This website uses cookies, pixel tags, and similar technologies (“Cookies”) for the purpose of enabling site operations and for performance, personalisation, and marketing purposes. We use our own Cookies and some from third parties. Only essential Cookies are used by default. By clicking “Accept All” you consent to the use of non-essential Cookies (i.e., functional, analytics, and marketing Cookies) and the related processing of personal data. You can manage your consent preferences by clicking Manage Preferences. You may withdraw a consent at any time by using the link “Cookie Preferences” in the footer of our website.

Our Privacy Notice is accessible here. To learn more about the use of Cookies on our website, please view our Cookie Notice.

The freight-ening truth - is shipping aligned to climate goals?

Jack David

•16 min read

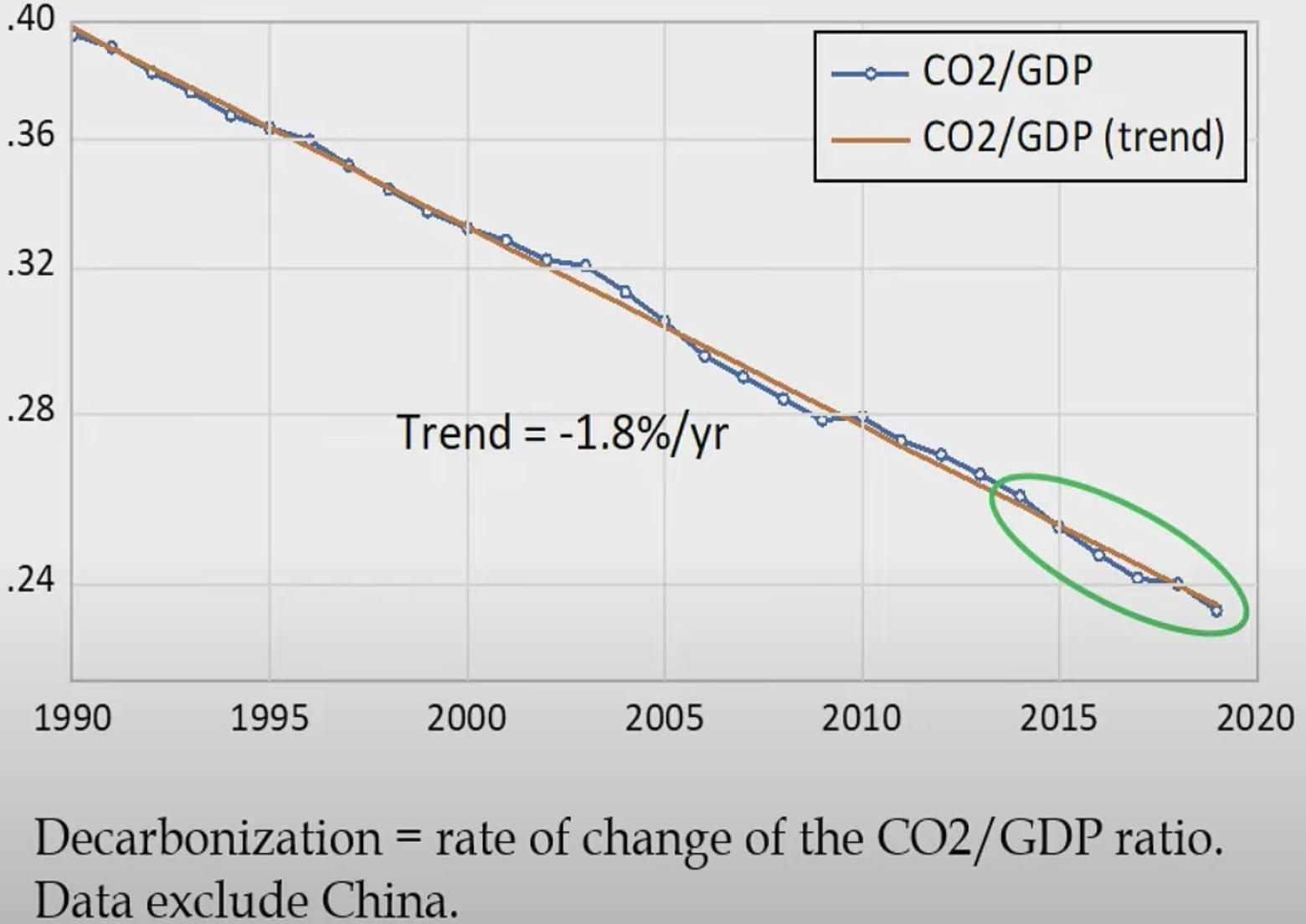

The climate crisis is rapidly shifting from an abstract and theoretical future event, to something that we see happening in the flesh. A new report from the IPCC estimates that even if we commit to drastic carbon reduction right now and hit our best-case scenario, we will still breach the biblical 1.5°C global temperature rise by 2040. Couple this with the sobering fact highlighted at the G20 climate conference in June; that over the past 30 years, the rate of reducing CO2 emissions hasn’t improved relative to GDP; declining at a steady -1.8% per year.

