This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

A tale of two halves, August markets first rallied on expectations of peak inflation before falling away on reaffirmed hawkishness from the Fed and ECB. Wednesday’s August flash reading for Europe came in at 9.1% – the highest since the inception of the Euro – while 9 of the 19 Eurozone countries are now reporting HICP inflation above 10%.

“You think that’s the peak?”

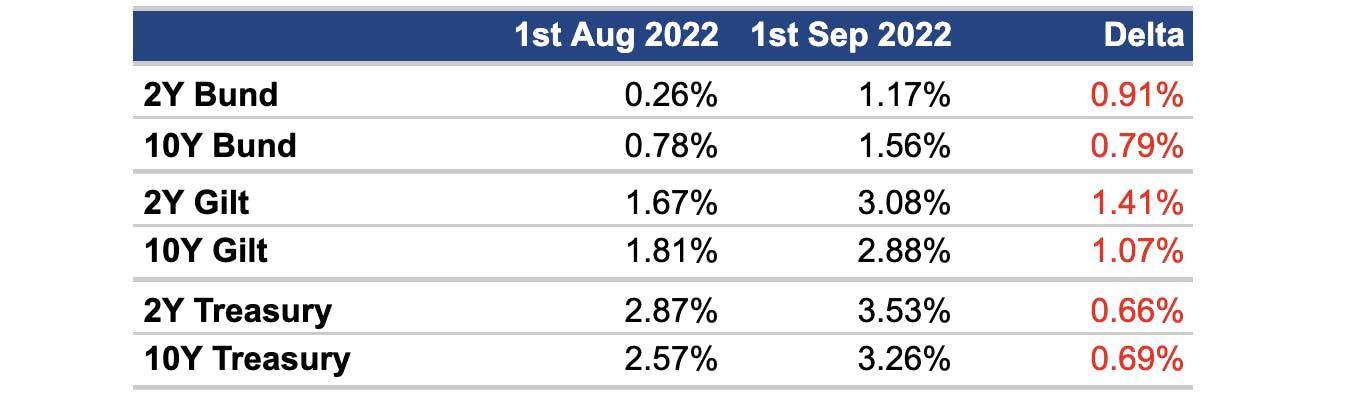

With inflation stubbornly persistent, the narrative has flipped back toward further rate hikes, pushing sovereign yields significantly higher on the month.

The 10-2 yield curve: Bund remains upwards sloping, the US curve remains downwards sloping, and the UK curve is now downwards sloping

Notably, short term borrowing costs for the UK have risen sharply, up 141 bps over the month – yields you have to go back to the GFC to experience. A first among major central banks, the BoE has already reported its intention to commence Gilt sales currently held in the Asset Purchase Facility (which stands at £843.8bn) shortly after the September policy meeting. A sales programme of around £10bn a quarter remains envisaged from September, although this first depends on an MPC vote to begin gilt sales, which will give the market at least a week's notice.

At the periphery, the BTP-BUND spread (now at 236 pts) gave back any tightening from Giorgia Meloni’s announcement last Thursday that she couldn’t imagine ‘wrecking the country’s finances’ or doing ‘crazy things’. The leader of the “Brothers of Italy” party ruled out full control of the country’s national energy groups Eni and Enel, but still plans to nationaliseTelecom Italia.

And at Thursday’s close 172 bps of further ECB hikes are priced in for 2022, lower than the BoE’s 186 bps, and above 142 bps from the Fed. This points to a third 75 bps hike in both Europe and the US.

High Yield Secondary

Tracking a marked loss on the week, instruments were down an average of -1.41 pts (6% +0.59 pts | 92% -1.58 pts). Over the last month, it’s an average fall of -1.80 pts (23% +1.35 pts | 76% -2.78 pts). By Industry, all were in the red, from -0.57 pts for Energy names, to larger moves across Consumer Staples (-1.63 pts), IT (-1.70 pts) and Healthcare (-1.90 pts).

By currency, EUR instruments lost a weekly average of -1.39 pts, GBP -1.41 pts, and USD -1.53 pts. This pattern is matched on a monthly basis, with EUR -1.46 pts, GBP -1.65 pts and USD a sizeable -2.69 pts.

