with the market could smooth the process here, with some lenders describing attitudes towards the name as sweetening in the face of its Covid resilience. “The market in general for the past two or three years has been sceptical on this credit, but it’s one of my favourite names and sentiment is turning now,” a third buysider told 9fin.

For Inetum, underwhelming margins were cited as a risk alongside concerns about volatile demand of the recurring revenue in the downturn. The deal did, however, manage to upsize to €450m on its euro TLB today (from €300m-€400m), potentially allowing the banks to reduce the accompanying TLA, initially set to come between €333m and €533m. Read 9fin’s preview here.

Spanish business outsourcing servicer KronosNet, meanwhile, follows the same path, lessening pressure on its €450m TLB with a €350m TLA. Guiding at 93, the deal funds the combination of Konecta and Comdata, with buysiders keeping an eye on the latter’s knotted past after it emerged from a restructuring in August 2021 following an earnings miss. See 9fin’s Restructuring Database for more details.

“It makes sense to do it this way with Comdata’s history,” said a third buysider. “The TLA can be momentary — come again next year, do an add-on and refi some or all of it at attractive rates.”

This is set to be something of a trend: the siphoning off of euro syndicated debt to TLA, private debt and USD markets could slice supply of €20bn in half in September, Murad Khaled, Head of EMEA Leveraged Finance Capital Markets at Bank of America, told 9fin this week, with around €3-4bn pivot fully or partially into private credit strategies. “That leaves around €8-9bn of true institutional syndicated supply (including transactions currently in market) which is less than half of the corresponding amount we had at the September 2021 restart,” Khaled said.

“As it stands, and without a large bank bid, I think a new money institutional LBO financing of more than €500-600m will likely require a bond component or the ability to incorporate a dollar term loan if preservation of pre-payability is a priority.”

The final offering in market comes from Netherlands-based synthetic grass manufacturer TenCate Grass (92-93 PT). Moody’s changed its outlook on the business to negative in May 2022 on the back of the company’s acquisition of Hellas and Geo Sport Lighting, expecting the moves to delay deleveraging. TenCate Grass last came to the field fairly recently, out with a €315m 2028 TLB at E+500 bps and 98.5 in October 2021.

Leveraged Loans Secondary

As above, softness in the European loans secondary market continues, with all sectors tracked by 9fin down this week. Leading the pack is Consumer Stables (-0.3 pts) and Financials (-0.2 pts).

British e-commerce company The Hut Group fell furthest, down -3.1 pts to 89.1 on its €600m 2026 TLB after it reported a -60% drop in EBITDA in H1 2022. UK auto auctioneer Constellation Automotive Group is also down again following its similar -66% YoY crash in EBITDA in Q2 2022.

More significant is the leapfrog in pricing made by UK health retailer Holland & Barrett after its sponsor LetterOne launched an almost billion-dollar debt buyback. LPC reported that LetterOne had offered to buyback outstanding debt at between 75% and 80% of face value. In response, the company’s loans shot up from between 58 and 61 to around 77.

Lenders had previously told 9fin they were struggling to get from LetterOne what its intentions were with the business (though LetterOne disputed this) after the firm rejected a lender request for an updated business plan and more regular communication in May this year. Concerns had been mounting on the name after a post-pandemic slump in earnings, with extra tension following Western sanctions on Russian oligarch. Mikhail Fridman, a founder of LetterOne, stepped down from the board of LetterOne in March following sanctions.

LetterOne told 9fin at the time: “LetterOne is not subject to sanctions and has communicated this extensively with its stakeholders, including Holland & Barrett lenders.”