The grand total of unilateral agreements, corporate pledges, cultural awareness, government policies and new technologies have made little difference to the rate at which we are polluting our atmosphere with greenhouse gases. Estimates are that companies need to average a 10% GHG reduction per year until we hit net zero in order to avoid the worst case scenarios. Industries differ greatly in their efforts and progress but one industry, passenger, freight & cargo shipping, has been called out as both a rising emitter and a climate change laggard.

At 9fin, we cover 18 European transport shipping companies that have offered 80 bonds and loans since 2009, making it a significant segment of the LevFin universe. In the past year, we’ve seen an uptake in sustainability-linked bonds and loans.

Notably, Hapag-Lloyd spruced up its offering in April with a lick of green paint by linking it to a single emission intensity target and Ship Finance International (somewhat feebly) tried the same in May. Like the industry’s sustainability efforts at large, these deals have run up against criticism. In this case, cashing in on greenium while having limited real world impact, as well as incentivising investors to bet against portfolio companies hitting their green targets.

Dragging anchor on emissions

Shipping accounts for 3.6% of global emissions, and is one of the fastest growing emitters with a 32% increase over the last two decades. Not unlike the vessels themselves, it is a historically slow moving industry, especially with regards to regulation. Since the invention of the shipping container, arguably the biggest driver of globalisation over the past 50 years, it has been more-or-less business as usual for the sector. Slow steaming regulation has failed to materialise and the IMO’s first sulphur emissions regulation only came into force last year. This is despite reports from 2016 which showed low grade marine (bunker) fuel contains 3500 times more sulphur than road diesel.

Shipping companies have been criticised for their delayed and backward looking response to the regulation, choosing not to act until the last moment and then looking to what some technical experts have called a "dilapidated technology called scrubbing, which was invented in 1858" instead of investing early in progressive alternatives, such as nanotechnology.

In 2018, the UN International Maritime Organization (IMO) sought to change the industry’s course with its new strategy for a green future, targeting a 50% reduction in GHG emissions by 2050 vs 2008. In stark contrast to this target, the IMO’s fourth GHG study actually estimates a 50% rise in emissions by 2050 vs 2008, under a business as usual scenario. The International Chamber of Shipping (ICS) reports that the IMO target would require carbon efficiency improvements of 90% when global trade growth is factored in. Despite the monumental scale of this task, if achieved, the IMO target will still considerably fall short of the Paris Agreement’s 1.5°C pathway as well as EU Green Deal targets.

In order to support the UN’s aims, 80 stakeholders formed the Getting to Zero Coalition in 2019, partnered with Global Maritime Forum and Friends of Ocean Action and backed by the World Economic Forum and the World Resources Institute. The coalition now has more than 150 members and a number of publications have been produced in order to define the roadmap. In its latest attempt to steer the industry around the figurative (and literal) storms ahead, in June 2021, the IMO announced the new Energy Efficiency Existing Ship Index (EEXI), which will require all ships to report on their efficiency and implement corrective action for low scoring vessels, and the Carbon Intensity Indicator (CII) rating scheme to address operational efficiency. These proposals were met with mixed response: ship-brokers, SSY, estimate that only 25% of bulk carriers and tankers will be able to attain EEXI compliance, which may hit notoriously slow-to-change shipping companies hard.

On the other hand, NGOs have accused governments of riding “roughshod” over the Paris Agreement by signing off on a half-measure set of proposals. Protest groups have also pointed out the imbalance of power within the IMO, claiming it to be acting on behalf of “tier one" nations and the prosperity of the industry itself, instead of acting as a global UN body, responsible for complying with the Paris Agreement. This government policy gap is in part due to the complex nature of the global shipping environment, but it does not reflect the technological and industry level factors that are driving change within shipping.

Fly, drive or sail

When comparing aviation and shipping, aviation emissions were partly brought into the EU’s emission trading system (ETS) in 2012, whereas shipping has only been proposed as an addition in July under Fit for 55, with a planned inclusion for 2026, a delay which the Clean Air Task Force say has no justification. The delay in shipping’s inclusion so far has been down to the complexity of apportioning global shipping emissions to nations. Perhaps as a result of the pressure applied by ETS inclusion, the International Civil Aviation Organization (ICAO) took early action in 2010 to halt emissions growth after 2020, eight-years prior to the first IMO target. Additionally, the Fit for 55 proposals support the use of biofuels that have been linked to deforestation as well as LNG gas, a fossil fuel which contains high levels of methane (a gas which has a global warming potential (GWP) 25 times that of CO2).