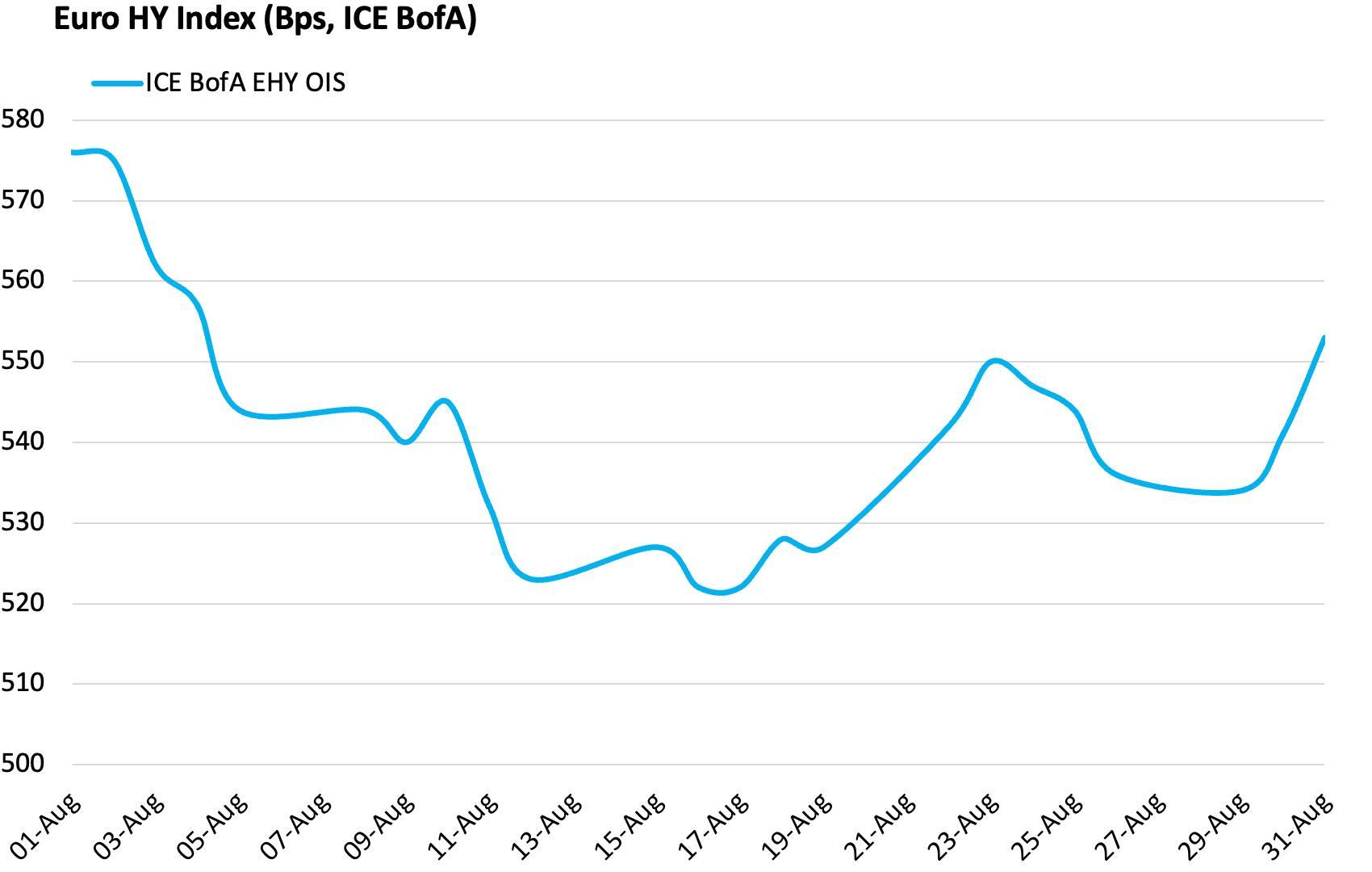

Matching sentiment, data from BofA and EPRA Global shows outflows across Global (-$357m) and Euro (-$207m) High Yield, with a small +$43m inflow for the US. Also, while the EHY index tracked by ICE marked only a 30 bps widening from its lowest point in August, the iTraxx Crossover widened out a generous 125 bps during the traditionally quiet month – last seen on Thursday at 586 bps.

One of the greatest single name drops, Pure Gym SSNs fell an average of -5.2 pts to the high 80s. The low-cost fitness chain reported Q2 numbers last Thursday, although prices only started to tumble on Tuesday this week. At first glance earnings appear broadly positive, with sales +43% YoY, EBITDA +63% YoY. Secured net leverage on the group’s “FY19 Proforma RR Adj EBITDA” stands at 3.5x, although on an LTM basis this jumps to 5.7x.

Likewise, forecourt operator EG Group also saw declines across its SSNs following Q2 results. On a constant currency basis, LfL revenues grew +28%, although EBITDA was down -5% (or -11.7% on a reported basis). The weaker EUR versus the USD was the main driver of a -$25m FX movement, in addition to ongoing inflationary and weaker consumer demand from increases to cost of living. The USD 2025s dropped -5.0 pts to ~93, while the remaining stack fell an average of -1.5 pts.

Other notes softening on earnings include Cheplapharm (EBITDA growth of +4% YoY, but a margin decline from 67% to 58%) whose USD 2028 SSNs slid -4.6 pts, while the EUR 2027 and 2028s fell -2.7 pts on average. Miller Homes (you can read our write-up here) SSNs and SS FRNs dropped -4.6 and -3.6 pts respectively, and family favourite Iceland’s Sterling SSNs dropped an average of -2 pts, as unhedged energy exposure put a £19m hit on EBITDA.

