This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

Friday Workout - Temper Taper Trap, Ever Tether, Lars’ Heavy Water experiment

Chris Haffenden

•11 min read

9fin staffers returning on Tuesday were braced for a deluge of LevFin supply, but none came, giving respite for another week. We know the forward pipeline is huge; some analysts are predicting record supply in Q3 driven by a number of large buyouts. We also note around €35bn of EUR or GBP high yield paper is trading to call between now and the end of the year. With spreads so tight (especially in HY, single-B lev loans are more attractive IMHO) and government bond yields rising again, as upcoming supply is likely pressurising pricing, it is tempting to stick my neck out and call the top (interim or otherwise).

The risk-on, risk-asset rally from a year ago was characterised by extremely low volatility, with no significant pullbacks, which is very unusual. From bitter experience volatility and liquidity are asymmetric, they shift way more on the way down. But the timing and trigger is uncertain. Powell’s Jackson Hole temper was not to be drawn into the taper trap, is there anything that could upset the disposition of markets?

Sweet disposition

Never too soon

Oh, reckless abandon

Like no one's watching you

Given that we are in the tail end of silly season (August holidays mean hard news is scarce) the Workout looks at some of the more unusual things coming across our desk – the rumours that Tether could be exposed to billions of Evergrande CP – and Lars Windhorst’s attempts via a securitisation to change the molecular structure of his H2O holdings purchases.

Catching a Rising Star

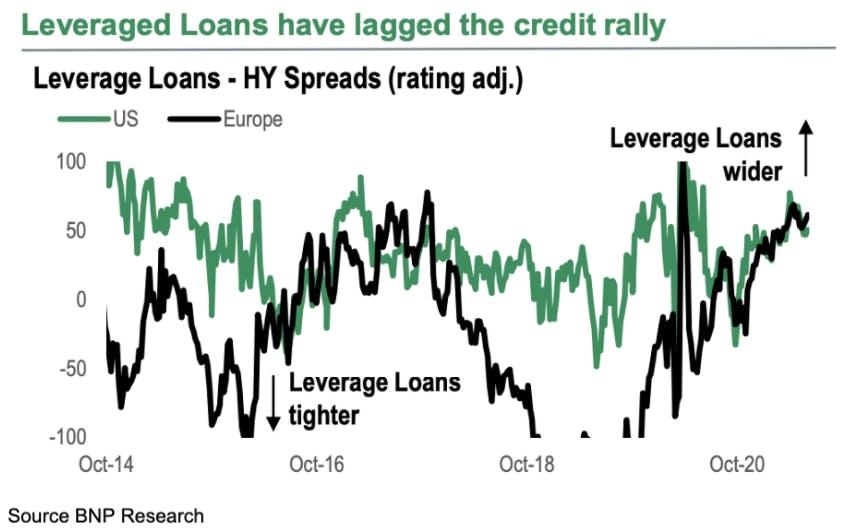

Most sell-side research remains positive on the near-term outlook for High Yield and Leveraged Loans albeit less enthusiastic and euphoric than earlier in the year. Whereas 2020 was the year of fallen angels with record numbers of companies dropping out of Investment Grade, 2021 and 2022 are likely to be years of the rising stars, as upgrades outpace downgrades - BNP is forecasting €29bn of upgrades in 2021. On average this year, 1.5% of the EHY market is upgraded every month, notes BofA.

Picking up on excessive issuance, BNP recommends a defensive stance in EHY by picking BB paper over single-B’s. Conversely, with CLOs in Europe underweight single-Bs which are historically cheap to their bond equivalents, BNP picks B+ names for upward rating migration.

For this to happen, CLO pricing must come in first, however. Over the summer we’ve seen CLO tranche spreads widen, which has in turn impacted the pricing of leveraged loans. The first European loan deal since the August break, Roompot – the Dutch holiday parks business owned by KKR – is a good example of this. The B2/B rated term loan is indicated at E+450 bps, but it could have been priced as tight as E+375 bps in the spring.

Ever Tether, Too Clever?

In recent weeks we have highlighted potential systemic risks from ‘breaking the buck’ on Stablecoins – if the collateral backing the one-to-one dollar link unravels- and potentially the largest corporate collapse ever, China’s Evergrande.

Imagine my excitement to see the two risks potentially combined, as outlined in a tweet from TheLastBearStanding – as he says, sometimes the truth is stranger than fiction.

Remember Tether’s one-pager to the regulator this spring, outlining the assets backing its Tethers, saying that 76% was in cash or cash equivalents. Most of the remainder was Commercial Paper, which surprised market observers as this would make it a significant buyer, but the largest CP Players were not aware of their participation in their market. In August, it gave an update, now almost half is in commercial paper and certificates of deposit – a hefty $30.8bn – with just 10% in cash.

Tether has denied that these are loans between crypto exchanges and itself, and in an interview with CNBC refused to give details of its commercial paper holdings beyond that its assets contain international CP “overwhelmingly rated A2 or better.” It declined to answer whether any of it was Chinese. Given that there were concerns over the collateral surely it would have been in their best interests to deny it – suggests TheLastBearStanding.

Evergrande is a hefty issuer of commercial paper and was desperate to roll over existing debt as its bonds tanked and it became under increased pressure from the authorities and local banks. The CEO has probably exhausted the generosity and patience of his poker playing buddies.

Until recently Chinese companies used a legal loophole to use shell companies and affiliates to raise funds without having to disclose to regulators. But now, the regulators have asked them to provide details on a monthly basis.