Given the availability of zero-emission fuels and the enormous amount of funding needed to facilitate replacing one fossil fuel technology with another, the proposals do not make much sense. This same allowance was not given for the automotive sector, which pushed back against a proposed ban on sale of all fossil fuel vehicles by 2035 and the aviation sector (which has comparable global emissions to shipping) agreeing to all flights within and departing the EU hitting net zero by 2050 under destination 2050.

At an industry level, pressure is being applied from shipping supply chains. Major suppliers such as Amazon are encouraging companies to clean up in order to reach their own carbon-neutrality targets. In recent years, the tide does seem to be turning for the shipping sector, with some reports that these factors have helped edge shipping ahead of aviation on GHG matters. Despite this, mediocre action on the part of IMO and the EU suggests that they are failing to recognise this shift; giving the sector major allowances and causing some to label the shipping sector a carbon freerider.

In terms of technology, shipping should be able to make greater strides than aviation. Design tolerances are lower with aircraft, meaning that it is much easier to retrofit a ship with zero-carbon technologies such as new fuels, larger batteries, and new hull designs. However, in recent years there has been a lack of investment in new fleets due to uncertainty around trade growth as well as anticipation of environmental regulation. Shipping companies are unwilling to invest in any one technology as there is a risk that regulation will steer the industry in a different direction, leading to stranded assets.

At the aforementioned G20 climate conference, it was made clear by academics and policy makers alike that competitive green technologies lacked R&D funding across the board, and perhaps nowhere is this clearer than with shipping. In order to funnel funding into low-carbon technologies the price of carbon needs to be sufficient to make the investment in R&D attractive, and without a global price on carbon, carbon leakage threatens to undermine efforts. To date, the UN Climate Change Conference (COP) has failed to establish a global carbon market due to a lack of agreement across nations, especially in relation to the Common but Differentiated Responsibilities and Respective Capabilities (CBDR-RC).

The shipping sector is taking some action on the technology front. The ICS asserts that IMO targets cannot be reached by efficiency improvements alone, and will require industry wide deployment of zero-carbon technologies such as green hydrogen & ammonia, fuel cells for long charters, and electric propulsion and batteries for shorter trips. Unlike within the automotive sector, these technologies do not yet exist in a form and scale needed to make a transition realistic.

In response, the industry has proposed a $5bn Research & Development (R&D) fund to facilitate progress. The ICS has backed a $2 levy on every metric tonne of shipping fuel with the aim of raising $500 million in R&D funds and 40% of commercial shipping nations have already signed the proposal. Although, many fear this is too little too late within the wider context of the climate crisis. The Environmental Defence Fund (EDF) amongst other groups have countered the levy is inadequate and will retract from other more meaningful carbon pricing strategies. A lack of incentive for funding or government policy to date has stunted developments, meaning companies now face a substantial headwind en route to zero-emissions.

The Energy Transition Commission argues that the “first wave” of commercial zero-emission shipping projects must occur within the next five-to-10 years in order to reach the IMO target.

We take a look at a range of proposed technologies below, as well as some indication of how well each of the companies we cover are doing on track towards these goals.

Fuel and system efficiency

Fuel is by far a ship operator's biggest cost, so there should be a considerable financial incentive to improve ships’ efficiency and reduce fuel consumption. A variety of technologies include zero-ballast designs, streamlined propulsion systems, hull shape and construction, anti-fouling paint, speed nozzles, efficient steering gears, streamlining bubble technology and route optimisation. Each measure could offer roughly a 3% to 5% increase in efficiency.

LNG gas

Liquefied natural gas (LNG) is a fossil fuel estimated to reduce CO2 emissions by 20-25% and sulphur emissions by 90-95%. While this sounds promising, some groups warn that in reality, it offers little benefit over traditional fossil fuels, and that this benefit may evaporate completely when its high methane content is factored in. There is a risk that the costly conversion of ships to LNG gas will provide a false sense of security for the industry to continue its business as usual trajectory, locking in fossil fuels over the next few crucial decades and causing the industry to fall short of its targets and the Paris agreement.