Elsewhere, high natural gas and carbon prices have pushed CF Industries Holdings’ UK subsidiary CF Fertilisers to halt ammonia production at its Billingham complex. As the UK’s largest producer of carbon dioxide, the Government has previously provided financial support to continue production. That won’t happen this time. The knock-on effects have been felt by Ranjit Singh Boparan, the “chicken king”, who warned that the potential shortage in CO2 – used poultry slaughter – could cost the group an additional £1m a week. Their 2025s are down -2.5 pts this week.

And finally, Italian gaming company IGT today announced a capped tender offer of up to $500m of its $1,100m 6.50% SSNs due 2025 and €500m 3.50% SSNs due 2024. The dollars were unmoved as of publication, last seen at 98.6, while the Euro’s are up +0.8 pts to ~par. As of 30 June 2022, the group reported total liquidity of $2.1bn, of which $700m was unrestricted cash.

Leveraged Loans Primary

Finally, a primary loan deal. As physical bookrunner, Goldman Sachs has golden plans for Accell, a bicycle maker, which is issuing a €700m TLB. Valued at €1.56bn, according to Bloomberg, KKR plans to take the Amsterdam-listed business private and support the deal with a €1.3bn equity cheque. See more 9fin analysis on legal covenants here and ESG here.

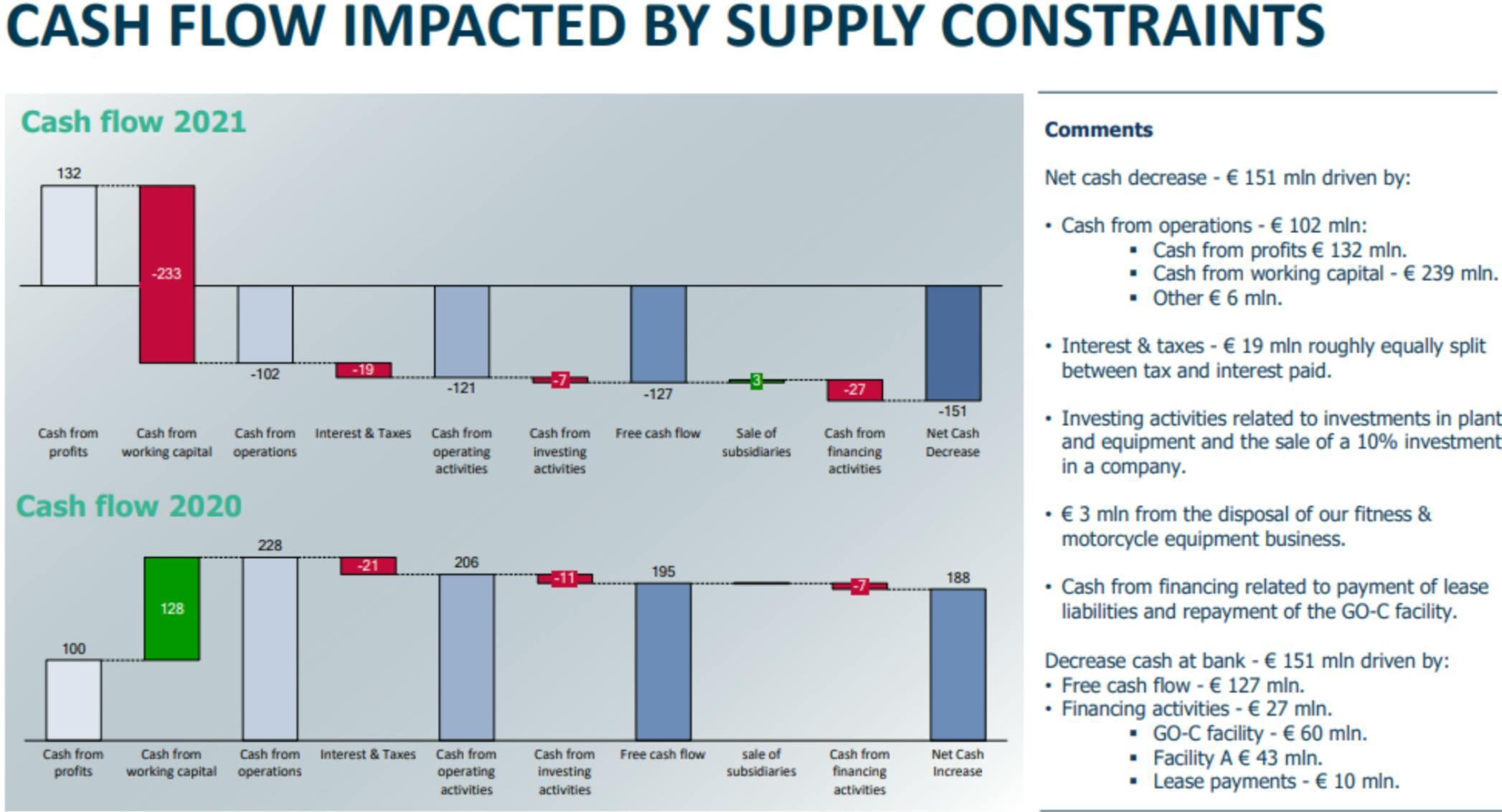

The company produced bicycles and bicycle components and, like any industrials business, has suffered from margin pressure due to supply chain issues since 2021. As a result, and as reflected below, cash from working capital sat at €128m at the end of 2020, while that number was -€233m at the end of 2021, according to its annual report.

Source: Accell company presentation

The tranche will be B1/B-rated (M/S&P) and is currently talked at E+500 bps with the OID TBD. Mandated lead arrangers are Deutsche Bank, Raiffeisen and Shinhan, the latter suggesting we can expect some Korean investment in this deal. Commitments are due 15 September.

Accell has a presence in Asia, especially Taiwan, but is mainly focused on the European market, with 40% of revenue generated in 2021 coming from Germany alone, according to Fitch.

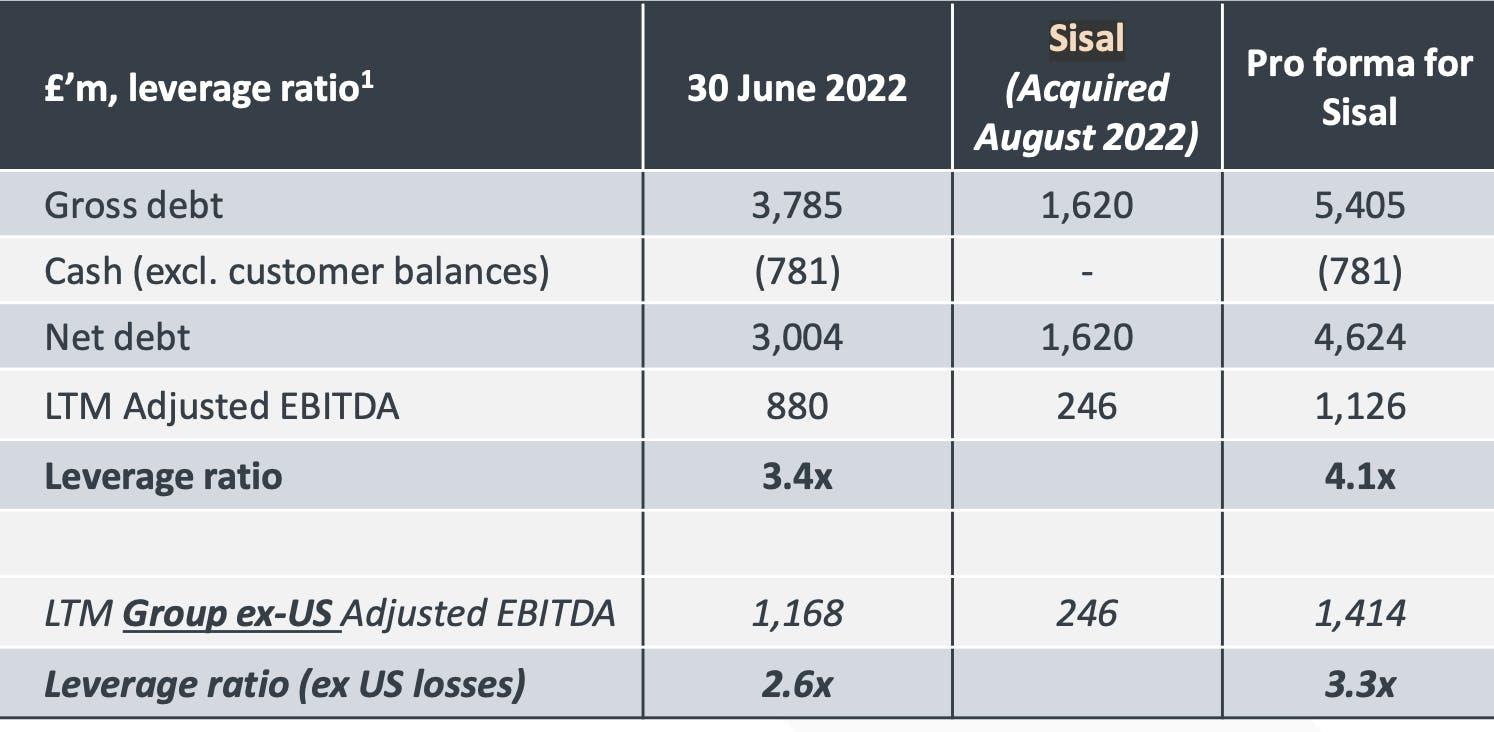

Flutter Entertainment, the gambling company and regular LevFin issuer, today (2 September) has launched a €1bn USD-equivalent TLB to support the acquisition of Sisal, an Italian gambling business that operates online and through bricks and mortar stores. The TLB will form part of a €1.913bn-equivalent financing package, which will include euro TLAs and SSNs.

