News & Insights

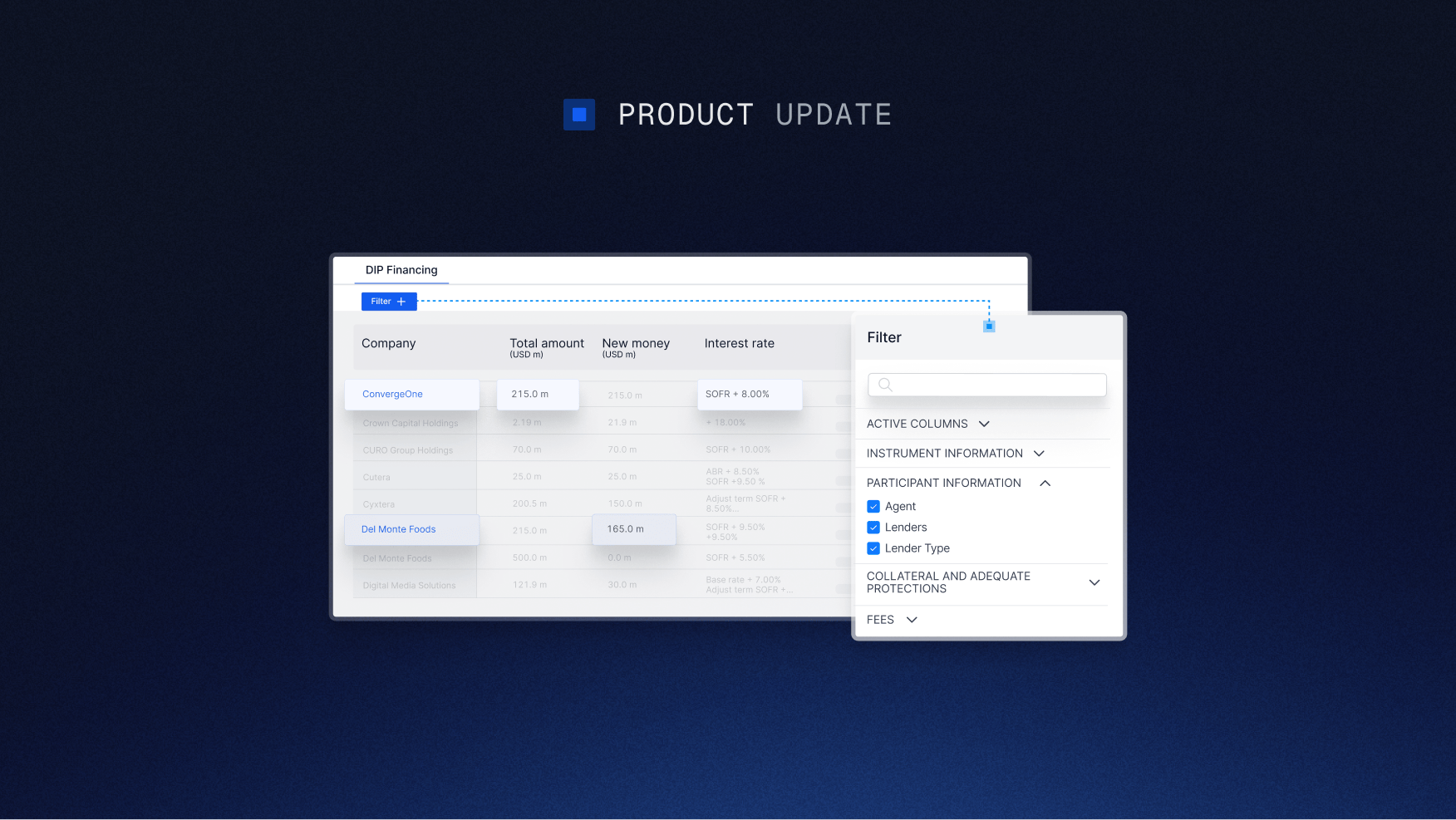

InsightsUS IG Wrap — Oracle lawsuit brings ‘fake it till you make it’ vibes to IG, Goldman leads bank surge

Market Wraps

US IG Wrap — Oracle lawsuit brings ‘fake it till you make it’ vibes to IG, Goldman leads bank surge

William Hoffman16 Jan 2026 | US | 5 minute read

Related Posts

Discover more insights.

Use the previous and next buttons or keyboard arrows to navigate between slides.