Low and zero carbon fuels

The Energy Transition Commission’s blueprint for zero-emissions ships focuses on low and zero-carbon fuels as the main driver towards hitting IMO targets. Many of these fuels are traditionally made via electrolysis powered by coal, however, “green” varieties can now be produced using renewable energy. Scaling up this technology will be a challenge, for example it would take 60% of the world's renewable energy to power the shipping industry using hydrogen.

Biofuels, some of which can be used in existing engines and fuel infrastructure, are also close to cost-parity with traditional fuels. As such, industry leaders have initiated commercial scale operations. Although vastly less carbon intensive than traditional fuels, they do emit CO2 upon use. Other concerns are around availability of sustainable bio-feedstock and impact on land-use change, including deforestation, meaning use is controversial and may ultimately be an environmentally damaging fuel alternative.

Hydrogen is already used as a fuel in road transport and a significant reduction in the price of zero-carbon (green) hydrogen is expected in the next 10-15 years. Although promising in the long term, limitations, such as the need for large storage containers, low storage temperature and high volatility and flammability may make other fuels better suited to the task.

Ammonia is heralded as a promising fuel, and is the second most widely produced chemical globally, mostly used as a fertiliser within farming. Ammonia is made using hydrogen and has much of the same minimal waste products. The fuel requires less container space and lower storage temperatures than hydrogen, but would require new regulation due to its toxicity. Currently the cost of green ammonia is 2.5 times that of conventional fuels.

Methanol may be more widely available than ammonia in the short term as methanol-HFO engines are already commercially available. Methanol still emits CO2 on point of use. To be carbon neutral the technology would need Direct Air Capture (DAC) technology, which is expected to be commercially available towards the end of the 2020’s. The fuel can be held at the same temperature as traditional fuels.

Synthetic diesel is produced with hydrogen and CO2 and could be used with existing engines and infrastructure, however, also emit CO2 upon use. The same constraints around Direct Air Capture (DAC) technology as with methanol exist. The technology is expected to be commercially available by 2030.

Electric propulsion

Electric propulsion is unlikely to be viable for deep sea journeys due to limitations of battery technology; it would reportedly take a ship the power of 10,000 Tesla batteries per day to cross the Atlantic. However, electric propulsion, batteries and hydrogen fuel cells are likely to play a part in short hall and passenger shipping, as well as exploration and seabed monitoring vessels, with the first ships already in operation.

Wind power

There has been growing interest in one of the earliest forms of ship propulsion. Innovative sails, deck mounted wings, kites and hull designs could all play a key role in the net zero transition and a growing number of vessels are already incorporating the technologies as auxiliary and assistant propulsion systems.

LevFin leaders & laggards

Here are a selection of industry leaders, middle-of-the-roaders and laggards within the LevFin universe. We have assessed the companies we cover by the following criteria:

Ambition of environmental strategy, including emissions targets in relation to peers, IMO and Paris Agreement targets;

Strength of roadmap to achieving this strategy and targets, including R&D investment in zero-emission technology; and

Current progress along roadmap and towards these goals.

Benchmark: Maersk

Not a high-yield issuer, but included here as a benchmark. The Gliese Foundation rated Maersk 4.9/5 on environmental reporting, topping its leaderboard. A founding member of the Sustainable Shipping Initiative, Maersk is considered an industry leader and is one of only two companies (with Evergreen Marine) that report to the Task Force on Climate-Related Financial Disclosures (TCFD). Maersk has channeled considerable funding into zero-emission technology R&D and has an ambition to have an all carbon neutral fleet by 2050, aligned with the Paris Agreement and net zero targets, leading the unambitious IMO target considerably. Maersk also reports on its scope 3 emissions, which may soon be subject to more stringent mandatory reporting. Only Maersk and CMA CGM currently report on this data, setting them ahead of probable future regulatory requirements. Notably, Maersk has made the decision to transition directly to zero-emission fuels, bypassing EU-supported LNG gas alternatives.

Maersk is aiming for the first zero-emission container ship to become operational by 2023, fast tracking its original target by seven years. With an additional 16 ships, capable of sailing from China to Europe ready in 2024 and 2025. Each ship has a 16,000 container capacity and are said to be replacing old ships rather than adding new capacity. It should be noted that zero-emission operations are heavily reliant on supply chains and supporting infrastructure, as such, the ship is built to run on fossil fuels as well. Nevertheless, this is an industry first, proving that shipping can make the transition. Maersk falls short of a clean slate by failing to rule out the controversial North Sea arctic shipping route, having completed the first voyage in 2018.

Leader: CMA CGM

CMA CGM is rated 4.5/5 by the Gliese Foundation on environmental reporting, ranking it third overall. CMA CGM ultimately achieves leader status among high-yield issuers due to its 2050 carbon neutrality target, which equals Maersk and aligns with the Paris Agreement and net zero targets. CMA CGM has comprehensive reporting, including scope 3 emissions and details of specific low carbon technology and efficiency improvements to ships, including hull design (bulbous bow) and propeller improvements.