Source: Flutter Q2 presentation

These deals in Europe should bring some hope to a somewhat negative market, that relies on a steady stream of primary to allow for diversification amongst Europe’s myriad CLOs. But it is also notable that Flutter decided to go all dollars with the syndicated loan tranche.

CLOs in Europe have a much higher portfolio overlap rate than in the US, which usually leads to solid demand for primary.

Looking ahead

One buysider said: “We’re just covering off reporting and waiting for September to see if a few of these deals come through. It doesn’t feel like it’s going to be super busy, maybe the odd deal will come,” earlier this week and prior to the launch of Accell and Flutter.

They were looking to Citrix for the US team and House of HR, a transaction that will be offering a variety of instruments including a TLB and potentially a second lien, though a portion may also go to direct lending. The Belgian recruitment group is coming back to the market, this time to support the acquisition of a 55% stake by Bain Capital for an estimated price tag of €2.5bn to €3bn, according to De Tijd.

Lenders so far are keen to welcome back this market familiar after the long primary drought, praising its strong cash position and acyclicality, as well as existing management. They also believe that Bain should be able to comfortably bump leverage up a couple of turns (from 4x) in the upcoming financing.

Other deals in the M&A pipeline include, a TLB to support Comdata and Konecta’s merger backed by ICG, and another KKR LBO for London-listed power generation company Contour Global.

Buysiders are still laser-focused on pricing and they’re conscious that deals originally underwritten before March 2022 were acquired at inflated multiples and banks would have to be comfortable with structural flex.

One sell side source was positive about the demand picture, stating that 6-8 CLOs were looking to price in September, translating into €2.5bn of fresh capital.

The first buysider disagreed, commenting on how little dry powder is available. “CLOs will have the odd repayment there, but there’s no constant churn of the book. Deals will get done, there is a price point for when you can get something away, it’s just hard to see where the actual dry powder is coming from.”

When asked about where pricing would have to be to syndicate a large deal, two buysiders bemoaned the trickle of primary. “Normally you would have something to benchmark against. In a couple of weeks, we might start to look at alternatives in secondary or do some primary, but there’s an opportunity cost to that [in an illiquid market].”

A second buysider was happy to use secondary prices as a benchmark and said that stable cash generative businesses, such as software names well known to the market and rated B2 could get done at a 95 OID and a E+450 bps margin.

Two others said they felt a 97 OID and a 500 bps margin would be more on the money.

Leveraged Loans Secondary

Once again we’re back in the red, following a few hopeful weeks for leveraged loans secondary, when some portfolio managers felt a bit more comfortable with where levels were at. All industries fell less than a point however, so the damage isn’t too dramatic, yet.