Evergrande defaulted on some of its CP in June, according to Reuters. Coincidentally, in June Tether stopped printing additional paper and a few weeks later Fitch called out Tether as a potential systemic risk, citing its commercial paper exposure.

As TheLastBearStanding says: “A lot of smoke, but no smoking gun. But it does connect so many dots in a way that it can’t be totally dismissed.”

In the next few days, we may find the answer. Evergrande’s bonds fell on Tuesday as it warned of potential default in its earnings release. They fell another 5-8 points on Wednesday (2025s are in the 30s) as a social media screenshot doing the rounds purportedly said that the property developer is taking ‘detailed measures’ including the resignation of the CEO, laying off 60% of the staff and cutting the salaries of those remaining by half. More positively, the screenshot revealed that Evergrande is awaiting an injection of funds from state-owned enterprises.

Today trading in the bonds was temporarily halted as prices hit the 20% daily down limit, with some of its bonds falling into the 20s - could Evergrande be too big to fail or too big to bail?

Lars’ Heavy Water experiment

Over the years I’ve found that trawling through court lists and recent judgments can prove fruitful. It does help to have a memorable surname. In 2009, I saw Rouvroy listed as a defendant with two hedge funds as claimants. Unsure if this was Jacques Rouvroy, the CEO of French drinks business Belvedere, I took the short walk to the Royal Courts of Justice, and was treated to viewing his uneasy cross-examination, as QCs grilled him on his reneging of a warrants deal struck with the two funds.

The court was virtually empty but was full of bondholders and their advisors the next day, after my report. The company was already in Sauvegarde insolvency protection. In the end, the CEO and Chairman faced contempt of court and having their personal assets seized. Jacques claimed poverty as all assets were in the name of his wife who was divorcing him.

It was such a bizarre situation. My biggest memory is talking to Bruce Willis’ agent to confirm that the Chairman didn’t have a back problem stopping him travelling to the UK to face the courts and listing his personal assets. The chairman was spotted and photographed by Time Magazine dancing with the actor at Belvedere’s shareholder party a day earlier. Incredibly, our flamboyant and well-connected head content editor knew his agent personally.

This week, checking to see whether the Comexposium judgment has been published, I unearthed a judgment from last week, against Lars Windhorst. For those looking for a history of the controversial and flamboyant German financier, I recommend the excellent coverage from Robert Smith and the team at the FT over the past couple of years.

His links with Natixis’ H2O asset management, who invested in illiquid bonds issued by Windhorst’s companies such as lingerie business La Perla and Hertha Berlin football club are well known. H2O Investors eventually became spooked, withdrawing €8bn from the funds, leading to an agreement last year whereby he would buy back some of the illiquid bonds. The FT noted that Windhorst registered a Luxembourg entity Evergreen Funding as a vehicle to repurchase the bonds.

The judgment fills in some of the gaps and provides some interesting revelations.

Windhorst failed to honour a February 2020 settlement to Heritage Travel and MLDO Private Foundation, leading to a June settlement. These related to four sets of repo transactions in shares of companies connected to Windhorst which served the purpose of providing short term loans to himself, his Tennor Holding BV company, La Perla, and Civitas Properties. He was ordered to pay €55m by June 2020 and a further €69.2m by February 2021.

Windhorst’s only prospect of raising the funds to repay the claimants was via the Evergreen transaction, notes the judgment. The claimants had threatened to sabotage the transaction unless they entered into the June 2020 settlement.

According to the judgment - the Evergreen Transaction was explained by Mr Windhorst as follows:

In around April 2020, an opportunity arose with a third-party investor, H2O Asset Management ("H2O"), to raise additional finance so that Tennor [the Second Defendant] would be in a position to buy back the relevant shares in respect of each of the [Prior Transactions] (as varied by the February 2020 Settlement Agreement).

This deal .. required Tennor to establish a special purpose vehicle, Evergreen Funding SÀRL .. which was to purchase a number of securities from H2O, then issue bonds to investors in order to raise the necessary finance .. I anticipated that the amounts raised from this transaction would be up to EUR 1.25 billion, which would readily allow Tennor to repay the amounts outstanding to the Claimants, as I told Ms Levis and Mr Lefebvre at that time ..

It was revealed during submissions that the bonds would be repurchased for €850m, a deep discount to the €1.25bn originally paid by H2O. However, as the judge commented:

“Unfortunately, that explanation still does not reveal how these "illiquid stocks and bonds" could realistically have been expected to stand as the underlying assets for a securitisation that was itself intended to yield EUR 1.25bn, given that the market value of such "hard-to-sell assets" might (at least prima facie) be expected not to be significantly greater than the acquisition cost of EUR 850m. That, however, is not an issue that I am in a position to explore further on this application.”

We would note this is the exact opposite of one of the key principles of securitisation – overcollateralization. But in the end the deal failed to go ahead as the FCA started to investigate H2O transactions which Mr Windhorst said had put off investors in the securitisation.

In brief

Imagina lenders have extended their minimum liquidity covenant waiver to 15 September to explore two restructuring offers, according to a local press report. One is from shareholder Orient Hontai Capital with a €620m recapitalisation plan, the second is from Searchlight, Invesco, and senior lenders with over €200m of new money and equitizing all the second lien and €150m of the first lien.

As more and more challenging credits are put in front of investors, I often hear analysts using the phrase Sh*tco – this Fintwit HY investor presents the 10 principals they should live by

Finally, a shout out to @lewis_goodall and the BBC Newsnight team for their special on the building safety scandal, its causes and implications. A Grey rhino for the UK property market and the economy. Essential watching on catch-up.