The LNG transition puts CMA CGM behind Maersk. Notably, this a major element of its carbon neutrality strategy, relying on offsets to achieve “carbon neutral LNG”. Offsetting carbon will be a key tool in achieving net zero, however, it remains a controversial strategy, especially while carbon is not properly priced. Despite stating that it has “invested heavily” in R&D, progress seems to be relatively slow, with technical solutions in the prototype stage. However, CMA CGM has signed an agreement to avoid the North Sea arctic shipping route.

Middle-packer: Hapag-Lloyd

Hapag-Lloyd is rated 3.5/5 by the Gliese Foundation for its reporting due to a lack of environmental data provided. Despite this, its emission targets are aligned with leading peers, by aiming for a 60% reduction in emissions intensity by 2030 vs 2008 levels. On the other hand, the organisation fails to address the equally important absolute emissions and doesn’t have a definitive net zero target.

The company is the first to retrofit a large container ship with LNG capability, which highlights its focus on this technology. Hapag-Lloyd has plans to introduce a further 6 six ships (of a 230 ship fleet) and are in the “initial test phase” of testing one biofuel; used cooking oil. There is evidence of investment in efficiency increasing technologies, such as logistics improvements, hull design and coating, and waste heat utilisation. However, there is minimal evidence of investment in zero-emission fuels and heavy investment in LNG gas transition may ultimately retract from the industry reaching crucial net-zero goals. Hapag-Lloyd has also agreed to avoid the north sea arctic shipping route.

Middle-packer: MSC Cruises

Given a generous 4.6/5 stars by the Gliese Foundation on environmental reporting, MSC Cruises tops the chart for passenger shipping despite not having particularly strong targets, merely aligning to IMO targets on emissions intensity and absolute emissions. MSC does have evidence of investment in zero-emission technology, for example, by joining the Hydrogen Council and taking part in the CHEK consortium.

However, the company is aiming for a zero-emissions fleet “in this century”, a vague and unambitious target. Additionally, the organisation is mostly LNG-centric, with three ships on order for 2022 (of a fleet of 17 ships). MSC does show awareness and understanding of environmental issues and acknowledgement of its own limitations, for example, connected to LNG use. As such, MSC falls short of leaders within the wider industry, such as Maersk.

Middle-packer: Carnival

Carnival scored a 3/5 star rating by the Gliese Foundation for environmental reporting, ranking it mid-way down the table. However, as the first cruise company to join the Getting to Zero Coalition, Carnival is making some reasonable steps towards carbon-neutrality.

The company has set a target of 40% reduction in CO2 intensity by 2030 which is aligned to the IMO target for intensity, but the company fails to set an absolute emissions target, which means that it would not be aligned to the Paris Agreement. Like others, the organisation is “pioneering” LNG gas, as the first cruise company to do so it leads peers and aligns to EU targets, however, the same concerns remain with investment in LNG gas.

Laggard: Ship Finance International

Ship Finance International Limited’s (SFL) ESG report spans a mere 19-pages and is sparse in detail. As a private company, there are no requirements for reporting on ESG factors but some emissions data is provided. The company states that materiality assessments have been carried out but that no targets have been set to date, including emissions targets. This means that the company is not aligned to the Paris Agreement or any net-zero pathways and is yet to establish a strategy for decarbonisation (it plans to do so in 2021).

The company describes a number of measures such as digital tracking of fuel efficiency on ships and scrubber technology for SOX removal, but these measures are legal requirements and are only just in keeping with IMO regulation, proving that to date, SFL is reactionary rather than proactive on environmental factors. Additionally, SFL highlights a number of ships in its fleet that are being phased out under IMO requirements, including its non-double hull tankers. In general, a lack of action on environmental considerations could lead to stranded assets for the company.

SFL has issued a sustainability-linked bond, which doesn’t give any high level targets for emissions, but does stipulate one KPI; that the amount equal to the size of the issue is to be spent on acquisition and retrofitting of ships with “low carbon/alternative fuel source” technology. Considering that over the next five years, to meet minimal IMO fuel efficiency requirements this investment would likely have to be made anyway, the SLB is not ambitious. Additionally, on a recent earnings call, SFL describes that the main reason for issuing the bond was to generate more investor interest and as such, more liquidity for the offering, with no mention of the environmental benefits.

We would be happy to send you more of our ESG content and analysis. If you would like samples, please contact team@9fin.com