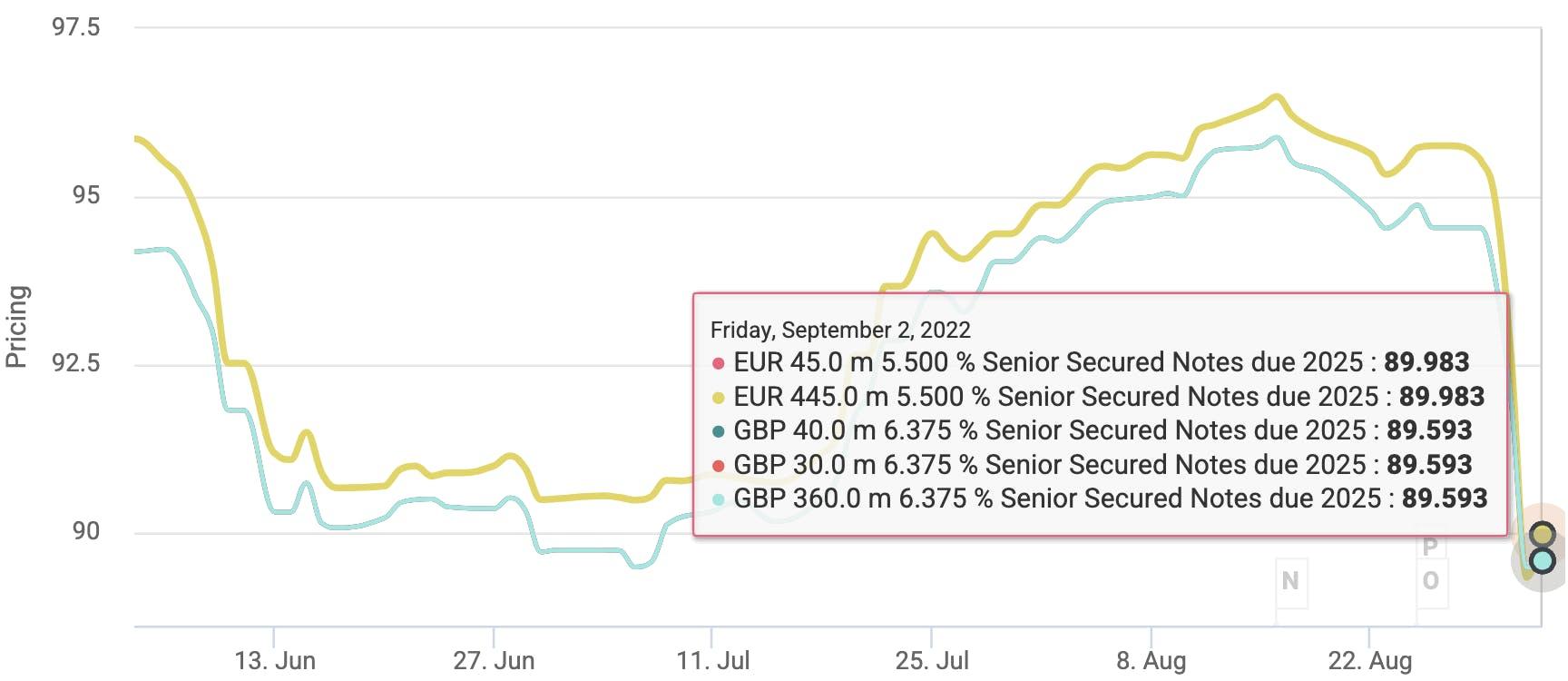

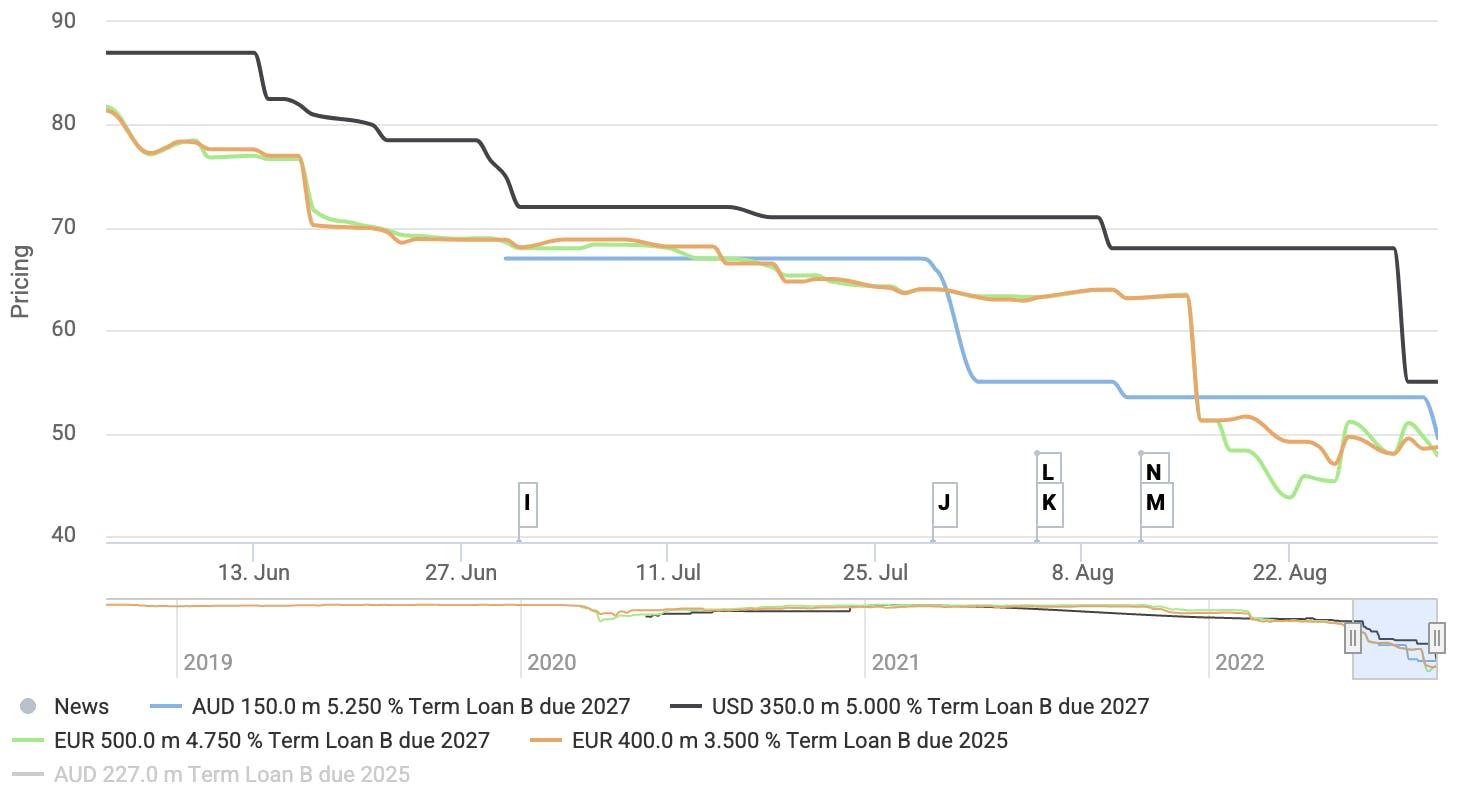

The biggest faller was GenesisCare, with a whopping 13 point drop. The beleaguered healthcare business has seen its TLB pricing fall dramatically in the past quarter, particularly after the sale of GenesisCare’s CardioCo finally came to an end in early August, as reported here.

GenesisCare Pricing

The provider of cancer and cardiac care services sold the asset to Australia-based investment manager Adamantem Capital. The sale was anticlimactic for lenders who expressed disappointment over the net proceeds, said two such lenders. The sale price was not disclosed by the company but Australian Financial Review (AFR) reported that it was between A$200m to A$250m, below AFR’s previous estimate of A$300m.

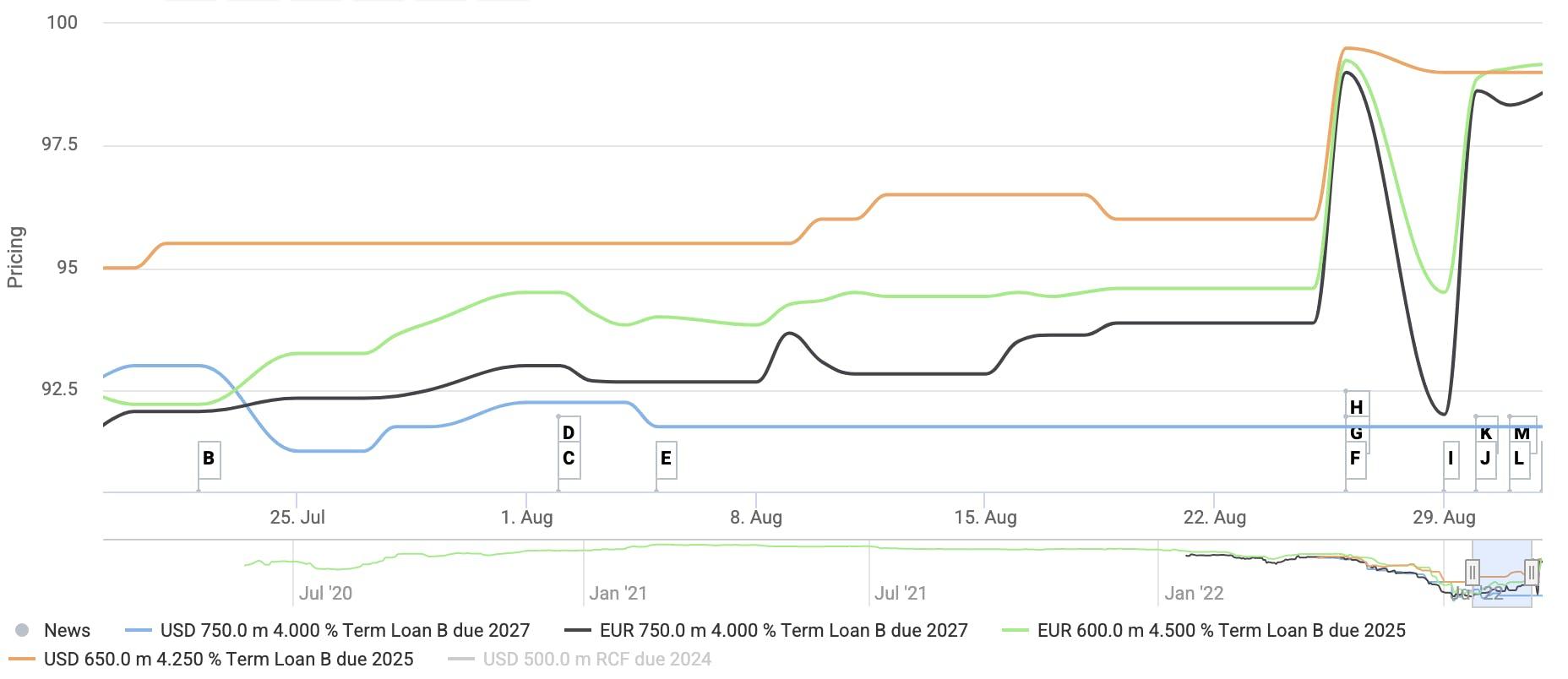

The week’s most dramatic risers were three of Micro Focus’ instruments, following the news the company could be bought and delisted by Open Text for £5.1bn. Moody’s has put the company’s ratings on review for an upgrade given the announcement.

Micro Focus Pricing

Micro Focus International is one of the global leaders in enterprise software and application solutions. It supports customers such as Vodafone, Dell Technologies, Accenture, Sky, BMW, BNP Paribas and the International Criminal Court, with 72% of FY 2020 revenues recurring. See here for a full loan preview.

In other secondary news, bids were due yesterday, Thursday 1 September, on a €91m portfolio of loans comprising 23 euro-denominated loans. The loans were generally either fairly fresh 2022 prints or companies that enjoyed a price bump after recent positive earnings. The biggest ticket was a €6m piece of Mediq’s TLB, followed by €5m slices of Cupa, Inovie, Solenis, Upfield and Veonet. See the full list here.

Another source has told 9fin that Ecotone, the struggling organic food products business, a line item in the above BWIC traded in the low 80s this week. The company missed its budget for the second time in May 2022 this year, as reported here.

Despite reasonable BWIC activity in recent weeks, the lack of liquidity in the secondary market is still bemoaned by buysiders. Three felt as though trading is an obstacle to portfolio management with some unable to buy or sell in a variety of a different credits in a range of stressed and performing scenarios.

The possibility that a trading desk could be blocking a significant trade in a distressed business adds another obstacle, because of the concern that the sponsor may block a transaction down the line due to transfer restrictions. The first buysider said it does happen, but that it depends on the desk and how proactive the sponsor is about names that aren’t performing so well. It is important to note however, that in an event of default, these transfer restrictions fall away.

Inflationary, inflammatory, let’s call the whole thing off

Second quarter earnings have “on the whole [have] been stronger than I thought they would be,” said the first buysider, even as many companies are suffering from either raw materials inflation, wage inflation or both.

Arxada, previously known as Lonza Specialty Ingredients, and a bond and loan name, reported stable second quarter earnings on Tuesday. The Swiss specialty chemical business was able to more than offset all input material price rises, with its gross margins holding steady. Chief executive Mark Doyle and interim chief financial officer Jan Kantowsky expect further robust price increases in the second half of the year to offset inflation, but assured lenders it is not highly exposed to LPG prices, currently experiencing volatile pricing and supply.

Arxada reported 12.6% top line growth in Q2 22 compared to the year before, with pro-forma adjusted LTM EBITDA picking up 16.7% to CHF 538m (€548.6m) in the same period. The company ended the quarter with CHF 45m positive free cash flow, CHF 108m cash on balance sheet and, including the RCF, CHF 347m of liquidity at its disposal. Even against overall growing earnings total net leverage picked up slightly by 0.1x to 6.3x, as the company is holding less cash.

Arxada has a host of bonds and four term loans, each of which are currently indicated between 90 and 95. See here for a full list of Arxada’s instruments.

Kloeckner Pentaplast, another bond and loan name, shared a similar story of offsetting cost inflation with price increases, though in a slightly less effective manner. The company burnt €50m of cash in the first half despite a €35m draw on the RCF, with net leverage ticking up to 9x on an IFRS 16 basis.

Management didn’t rule out the possibility of buying back its discounted debt in the secondary market on it Q2 earnings call on 31 August. Sequential margins were flat for the German plastic packaging firm, but its EBITDA has been suffering for months. The company’s current cap structure was issued in February 2021 on a well documented and heavily inflated EBITDA figure of €305.5m, which compares to a Jun-22 LTM figure of €234.4m. EBITDA guidance for FY 22 was “confirmed” at the lower end of a previously wider range, now expected to come in at €265-275m (versus €265-285m previously).

On the asset-lite, people-heavy side of things, House of HR reported strong earnings as it fights off margin pressure from wage inflation and sickness rates, as well as investments in acquisitions and new initiatives. Reporting on Thursday 1 September, CEO Rika Coppens was able to toot the company’s horn — with good reason.

Q2 saw more than 10% growth in both EBITDA and revenue, but EBITDA margins deteriorated by less than 1%, from 12.6% YTD in 2022 to 11.6% in the same period last year.

Coppens said: “We continue to invest in growth and we continue to believe we will see a growing market. That’s why we invest in digital initiatives, new offices, [expanding into] new areas of expertise, leading to a slight decrease in EBITDA.”

She highlighted gross margin pressure in the form of high sickness rates, but insisted the company was pushing through costs effectively.

“We’re doing all of this to make sure EBITDA says as strong as it was before,” she said. YTD EBITDA is currently €156.8m, up from €137.8m in the year before with Q2 22 EBITDA at €80.3m, up from €72m in the same period in 2021.